The world is transitioning to clean energy, driving demand for renewable energy, electric vehicles, and lithium-ion batteries. In the EV segment, government policies such as the Production-Based Incentive Scheme and the PM e-Drive Scheme, along with a lower GST rate of 5%, are driving demand for EVs. The government aims to increase the share of EVs in total passenger vehicle sales to 30% by FY30.

This, in turn, is boosting demand for sub-sectors such as lithium-ion batteries. CareEdge Ratings estimates that demand for lithium-ion batteries in India will grow rapidly to 54 gigawatt hours (GWh) by FY27 and 127 GWh by FY30. This is in line with India’s ambitious target of meeting 50% of the country’s energy needs from renewable energy by 2030. It is worth noting that India currently exports lithium-ion batteries, which are expected to decline to 20% by FY27.

This growing demand for advanced battery technologies is opening up a new growth avenue for chemical companies that supply critical inputs to the battery value chain. Similarly, three chemical companies are eyeing the lithium-ion battery sector.

#1 PCBL: From carbon black to battery tech

PCBL Chemicals is India’s leading carbon black manufacturer and a diversified specialty and performance chemicals company. It is a flagship unit of the RP-Sanjiv Goenka Group. PCBL is India’s largest carbon black manufacturer and the seventh largest globally. The company offers a diversified, innovation-led portfolio across four core sectors.

This includes tyres (rubber black), performance chemicals, specialty chemicals, and nano-silicon (battery chemicals). It offers over 110 customized product grades and serves customers in over 50 countries across six continents. Its carbon black production capacity is 7.9 lakh metric tons per year, with plans to expand to 1 million metric ton per year by FY28.

PCBL’s next growth frontier in battery materials

PCBL Chemicals is expanding into the rapidly growing battery chemicals sector, focusing on next-generation energy materials and conductive solutions. It is the first company globally to develop all three advanced technologies: super-conductive carbon, nano-silicon, and acetyl black for applications in conductive solutions & next-generation batteries.

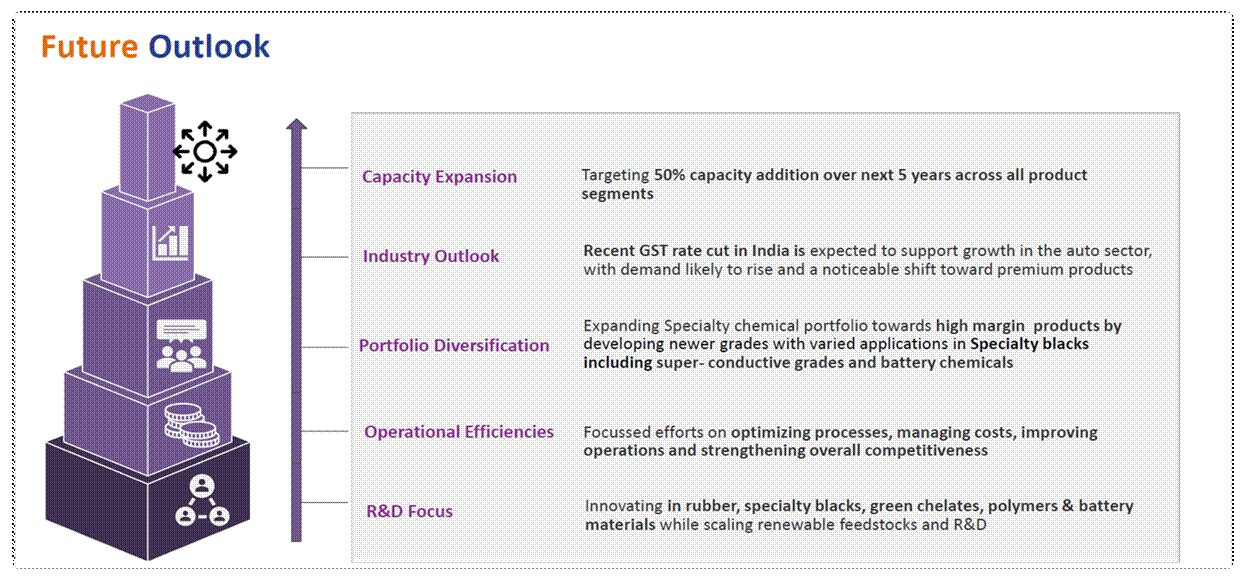

PCBL Future Outlook

This shift positions the company as a key player in ancillary services for electric mobility and green energy storage systems.

