BRIT’s sales growth at 10.3% y-o-y (7% domestic volume growth) was broadly in line with our estimates while Ebitda and PAT growth of 9.9% y-o-y and 12.8% y-o-y respectively came slightly below our estimates as margins disappointed on higher costs of new launches and subdued subsidiaries showing. We cut our estimates to reflect higher launch pipeline which will keep margin expansion under check. Maintain Hold given high valuations limiting upside potential.

Domestic standalone business

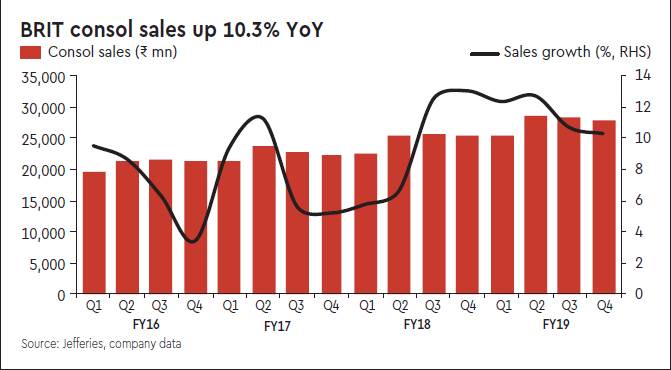

Standalone domestic business grew by 11.7% y-o-y led by 7% y-o-y volume growth in Q4FY19. Given the backdrop of slowdown in rural growth, we believe that growth trajectory is steady, also helped by market share gains, distribution expansion and strong innovation.

Consolidated growth

Consolidated growth was slightly lower than domestic standalone business due to lower growth in the international business. Growth in dairy and bread business, however, was in double-digits.

Margins

Standalone Ebitda margin grew 34bps y-o-y while consolidated Ebitda margin was flattish y-o-y. Raw material inflation has been benign (up 3% in Q4FY19) while expenses towards goodwill write-off and scale-up of manufacturing capacity led to higher other expenses.

PT and view

Britannia continues to gain market share in the core biscuits category coupled with a stepped-up focus on building new categories. While new categories would aid topline growth in the near term, it would limit margin expansion given investments needed in the scale-up. Valuations at 51.4x FY20 PE seem full given 16% EPS CAGR over FY19-21 amidst high consensus expectations (we are 4-6% below consensus).