")

China is building ships at a faster rate than any other country. Reports indicate that the country has increased investment in shipbuilding, and this year, more than 60% of global orders went to Chinese shipyards. S&P Global estimates China’s shipbuilding capacity is 200 times greater than that of the United States. According to a US Department of Defence report (2024), China has 332 ships, while the US has 291. This growth is primarily driven by its maritime sector. China has 10 of the world’s busiest ports, which are crucial to global supply routes.

This could pose a threat to India’s maritime security. Thus, India is also investing heavily in strengthening its defence ecosystem. Domestic defence production has grown from ₹460 billion a decade ago to ₹1.5 trillion. Of the total production, the private sector contributed ₹330 billion, and the rest came from public sector enterprises. Further, India aims to double defence production and export ₹500 billion by 2029.

Within defence spending, shipbuilding is at the centre stage due to India’s vast 7,500-kilometer coastline and heavy reliance on maritime trade. Mazagon Dock Annual Report states that the sector has an estimated investment multiplier of about 1.82. This implied that an investment of ₹1.5 trillion in naval shipbuilding could generate an estimated ₹2.73 trillion in economic activity.

Similarly, here are three shipbuilding companies that are expected to benefit from the growing shipbuilding industry…

#1 Mazagon Dock Shipbuilders: India’s Submarine and Destroyer Anchor

Mazagon Dock is the first government-owned shipyard to be awarded “Navratna” status and the third defence Public Sector Undertaking (PSU) in the country to have this unique classification. The company is the only shipyard in India that builds both destroyers and conventional submarines for the Indian Navy.

Mazagon’s Role in India’s Naval Backbone

Mazagon builds conventional submarines, such as the Scorpene class, in collaboration with M/s Naval Group, France. It constructs conventional submarines using two different technologies: the German SSK Class and the French Scorpene Class. The company is also the lead shipyard for building four Nilgiri-class stealth frigates.

The company also manufactures corvettes for the Indian Navy, and can build 11 submarines and 10 warships. Mazagon delivered one destroyer every 18 months between 2014 and 2025, bringing the total to seven. It has also built three frontline combat ships—INS Nilgiri, INS Surat, and INS Vagsheer —which were commissioned on 15 January 2025.

The company is closely aligned with the Government of India’s vision of Atmanirbhar Bharat and ‘Make in India’. The percentage of indigenous content in ships built by Mazagon has increased from 42% in the P15 Delhi-class destroyers to 75% in the P17A Nilgiri-class frigates (under construction).

How the Shipyard Is Expanding Its Capabilities

Mazagon Dock is investing ₹64 billion to expand its capacity. Its main focus is on developing a greenfield shipyard at Nhava Yard, which aims to build capacity for large ships and submarines, including major refits and repairs. It is also developing a greenfield shipyard at Tuticorin, Tamil Nadu, primarily for commercial shipbuilding, capitalising on government incentives.

The expansion projects also include the construction of a new floating dry dock with a capacity of 12,000 tons, the replacement of old level luffing cranes, and the establishment of a new fabrication workshop at Alcock Yarra. The company also forayed into the global market by acquiring a 51% equity stake in Colombo Dockyard in Sri Lanka for ₹4.5 billion.

The Colombo Dockyard will focus on commercial shipbuilding and ship repairs. Mazagon aims to ramp up the revenue of Colombo Dockyard from approximately INR 1,000 crores to INR 1,500 crores within the next year or so (a 50% increase). Also, in the commercial ship orders, the company is targeting short-cycle commercial projects, including tenders from PSUs like the Shipping Corporation of India, ONGC, and Indian Oil.

Mazagon aims to leverage its expertise in complex weapon-sensor integration for high-tech defence platforms to gain a competitive advantage in the international market. It plans to focus on patrol vessels, offshore support vessels, and green shipping technologies. Mazagon also intends to export pressure hull sections to countries manufacturing/procuring Scorpene-class submarines.