Nano-Silicon bet for battery edge

PCBL entered the battery materials segment through Nanovace Technologies, a joint venture (JV) with Kindia Pty of Australia. Nanovace develops nano-silicon-based anode materials for lithium-ion batteries. Notably, nano-silicon is emerging as a next-generation anode material, offering energy densities about 10X greater than the theoretical capacity of graphite.

It is designed to significantly improve battery performance, increase energy density, and extend battery life. The use of nano-silicon can also increase battery range by 25-100% and increase charging speeds by up to 4X. A pilot-scale facility for nano-silicon is under construction at Palej, which is expected to be operational by 2025 end. The facility is expected to be commercialized between FY27-28.

Acetyl black plant adds depth

In addition, PCBL is also setting up a manufacturing facility for acetyl black, a high-conductivity material critical for battery electrodes. The plant with an annual capacity of 4,000 metric tonnes is expected to go live in FY27. It has India’s first backward-integrated acetylene black plant at Mundra.

To support this initiative, PCBL has also signed a technology transfer agreement with Ningxia Jinhua Chemical of China. Note that acetylene black is used in high-performance applications such as battery electrodes, semiconductors, high-voltage cables, and conductive polymers.

From a financial perspective, revenue remained flat at ₹21.6 billion in Q2FY26, as specialty black chemicals volumes grew only 2%. EBITDA (earnings before interest, taxes, depreciation, and amortization) fell 24.7% to ₹2.8 billion. EBITDA margin declined 400 basis points (bps) to 13%, leading to a 50.4% drop in profit after tax (PAT) to ₹620 million.

#2 Neogen chemicals: Betting big on electrolytes

Neogen Chemicals is a reputable specialty chemicals manufacturer, focused exclusively on bromine and lithium-based products. It is a leading manufacturer of bromine and lithium-based specialty chemicals, with a foundation in organic and inorganic chemistry. Neogen portfolio spans over 246 products, for sectors across pharma, agrochemicals, and battery chemicals.

Battery chemicals take centre stage

Battery chemicals are a key strategic focus and high-growth opportunity for Neogen Chemicals, particularly through its wholly-owned subsidiary, Neogen Ionics. This expansion is driven by the growing global shift towards electric mobility (EVs) and renewable energy storage, driving demand for high-performance and locally sourced lithium-based chemicals.

