RIL stock is down 15%, underperforming SENSEX by 10% in the past 3 months which we see as a buying opportunity. Concerns related to deleveraging and downstream margins appear to overlook upside potential from telecom and retail. Valuations are inexpensive; maintain Buy with lower TP of Rs 1,740 (from Rs 1,780).

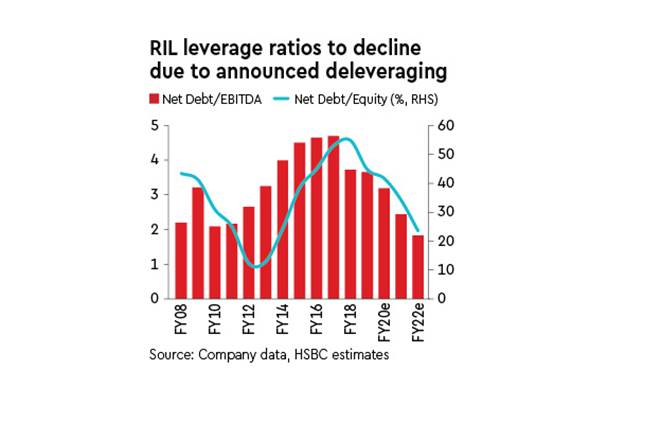

Debate 1: What if progress on RIL’s deleveraging plans slows down amidst rising macro uncertainties? We believe RIL is on a sustained path of deleveraging through: (i) strong operating cash flow generation; (ii) capex discipline; and(iii) selective asset monetisation. RIL is targeting to reach zero net-debt by FY21e; it announced several asset monetisation deals in 2019. In Q3FY20, RIL suggested steady progress towards completion of separate deals with Aramco (energy business), Brookfield (Tower InvIT) and the possibility of strategic investors in Fibre InvIT. Even in a negative case of slow progress on these, $21 bn of FCF over FY21e-23e should help RIL achieve zero net-debt by 2Q23e. RIL’s adjusted net debt of $32 bn appears high; however, its leverage ratios have started to decline, which supports our thesis of sustained deleveraging.

Debate 2: Will the margin uncertainties in its energy business lead to material de-rating of its valuation? Fears of large earnings estimate downgrades for RIL are overdone, in our view. We expect chemical margins to remain flat and GRMs to normalise in FY21e which along with the ramp-up of petcoke gasifiers should drive 15% growth in energy Ebitda. RIL’s chemical product portfolio is well diversified with feedstock flexibility placing it on the lower end of the global cost curve.

Further, chemical margins across most products are nearing or below their cash costs for its marginal supplies, indicating further downside is unlikely. While extrapolation of refining margins may suggest 5-6% downside to earnings estimates, we think this is partly balanced by the possibility of an increase in telecom tariffs. For sensitivity $1/b GRM impacts Ebitda by 3%; however, this can be offset by 5% or Rs 7 increase in ARPU.

Debate 3: Will RIL’s transition to become a consumer play gather pace? Together, Telecom and Retail businesses now contribute 30% of RIL’s consolidated Ebitda which we expect to increase to 46% by FY23e. Our comparison of operating performances suggests it continues to outpace peers in both segments. We think both these segments have large value creation potential in the medium term, which remains underappreciated in our view.

Valuation is not expensive: We factor in lower downstream margins leading us to cut our FY21e/22e earnings by 8%/5% and TP by 2% to Rs 1740. RIL is trading at an FY22e EV/Ebitda of ~7x, similar to its 10-year historical average. Steady earnings momentum and inexpensive valuation drive our Buy rating. Key risks include: (i) lower refining/chemical margins; (ii) higher-than-expected capex; and (iii) lower-than-expected ARPUs and subscriber additions in telecom.