Muted Financials, but a Reinforcing Order Book Ahead

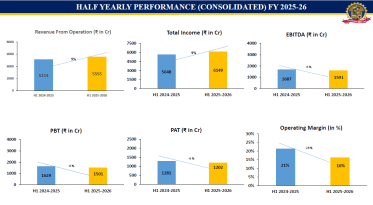

From a financial perspective, revenue rose by 9% to ₹55.6 billion in the first half of FY26. However, EBITDA (earnings before interest, tax, depreciation, and amortization) declined by 6% to ₹15.9 billion, while operating margins shrank by 500 basis points to 16%. As a result, profit after tax (PAT) fell by 6% to ₹12 billion, due to provisions of ₹10 billion for onerous contracts.

Mazagon Dock Financial Performance

Mazagon anticipates about ₹125 billion in revenue for FY26, up from ₹114.3 billion in FY25. Thereafter, the company expects a 5% growth in FY27 due to slower order book execution. However, it anticipates its order book to grow to over ₹1 trillion by FY27, from ₹274.2 billion as of 30 September 2025.

#2 Garden Reach Shipbuilders: Specialist in Compact Naval Platforms

Garden Reach Shipbuilders (GRSE) is one of India’s premier shipbuilding companies. The company is the first shipyard in India to build warships for the Indian Navy and the Indian Coast Guard. Its primary business activities, encompassing Manufacturing and Service, account for 93.8% of its total turnover.

Where GRSE’s Core Strengths Come From

GRSE also builds commercial ships and undertakes engineering and engine production activities. The company can build frigate-sized warships, but its strength lies in building smaller vessels for the Navy and Coast Guard. It has delivered 111 warships to the Indian Navy and Indian Coast Guard.

Additionally, as of 31 March 2025, GRSE had 40 vessels under construction. The company also engages in developing critical naval technologies, such as the 30 mm Naval Surface Gun. GRSE also repairs ships from other countries, like Sri Lanka, the Maldives, Mauritius, and the Seychelles. However, the ship repair segment’s contribution to revenue is only 2.2%.

The engineering division focuses on diversification, with a revenue share of 2.9%. The segment manufactures advanced products, such as portable bridges and specialized deck machinery. It actively works with organisations like the Border Road Organisation and the National Highways and Infrastructure Development Corporation.

How the Order Book Is Building Multi-Year Visibility

Looking ahead, management is confident that the order book will cross ₹500 billion by the end of FY26, from its current level of ₹202 billion. This order book (if materialised) will provide a strong multi-year revenue potential of about 10 years. To this end, the company has been declared the lowest bidder (L1) for the Next Generation Corvette contract, worth ₹250 billion. This contract is expected to be signed within the next three to four months.

GRSE also anticipates that if the anticipated P7 Bravo contract is also secured, the order book could potentially increase upwards of ₹750 billion within the next 15 to 18 months. While the long-term outlook remains strong, management is also confident of strong growth in the near future.

The company also sees massive future opportunities. Seven high-value projects have been accorded the Approval of Necessity by the DAC, totalling about ₹1.5 trillion. This includes the P7 Bravo project (₹700 billion), for which the Request for Proposal (RFP) is expected during Q4 of FY26, the Mine Countermeasure Vessels (₹320 billion), and the Landing Platform Docks (₹350 billion).

New Opportunities in Commercial and Export Shipbuilding

GRSE plans to enter the competitive commercial shipbuilding sector to meet both domestic and global demands. Targeted non-defence products include ocean ferries (cargo + passenger), multi-purpose vessels, tugs, dredgers, barges, and e-ferries. It is also actively pursuing avenues to increase its geostrategic reach for the export of defense and commercial ships.

To this end, it already achieved a breakthrough by securing export orders for the construction of eight Multi-Purpose Vessels for a German client ($108 million). This gives GRSE a foothold in the competitive European short sea shipping market.

Expansion Plans That Could Redefine Capacity by 2028

GRSE also has ambitious expansion plans. The company has envisioned the establishment of a state-of-the-art greenfield shipyard outside Kolkata by 2028 to enhance in-house capacity. It also plans to strengthen the refit and repair business vertical by actively targeting orders from the Indian Navy, Indian Coast Guard, Ministry of Home Affairs, and state governments.

The company is also building prototypes for Autonomous Vessels and widening its footprint in green vessels, such as the ‘Dheu’ fully electric ferry. This has led to subsequent orders for 13 hybrid ferries from the Government of West Bengal. The company is also working on Hydrogen Fuel Cell Ferry designs and Hybrid Tugs aligned with the Green Tug Transition Plan.

