DMART’s revenue growth at 33.1% y-o-y was slightly below while Ebitda and PAT growth at 7.5% y-o-y and 2.1% y-o-y respectively came in much below our expectations. Given price cuts by DMART, gross margin fall was on expected lines; however, rise in other expenses led to margin disappointment. Run rate of store addition is still lower than our full year expectation of 24 stores; we expect a sharp addition during Q4FY19. Maintain Hold with revised price target of Rs 1,420.

Quarter topline

DMART witnessed healthy topline growth of 33.1% y-o-y (on a base of 22.6% y-o-y) which in our view was led by SSSG of 18-20%. Strong SSSG is not only led by price cuts but also led by increased operating hours of the stores. Generally a D-mart store operates for 12 hours (10AM to 10PM) but company has increased the operating hours for some of its key locations to 15 hours (from 8AM to 11PM), especially in Mumbai.

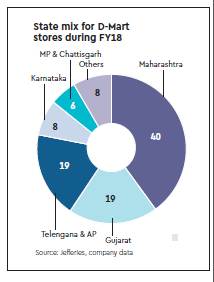

Store addition

Company added 4 new stores during Q3FY19, taking the total count to 164 stores (9 stores YTD19). Ergo, we expect increased store addition during Q4FY19 similar to FY18 when during Q4FY18 the company added 14 stores. However, company is opening larger stores as average size per store opened during YTD19 is ~45,000 sq ft per store, as against company average of 32,000 sq ft per store.

READ ALSO | The RuPay card PM Modi used to buy jackets; Know all about this India MasterCard, Visa rival

Margins in Q3

DMART saw gross margin dip of 170bps y-o-y which was led by price cuts undertaken in Q2FY19. Ebitda margin saw a decline of 199bps y-o-y impacted further by 39bps y-o-y increase in other expenses. Mgmt in its commentary said other expenses were also higher due to some preloading of expenses which in our view are one-time. Longer store operating hours during festive season also resulted in increased other expenses from higher sub-contracting expenses.

Change in estimates

We marginally cut our revenue estimates by ~1%; however, on account of lower than expected margins, we cut our Ebitda for FY19-21e by ~4%. Our EPS estimates are trimmed by ~5% for FY19-21e due to higher interest costs and lower other income.

Our view and PT

Mgmt’s strong execution, focus on market share gains and throughputs gives confidence on topline growth but margin expansion will be slow and scale led. Ergo, though D-mart will be one of the key beneficiaries in organised grocery retail space, trajectory of earning growth will taper down viz-a-viz that built in valuations keeping risk reward unfavourable (trading at 46x Ebitda FY20). We roll over to Mar-21 Ebitda and cut our target Ebitda multiple to 33x (from 35x earlier) to arrive at price target of Rs 1,420.