drove NII growth of 17% y-o-y.")

For Q1FY21, UNBK reported results for the merged entity (Andhra Bank and Corporation Bank are merged with UNBK with effect from 1 April 2020) and gave pro-forma numbers for Q1FY20 and Q4FY20. In Q1FY21, UNBK reported a PAT of Rs 3.3 bn (RoA of 0.1%). Lower cost of funds (down 65bp y-o-y) drove NII growth of 17% y-o-y.

However, a decline in fee income (down 37% y-o-y) and elevated operating costs (up 11% y-o-y) limited pre-operating profit growth to 3% y-o-y. Moreover, higher provisions, driven by COVID-19 and for legacy stressed accounts, resulted in a PAT decline of 13% y-o-y. Net NPAs (down 8% q-o-q) improved sequentially.

Net NPAs moderated; share of loans under moratorium at elevated levels: Mgmt highlighted that c28% of the customers in terms of value have availed the moratorium as at end-June. While gross NPAs remained stable q-o-q, net NPAs declined by 8% q-o-q as provision cover increased to 70% (vs 68% in Q4FY20). Mgmt guided for 3-3.5% of slippage estimates for FY21e. It also indicated that c5-6% of the customers (in terms of value) could opt for restructuring. We estimate c6.5% slippages for FY21e.

Subdued operating performance: In Q1FY21, loans were up just 2% y-o-y. Corporate/overseas book and agri book drove growth. Deposits increased by c7% y-o-y. CASA ratio increased from 32.2% in Q1FY20 to 33.3% in Q1FY21. NIMs remained stable y-o-y at 2.5%. Core fee and elevated opex dragged operating profit growth (up 3% y-o-y). With the merger and on account of harmonisation of accounting and credit policies, CET-1 ratio of the merged entity came in at 8.4% as at end-June 2020.

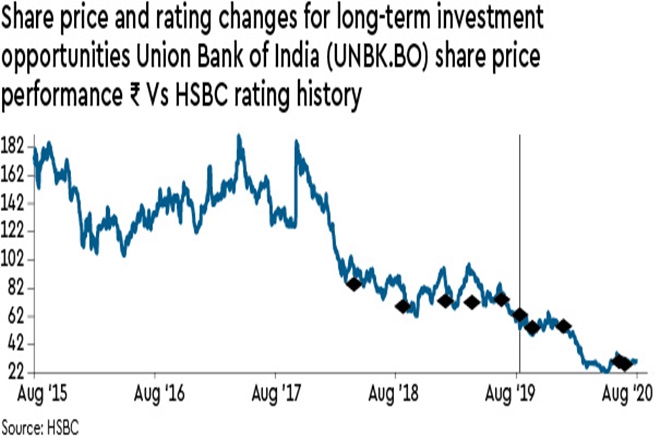

Hold; uncertain outlook with limited buffers: Low CET-1 ratio (of 8.4%), thin operating profit margins (1.5-1.6% of assets) and still-high net NPA ratio (c5%) leave little room for comfort. Ongoing disruptions from COVID-19-led lockdowns, integration of two weaker banks into UNBK and NPA/provision risk from the moratorium loan book cloud the near-term outlook. Our target price implies c8% downside. We maintain our Hold rating as we believe the stock is trading at inexpensive valuations (0.3x FY22e PB).