From a financial perspective, revenue increased 38% year-on-year to ₹29.8 billion in the first half of FY26. PAT surged 48% to ₹2.7 billion, as operating margin expanded by 300 bps to 9%. The growth exceeded the company’s own guidance and its historical average of about 30%.

#3 Cochin Shipyard: Core Builder of Complex Vessels

Cochin Shipyard is a leading Indian company in the maritime sector, primarily engaged in shipbuilding and ship repair. The company has been at the forefront of India’s maritime journey for over five decades. The company specialises in shipbuilding (58.8%) and ship repair, which accounted for 42.2% of revenue in FY25.

A Shipbuilder Positioned at the Centre of India’s Maritime Push

Cochin specialises in complex vessel construction, ranging from India’s first indigenous aircraft carrier to world-class hybrid and electric-powered vessels. The shipbuilding portfolio includes Aircraft Carriers, Technology Demonstration Vessels, Hydrographic Survey Vessels (for defence), and Oil Tankers and Passenger Vessels (for commercial sectors).

Order Book Strength and the Pipeline Driving Long-Term Visibility

Looking ahead, Cochin’s forward strategy is encapsulated in its refreshed roadmap, CRUISE 2030 2.0. This aims to solidify the company’s position as a globally competitive, innovation-led leader in the maritime sector. The company plans to double its turnover to Rs 120 billion by FY2031 by growing at a rate of 10-12% over the next 5-10 years or more.

Cochin’s current order book (Q1 FY26) stood at ₹211 billion, providing revenue visibility of about 4 years. Additionally, the company has disclosed a shipbuilding order pipeline of about ₹2.8 trillion. The company estimates the defence sector pipeline to be worth ₹2.2 trillion, including the Mine Countermeasure Vessel, P-17 Bravo Vessel, and Landing Platform Dock.

Additionally, the commercial pipeline stands at about ₹650 billion, split between Domestic (₹250 billion) and International (₹400 billion) opportunities. Cochin aims to capture high-value segments in both shipbuilding and ship repair sectors through long-term partnerships.

Strategic Partnerships Shaping the Next Phase of Growth

To this end, the company has signed a long-term association focused on merchant shipbuilding with HD KSOE, South Korea. This partnership aims to jointly explore new building opportunities, share technical expertise, and enhance productivity and capacity utilisation. The benefit of this is expected to fructify over a 3-5 year horizon.

A Memorandum of Understanding was signed to explore the joint development of world-class ship repair clusters in Kochi and Vadinar. This collaboration focuses on the ship repair sector and is expected to be completed within one to two years. Cochin has also signed an MoU with Maersk primarily for ship repair and people skilling.

From a financial perspective, revenue increased by 6.7% year-on-year to ₹19.2 billion in H1FY26, while net profit declined by 22.7% to ₹2.9 billion. Profitability declined due to the absence of high-value and high-margin repair projects of 2 aircraft carriers (INS Vikrant and INS Vikramaditya), which were included in the previous financial year.

Stronger Growth Visibility, Reflected in Premium Valuation

From a valuation perspective, all three companies, Mazagon, GRSE, and Cochin, are trading at more than double their median price-to-earnings multiples. Relative to industry P/E, GRSE offers a better margin of safety as it trades at a discount. Mazagon is broadly in line with peers, while Cochin Shipyard continues to command a premium. This implies that all these companies factor in the near-term order book, and now execution remains the key.

Valuation Comparison (X)

| Company | Existing P/E | 5-Year Median | Industry P/E |

| Mazagon | 48.1 | 21.1 | 48.1 |

| Garden Reach | 53.8 | 26.4 | 66.9 |

| Cochin Shipyard | 59.9 | 22.0 | 48.1 |

That said, India’s shipbuilding story is entering a decisive phase. As China accelerates its maritime buildup, New Delhi’s push to strengthen coastal defence and expand naval capabilities is creating a multi-year opportunity for domestic shipyards. Mazagon, GRSE, and Cochin are positioned at the centre of this shift, supported by expanding order books and long-cycle visibility. While valuations have moved up, the sector’s growth runway, policy alignment, and rising global relevance continue to underpin investor interest.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data was not available have we used an alternate but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.