Britannia’s recent launch of lower unit packs (LUPs) in the creams segment (under Treat Jim Jam brand) offers ‘value for money’ and also caters to customer aspirations. The creams category is large (`18 bn) and highly profitable (net margins 2x that of category), but has so far been urban-focused. We note that the company has already done well with LUPs for its premium cookie brand Good Day – also in rural areas where demand for LUPs is good. Thus, creams LUPs should help the company to penetrate well in the rural markets and drive incremental volume growth.

Strategy for incremental volume growth is focused on:

Increasing rural salience: A combination of efforts (rural distribution expansion, dedicated focus on five key states in central India, new products and new pack sizes) over the past few years have helped BRIT to double its rural sales to Rs 15.56 bn. The company sees huge headroom for growth in rural markets, and expects revenue contribution from rural to increase to 30-35% (from 20% now) over the next 2-3 years.

Rapid growth in distribution: Distribution expansion for BRIT has been massive, with its direct reach doubling over the past three years to 1.56 mn. Its direct reach as of Q2FY18 stands at 1.8 mn outlets, second highest after HUL, implying addition of 0.24m outlets in H1FY18. BRIT has also set up 13,000 distribution points across rural areas. We believe that the company should not be benchmarked against Parle’s reach of 5.8m outlets (BRIT is narrowing the gap year after year on total reach; in terms of direct reach, BRIT already is twice as large as Parle), given that biscuits is a low-cost/high-velocity consumption product and that there is potential to boost the reach to 9 mn outlets.

Growing presence in weak states: Improving market share in the Hindi belt (Rajasthan, Gujarat, Uttar Pradesh and Madhya Pradesh) is the second key priority for BRIT. The company’s market shares are still in early teens in these states; it believes that there is still a long way to go. Notably, BRIT gained 170bp market share in these weak states in central India in Q2FY18.

Get lower unit packs to play a big role: Distribution expansion, along with introduction of LUPs of its products (have been successful in the hinterland) addresses one of our key erstwhile concerns that the imminent rural revival would lead to Parle clawing back some of its market share losses to BRIT in recent years. We note that LUPs have been in the market for many years now and doing well particularly in rural markets. LUPs form fairly large part of the business at 50% for BRIT, and thus, will be an important rural sales driver.

Focus on the Rs 5 pack of premium products: BRIT appears to have realised from experience that competing against Parle-G on price through its brand Tiger in just the basic glucose category would be tough. Thus, apart from Tiger variants like Tiger Creams, it has decided to introduce LUPs of premium products. When the introduction of Rs 5 packs of Good Day saw good success in 2013-14, BRIT decided to introduce LUPs for its premium offerings in 2015. Consequently, the performance of weaker states improved and BRIT started gaining shares there. In August 2017, as part of its strategy to expand the share in the creams category (Rs 18 bn category) from 35% to 50% over the next two years, BRIT introduced the Rs 5 pack for the creams category. Net margins in the cream category are 10% (2x the average biscuit margins). We believe this will help ramp-up sales in the rural regions and also would not be margin-dilutive.

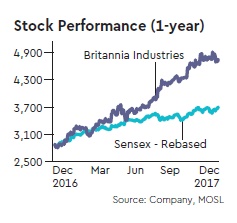

Valuation view

We are enthused with BRIT’s consistent healthy performance in a difficult operating environment. Rapidly expanding distribution, continuing investment in R&D and significant expansion of its own manufacturing indicate management’s optimism about the growth prospects. LUPs of premium products continue to receive good response, aiding volume growth substantially. Opportunity beyond biscuits is also substantially high. Continuing premiumisation, significant incremental cost savings and a favourable commodity cost outlook mean that 15% Ebitda margin is now achievable. We reiterate our Buy rating with a revised target price of Rs 6,100 (48x December 2019e EPS, a 20% premium to three-year average due to improving visibility on both volume recovery and margin growth).