There are times in the market when a company’s story doesn’t change because of a new product or a turnaround in the economy. But they are because of the people at the top. Leadership, after all, shapes strategy, capital allocation, and culture, and when that shifts, it can quietly reset the company’s entire trajectory.

Over the last few years, a handful of once-overlooked businesses have seen precisely this kind of transformation. These companies struggled with slow or stalled growth, low margins, and profitability, eroding investor confidence. However, when new management came in, often with a more precise focus, lean operations, and a long-term outlook, the story changed.

What followed wasn’t just a recovery in numbers but a revival in narrative. Balance sheets strengthened, businesses refocused on their core strengths, and shareholders who stayed patient witnessed extraordinary wealth creation. In this story, we’ll look at three companies where a change in leadership led to a multibagger rally.

#1 CG Power and Industrial: From crisis to comeback

CG Power is an 86-year-old engineering group and a leader in the electrical engineering industry. The company operates in two business lines: Industrial Systems and Power Systems. It manufactures traction motors, propulsion systems, signaling relays, and other components for Indian Railways.

Additionally, it manufactures induction motors, drives, transformers, switchgear, and other products for the industrial and power sectors. It has also forayed into the consumer appliance market, offering products such as fans, pumps, and water heaters.

CG Power’s turnaround under the Murugappa Group

Its financials began to deteriorate a decade ago, as its revenue fell from ₹136.3 billion in FY14 to ₹51.5 billion by FY20. The company was later found to be involved in accounting irregularities. Later, in 2020, the Murugappa Group took over CG Power, infused ₹7 billion, and appointed directors to its board. The group entity Tube Investments of India holds a 57.9% controlling stake in the company.

The company subsequently rebounded, with revenue growing 1.9x from ₹51.6.7 billion in FY20 to approximately ₹99.1 billion in FY25. Its profitability also rebounded from a loss of ₹13.2 billion in FY20 to a net profit of ₹9.7 billion in FY25. As a result, the stock price has returned approximately 31.4x over the past 5 years.

