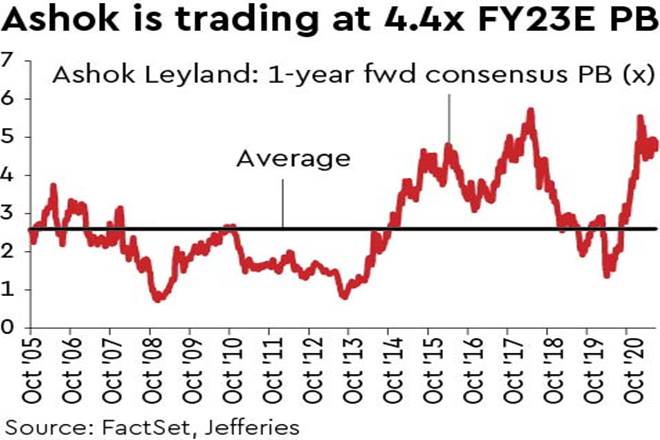

AL’s Q4 EBITDA rose 110% q-o-q, 18% above JEFe. The second wave of Covid has impacted truck demand and delayed the up-cycle; however economy is recovering well and June e-way bills rose 2% vs 2019. We cut FY22e EPS by 57% but broadly maintain FY23 estimates. We retain Buy but also our view that investors should moderate return expectations after ~3x rally since Apr-2020 as stock is already at 4.4x FY23e PB vs last peak of 5.8x while AL’s market share is slipping.

Good Q4 results: AL’s Q4 volumes grew 32% q-o-q (down 26% vs Q4FY19) while Ebitda rose 110% q-o-q (down 46% vs Q4FY19). Q4 Ebitda was 18% above JEFe led by lower-than-expected staff costs. ASPs were up 10% q-o-q but gross margin fell 250bp q-o-q on higher commodity costs. Ebitda margin still rose 240bp q-o-q to 7.6% led by operating leverage benefit. Recurring PAT was 10x q-o-q on a low base. In FY21, AL’s volumes fell 20% y-o-y, Ebitda declined 54% y-o-y and it reported net loss of Rs 3.0 bn.

Margins and balance sheet should improve: AL’s Ebitda margins fell from an average 11% in FY16-19 to 3.5% in FY21. We expect input costs for autos to intensify in H1FY22 as the full impact of CYTD metal price rally comes through, but vehicle price hikes should outpace incremental costs in H2. We expect AL’s margins to recover to 7.3%/11.3% in FY22/FY23.

Balance sheet worsened from Rs 7.4 bn net cash in FY19 to ~Rs 42 bn net debt in Q1FY21, but net debt is since down 38% to Rs 26 bn. FCF was negative over FY19-21 but should turn sharply by FY23.

Retain Buy: AL stock has trebled since April-2020 outperforming Nifty-50 by ~100%. We believe the stock still holds potential for healthy returns given trucks are at early stage of an up-cycle.

But investors should moderate return expectations as stock is already at 5.0x/ 4.4x FY22e /FY23e PB versus last cycle peak of 5.8x while AL’s market share is slipping.We retain Buy with Rs 150 PT (5.4x FY23e PB).