Gujarat facility to lead capacity

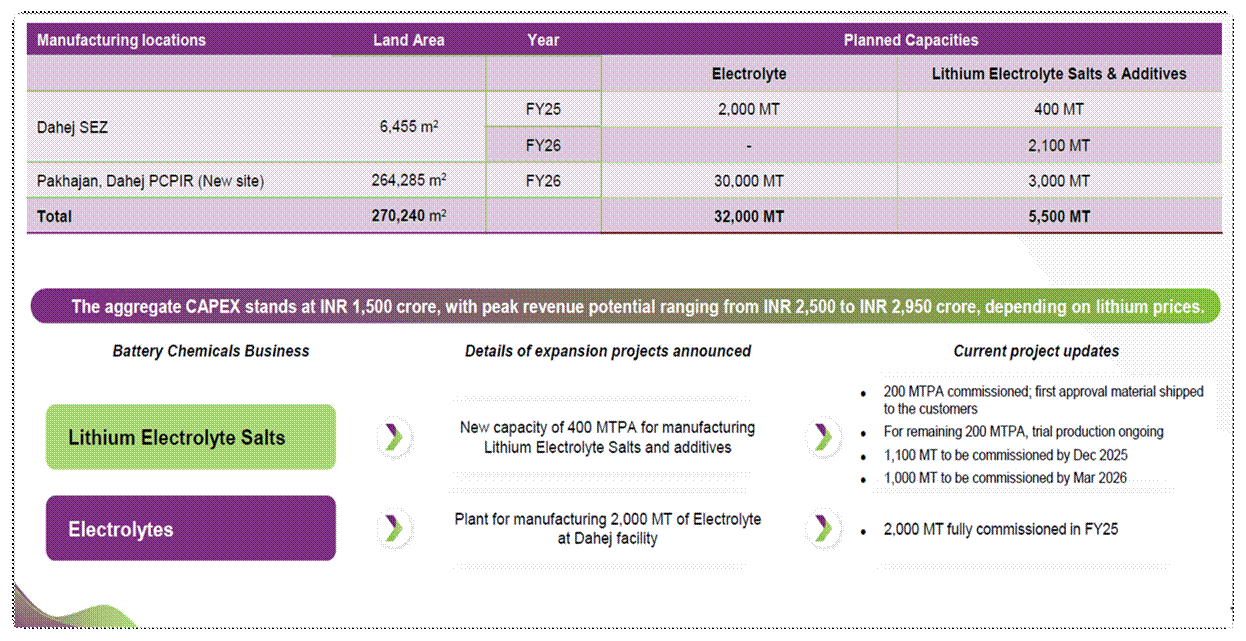

Neogen is establishing a large manufacturing facility for battery chemicals in Gujarat. The total planned capacity across all locations is 32,000 metric tons for electrolytes and 5,500 metric tons for lithium electrolyte salts and additives. This facility is projected to become India’s largest integrated facility for battery materials.

Neogen Capacity Expansion Details

This capacity, with an investment of ₹15 billion, is expected to be operational early next year (in FY26). Note that electrolytes, lithium electrolyte salts, and additives are key components for lithium electrolytes. Additionally, a 2,000 metric tonne per annum electrolytes capacity is already commissioned in FY25. This facility is currently undergoing testing.

MU Ionic partnership strengthens edge

For lithium electrolyte, Neogen has an exclusive partnership and technology license from Japan’s MU Ionic, a global leader in lithium electrolyte manufacturing. This license provides Neogen with a significant leadership advantage in the supply of high-quality electrolytes.

From a financial perspective, revenue grew only 4% year-on-year to ₹1.8 billion in Q1 FY26, due to the Dahej plant closure for the entire quarter. 71% of total revenue came from the domestic market and 29% from exports. EBITDA also grew only 2% to ₹315 million, while margins fell 20 basis points to 16.9%. Profit after tax (PAT) declined 11% to ₹103 million.

#3 Balaji Amines: The niche DMC advantage

Balaji Amines is a leading Indian chemical company specializing in aliphatic amines and specialty fine chemicals. It is India’s largest manufacturer of aliphatic amines and the third largest producer of methylamine. Its key chemical intermediates are vital inputs for pharmaceuticals, agrochemicals, rubber chemicals, solvents, resins, and corrosion control.

Electronic-grade DMC powers EV growth

The company serves several critical industrial applications, with pharmaceuticals accounting for 51% and agrochemicals accounting for 26%. Among its products, dimethyl carbonate (DMC) is a key chemical supporting the battery sector and the electric vehicle sector.