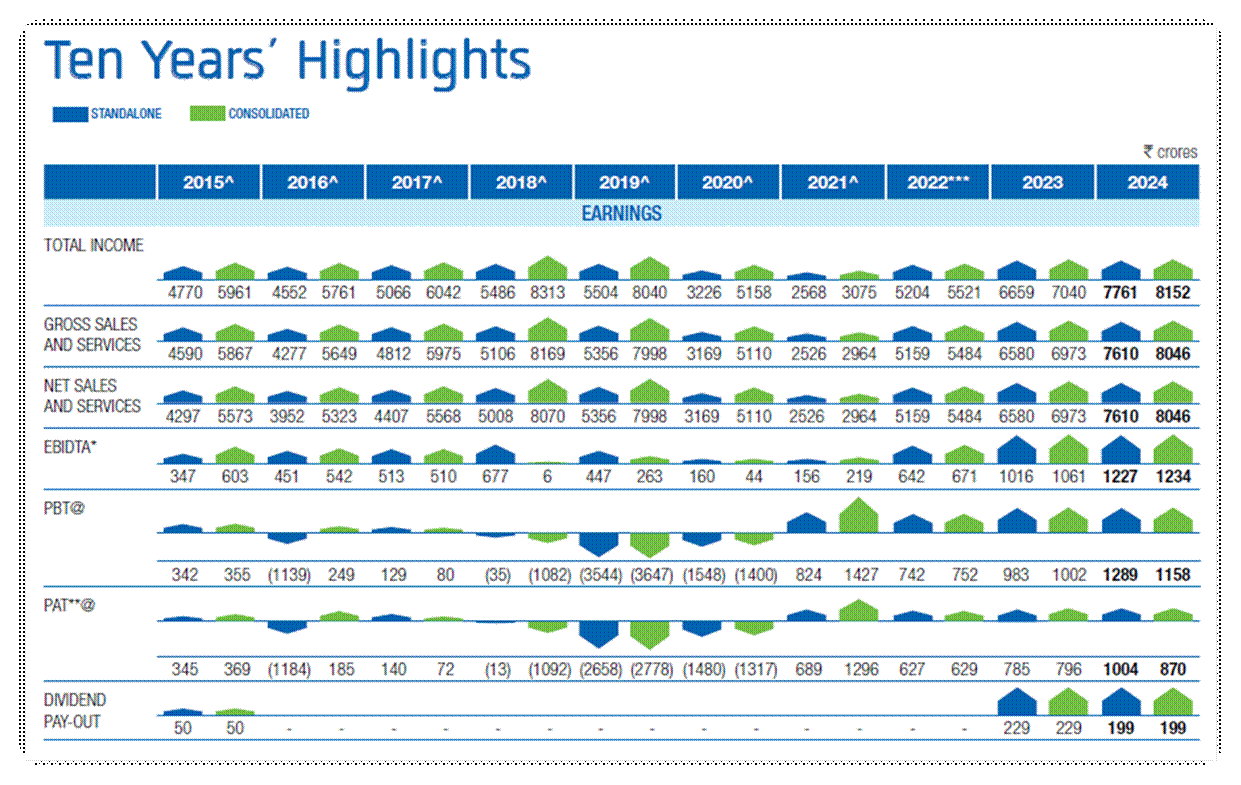

CG Power 10-Year Financial Performance

In the first quarter of FY26, the industrial segment dominated, accounting for 59.6% of revenue, with the remaining 40.4% coming from the power segment. However, the power business is more profitable, with margins of 22% compared to 11.6% in the industrial segment.

Strong performance across segments in Q1FY26

During the quarter, revenue from the industrial segment grew 16% year-on-year (YoY) to ₹15.7 billion. However, profit before interest and tax (PBIT) declined 6% as margins dropped by 250 bps to 11.6%. Rising commodity prices and increased investments in the consumer business contributed to the margin contraction.

On the other hand, the power sector revenue rose strongly by 43% to ₹10.7 billion. Margins also climbed 90 bps to 22%, driven by better price realization and operating leverage. As a result, PBIT grew 51% to ₹7.1 billion.

At the consolidated level, revenue rose 29% to ₹28.8 billion, driven by both segments. However, blended margins declined slightly by 200 bps to 14.2%, mainly due to pressure in the industrial business. Net profit rose 11% to ₹2.6 billion. Return on Capital Employed (RoCE) for the quarter was 33%.

Strong order book supports growth outlook.

Looking ahead, CG Power aims to maintain a robust growth rate, supported by a strong order book, which provides visibility into revenue growth. The total order book stood at ₹130.7 billion (up 82% YoY), providing revenue visibility for about 1.5 years on FY25 revenues.

The industrial segment had an order backlog of ₹29.2 billion (+19% YoY). Meanwhile, the power segment had an order backlog of ₹90.5 billion (+97%). The company is expected to benefit from the expanding power transformer market. It is investing ₹7.1 billion to set up a 45,000 megavolt-ampere transformer manufacturing unit.

With this expansion, CG Power aims to cater to growing domestic and export demand, further strengthening its market position. It also plans to enhance its export capabilities, particularly in the power segment. Additionally, the company is developing electric vehicle motors and controllers to leverage electric mobility and energy efficiency technology solutions.

The company trades at a price-to-equity (P/E) multiple of 117x, well-above its 10-year median of 76.4x, and industry (49.7x).

#2 Fortis Healthcare: A healing touch through leadership change

Fortis Healthcare is India’s leading integrated healthcare provider. As of 31 March 2025, Fortis manages a network of 27 healthcare centers with approximately 4,750 operational beds. It also operates a diagnostics business through its subsidiary, Agileus Diagnostics, which is India’s largest diagnostic services provider.

