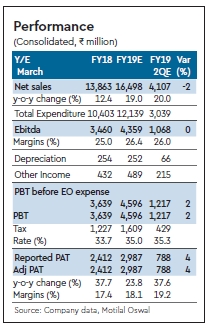

TELX’s reported 18% revenue growth y-o-y which amounts to revenue of `4 bn, lower than our expectation of 20% growth. Sequential growth for TELX at 5.4% was partially fueled by INR depreciation, adjusted for which, we estimate the growth would be marginal. Historically, Q2 has seen sharper growth for TELX given seasonality. Ebitda margin expanded by 190bp y-o-y to 26.5%, in line with our estimates. Consequently, PAT growth of 44% y-o-y to Rs 822m was above expectations by 4% on account of higher-than-expected Other Income. TELX has seen a gradual increase in growth rates since it hit its bottom in Q1FY18, from 9% y-o-y to 18% y-o-y now.

Valuation view: Given growth in the Engineering Services market, emergence of new areas like Medical Devices and Cloud, and strong traction across segments, we are currently expecting 20% revenue CAGR over FY18-20. Estimates for the quarter weren’t materially different from our expectations, thereby not changing our forecasts much. However, “headwinds in the British car industry” as cited by JLR, and BMW profit warning on trade war are risks to the company’s business that will weigh on valuation multiple (and earnings if reflected in demand by TELX). We hence value the stock at 25x FY20e EPS (versus 30x earlier) and maintain Buy with a TP of Rs 1,400.