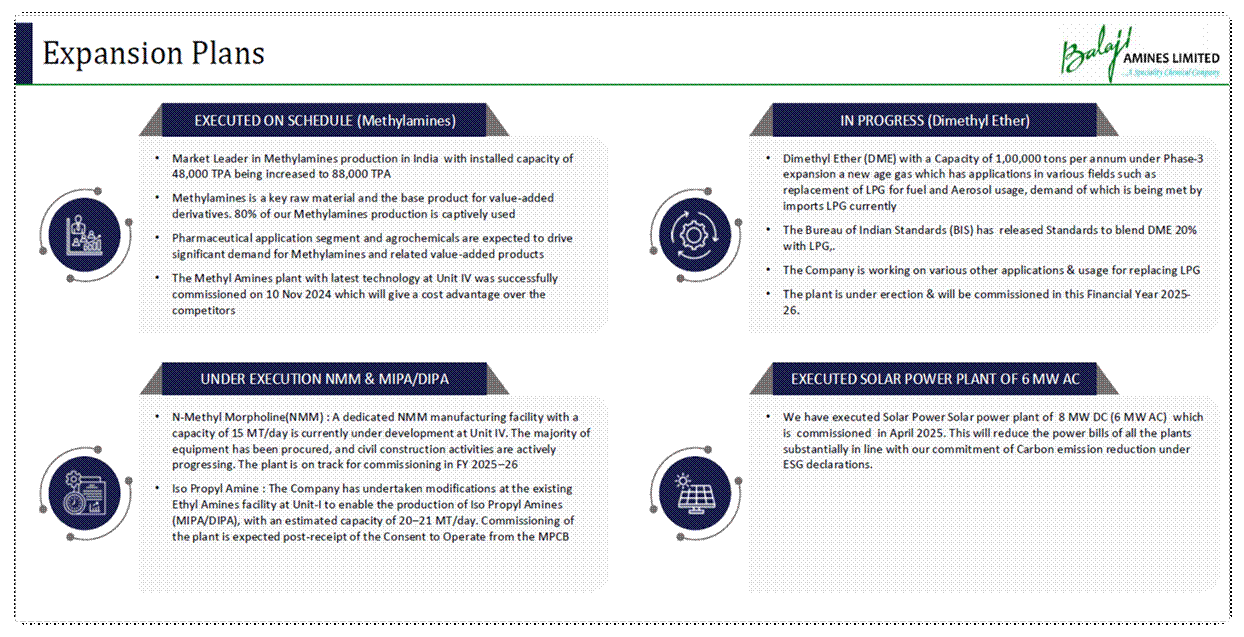

Balaji Amines Capacity Expansion Details

Balaji upgraded its existing Dimethyl Carbonate (DMC) plant by integrating advanced equipment specifically for producing Electronic Grade DMC. This new production line was commissioned successfully on 28 May 2025. This facility aims to address the rising demand coming from the EV battery segment.

Balaji is the only manufacturer of electronic-grade DMC in India, which provides it with a competitive advantage. The company believes this will open up attractive growth opportunities in the clean mobility ecosystem.

Aiming ₹20 billion revenue milestone

On the financial front, revenue declined 7% year-over-year to ₹3.6 billion in Q1FY26. EBITDA fell 14% to ₹640 million, while margins decreased 200 basis points to 17%. PAT, on the other hand, fell 20% to ₹37 million. With these expansion plans, Balaji plans to achieve revenue of ₹20 billion in the next 2 years from ₹13.9 billion in FY25.

Is growth already priced in?

From a valuation perspective, PCBL is trading at a price-to-earnings (P/E) multiple of 39.7x, which is double the 10-year median (16.6x) but in line with the industry (37.5x). Neogen trades at 98 P/E, which is at a premium to both the 5-year median of 82.8x and the industry (32.9x). On the other hand, Balaji’s P/E of 30 aligns with the industry, but is at a premium to its 10-year median of 22.5x.

Valuation Comparison (X)

| Company | P/E | 10-Year Median | Industry Median |

| PCBL | 39.7 | 16.6 | 37.5 |

| Neogen | 98.0 | 82.8 (5-Year) | 32.9 |

| Balaji Amines | 30.0 | 22.5 |

India’s battery opportunity is creating new growth avenues beyond cell manufacturing, drawing specialty chemical players into the spotlight. PCBL Chemicals, Neogen Chemicals, and Balaji Amines are among the early movers. Their bets align well with India’s clean energy goals, but valuations already reflect much of the optimism. The real test now lies in execution, scaling new chemistries profitably, and delivering on commercialization timelines.

Disclaimer

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data was not available have we used an alternate but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article. The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities, or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.