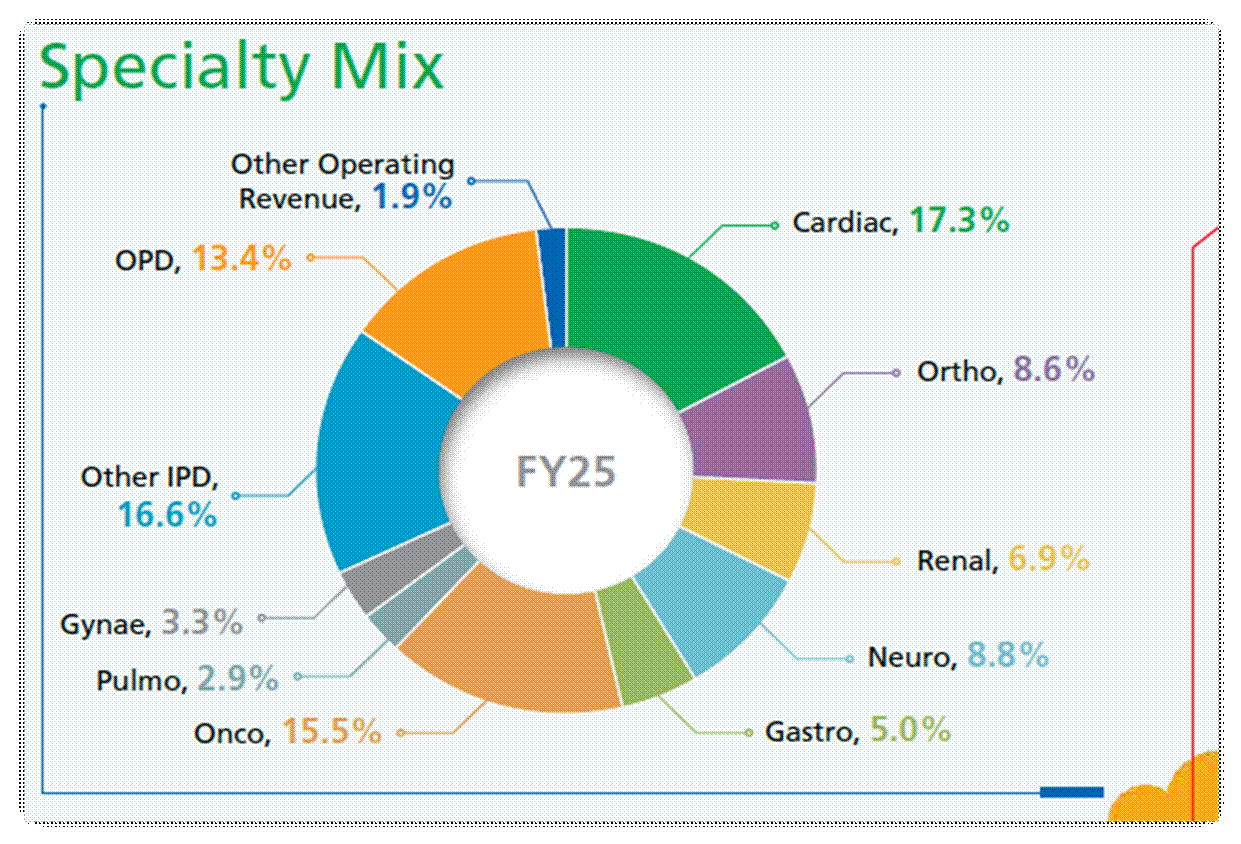

The company’s core focus remains on specialized medical care, including Cardiology, Oncology, Orthopedics, Neurosciences, Gastro, and Renal Sciences, which contributed 62% to the total hospital revenues in FY25. The overall hospital occupancy stood at 69% in FY25.

Fortis Revenue-Mix

How IHH’s entry reshaped Fortis Healthcare

Seven years ago, Fortis, led by its former promoters, the Singh brothers, struggled with governance issues and financial troubles. Then, in 2018, Malaysia-based IHH Healthcare Berhad acquired a 31.1% stake in Fortis for about ₹40 billion. That’s where the turnaround started, as under IHH, Fortis’ governance, cost structure, and hospital efficiency improved.

