and gain market share with improving profitability.")

Provision write-backs and healthy NII helped KMB to report strong Q3FY19 PAT of `12.9 bn (+23% y-o-y, marginally ahead of our estimate). NII grew 23% y-o-y to `29.4 bn, led by healthy loan growth of 23% y-o-y/6% q-o-q and margin expansion of 13bp q-o-q to 4.33%. For 9MFY19, PPoP grew 18.0%, while PAT increased 17% y-o-y.

Loan book grew 23.5% y-o-y, led by strong growth in retail loans (+25% y-o-y) and corporate loans (+22.5% y-o-y), while deposits grew 18% y-o-y (CASA deposits up 28.5% y-o-y). SA deposits continued growing strongly by 31% y-o-y (SA cost of 5.67%). Core deposit mix (CASA + TD < `50 m) stood at 80% of total deposits. CASA mix improved to 50.7%.

Asset quality improved, with NNPA declining by 6.9% q-o-q. The bank made provisions of `2.5 bn towards advances v/s our estimate of `3.6 bn. However, KMB reported negative provisions (-`0.3 bn) due to write-backs of `2.7 bn on the investment portfolio. GNPL/NNPL ratios stood at 2.07%/0.71% (-8bp/-10bp), while PCR improved by 337bp q-o-q

to 66.2%.

Subsidiaries performance remains mixed: Kotak Life reported 29% y-o-y growth in its net profit, while Kotak AMC reported 100% y-o-y growth on a low base. Kotak Prime and Securities, however, reported de-growth of 6/36% y-o-y. Share of the bank in consolidated profit stood at 70%. Consolidated PAT grew 14% y-o-y to `18.44 bn.

Other highlights: (a) KMB reported a Tier 1 ratio of 17.6%, with a total CAR of 18.1%; (b) SMA-2 advances stood at 18bp of loans; (c) According to Basel III, the exposure toward NBFCs has come down to 4.5% from 5.2% in Q2FY19. Exposure towards CRE (ex LRD), too, declined to 1.6% from 1.8% in the previous quarter.

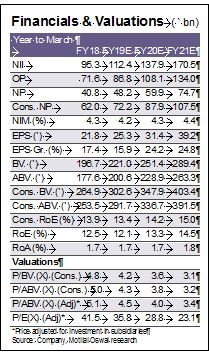

Valuation view: We revise up FY19/20e consol. PAT by 1.4%/2.3% and estimate consol. earnings CAGR of 20% (FY18-21e). We, thus, project FY21E consol. RoA/RoE at 2.2%/15.0%. We continue believing in KMB’s capability to deliver in a challenging environment and appreciate progress on building a strong liability franchise. We expect it to maintain continued traction in loan growth (FY18-21e CAGR of 23%) and gain market share with improving profitability. Maintain Neutral with a revised TP of `1,350 (3.8x Sep’20e ABV for the lending business).