Profitability takes center stage as margins expand

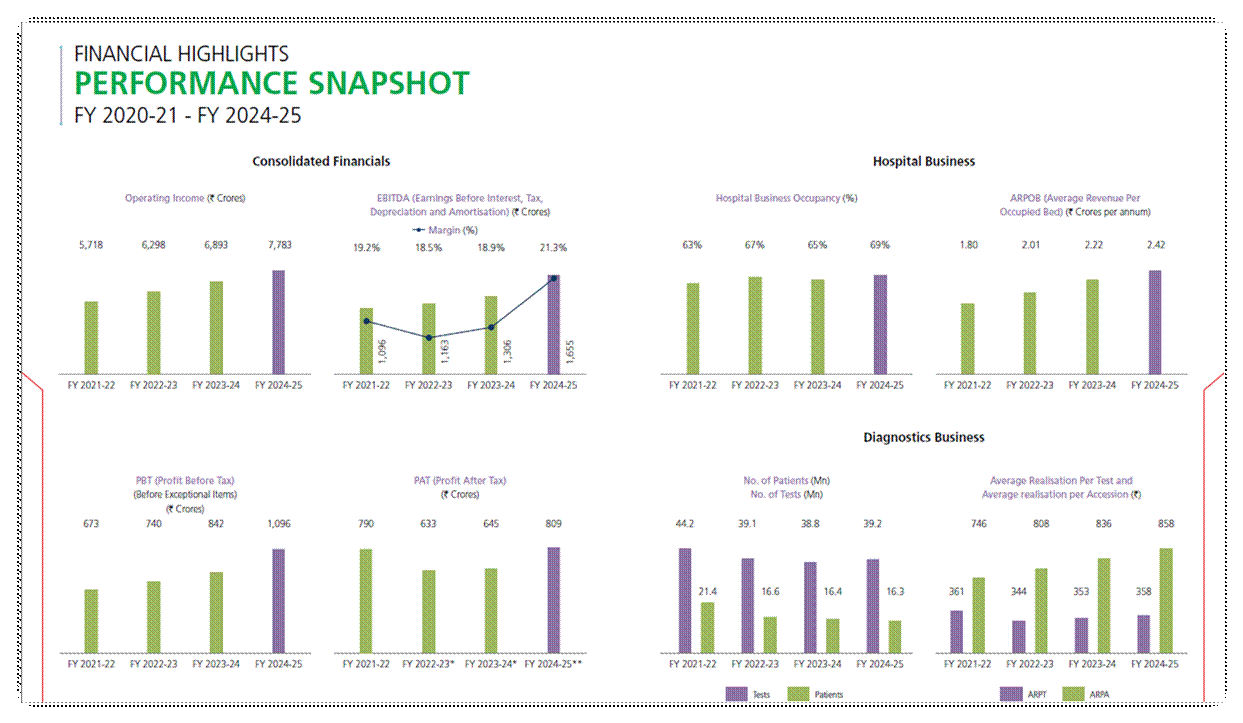

Fortis’s operating income has surged from ₹44.6 billion in FY19 to ₹77.8 billion in FY25. While the revenue growth has been slower, a bigger impact has been on margins and profitability. Operating margins increased from 5% to 21%, while it swung from a loss (loss of ₹224 crore) to a profit of ₹8.1 billion during the period. Its RoCE has doubled to 12%.

Fortis Financial Performance (FY21-25)

Consequently, its share price has returned 7.5x in the last 5-years.

In Q1FY26, revenue grew 16.6% year-over-year to ₹21.7 billion, while margins expanded 430 basis points to 23.4%. Net profit increased 53.4% to ₹2.7 billion. This increase was driven by higher occupancy, up 200 basis points to 69%. Average revenue per operating bed per year (ARPOB) also improved.

Growth momentum to continue with capacity expansion

Looking ahead, Fortis is confident of maintaining this growth trajectory. Fortis has recently signed an operation and maintenance (O&M) services agreement with Gleneagles India. This agreement entitles Fortis to receive a service fee of 3% of net revenue. The earnings from this agreement are expected to improve the consolidated margin by roughly 20-30 bps.

In addition, Fortis is on track to add about 900 beds in FY26, including those from the recently acquired hospital in Jalandhar. About 50% of these beds are expected to be operationalized in FY26, with a quick ramp-up likely as they are primarily brownfield projects.

This is expected to aid revenue growth. In FY27, Fortis expects to add additional revenue from 600 beds, translating into a revenue addition of around ₹15 billion based on the current ARPOB.

Valuation-wise, Fortis is now trading at an EV/EBITDA multiple of 46.3x, double the 10-year median of 23.9x. After the recent rerating, it is also trading above the industry multiple of 26.7x.

#3 Nuvama Wealth Management: Revival Through a Demerger and New Promoter

Nuvama was a part of Edelweiss Financial Services. Edelweiss particularly suffered from high debt, following the Non-Banking Financial Crisis in India. Then, PAG, an Asia-focused private equity firm, acquired a 61.5% controlling stake in Edelweiss Wealth Management for ₹23.6 billion in 2020.

PAG Acquisition Sparks Strategic Shift

This strategic move marked a significant shift in the company’s direction. Following the acquisition, Nuvama demerged from Edelweiss Financial Services, resulting in its listing in September 2023. Subsequently, Nuvama has doubled investors’ money over the past two years.

Nuvama today ranks second amongst India’s wealth management companies, serving high-net-worth individuals (HNIs), ultra-HNIs, affluent individuals, corporates, and individuals. It provides financial services, including product distribution, wealth advisory, investment banking, and asset management services.

Rapid Growth Across Client Assets and Profits

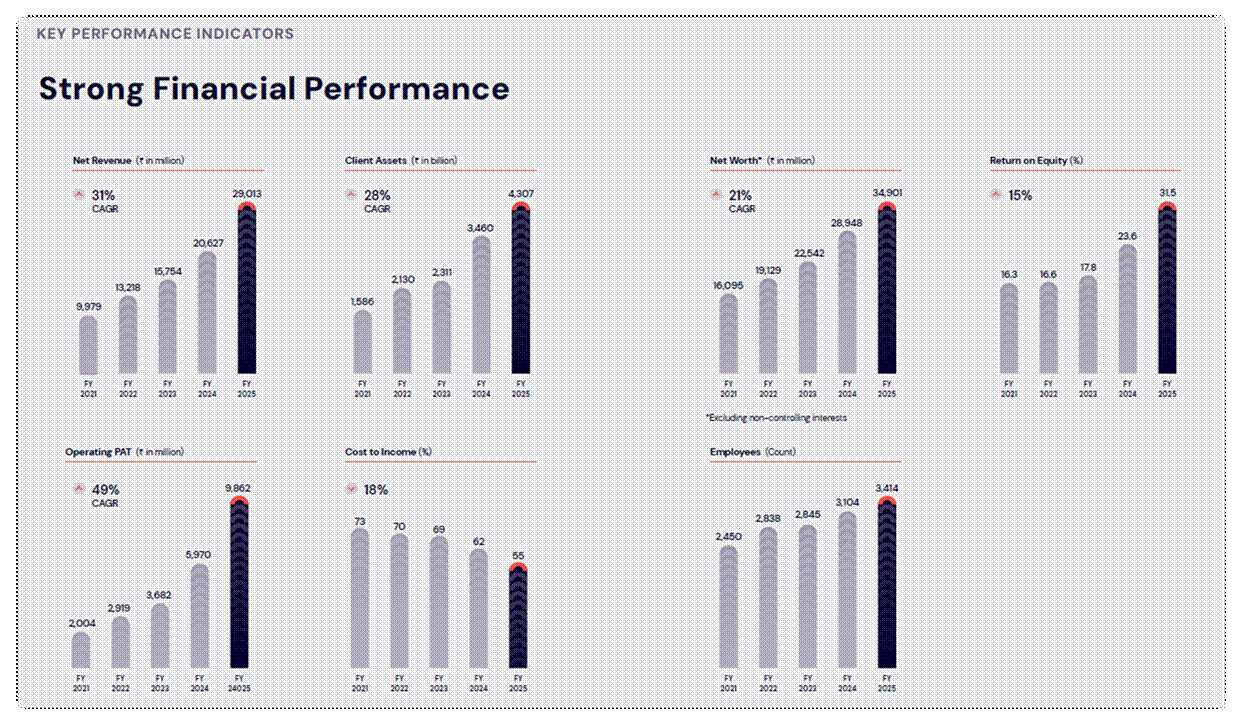

As of Q1FY26, Nuvama manages total client assets of ₹4.6 trillion (up 2.7x from FY21), which includes asset management (₹3.2 trillion), asset services (₹1.2 trillion), and asset management (₹11.8 billion). Net revenue almost tripled from just about ₹10 billion in FY21 to ₹29 billion in FY25. Net profit, on the other hand, surged fivefold to ₹9.8 billion during the period.

Nuvama Financial Performance

Much of this growth is led by its largest vertical, wealth management, driven by strong demand from growing high-net-worth individuals. The company is benefitting from operating leverage, as its cost-to-income ratio decreased by 1,800 basis points to 55% during this period. RoE expanded by 800 bps to 31.5% in FY25.

Expanding Wealth Management to Meet Rising Demand

Looking ahead, the company plans to rapidly expand its wealth management business in the coming years, with 20% annual growth in client assets in the coming years. To meet the strong demand, the number of relationship managers, which currently stands at 1,200-1,300, is projected to increase to between 3,000-4,000 over the next 3-4 years.

Valuation-wise, Nuvama is now trading at a P/E of 25x, in line with its 2-year median of 26.7x, and above the industry P/E of 16.6x.

Bottomline

Across these three stories, a common thread is clear: leadership matters. Whether it was Murugappa Group steering CG Power out of financial and operational turmoil, IHH Healthcare bringing governance and efficiency to Fortis, or PAG driving a demerger-led revival at Nuvama, decisive and focused management reshaped the trajectory of each company.

These turnarounds were not just about short-term fixes. They involved strategic investments, operational restructuring, and strong governance that eventually translated into topline and bottom-line, creating significant wealth. Hence, a capable management team can be just as powerful a catalyst for growth as any product or sector tailwind.

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data was not available have we used an alternate but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article. The website managers, their employees, and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities, or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.