")

The market is weak and has been in a depressed state amid a prolonged consolidation for over a year and a half. Since then, many portfolios have been in the red, and returns have been almost negligible to negative. But a select few stocks have still outperformed the broader market and delivered impressive returns. Consider these 3 companies whose share prices have increased by up to four times. Imagine if you had invested ₹1 lakh exactly two years ago, and by now you would have had ₹5 lakh.

Undoubtedly, such stocks are hard to find, and even if you do, you need the patience to sit tight. Industry tailwinds, government focus, consistent market share gains, and strong and consistent financial performance often drive such returns. But what’s really behind their rise? And after such a steep rally, is there still steam left?

Let’s take a look.

#1 Hitachi Energy India: Power sector tailwinds turned into fivefold returns.

Hitachi Energy provides products, systems, software, and service solutions across the power value chain. The portfolio encompasses a diverse range of high-voltage products, transformers, grid automation solutions, power quality products, and systems.

Sector Tailwinds Powering the Rally

Hitachi’s strong growth over the last two years was fueled by a growing order book, strong revenue visibility, a favourable product mix and a strong execution. The energy transition towards renewable energy and growing power demand are creating investment opportunities in key sectors like High-Voltage Direct Current (HVDC), data centres and electric transportation.

The company has maintained a strong presence in the renewable energy sector, with orders doubling in fiscal 2025. India’s ambitious target of achieving 500 GW of non-fossil capacity by 2030 is driving demand for grid strengthening solutions. The company maintained leadership in core segments, including HVDC.

The data centre sector has emerged as a significant opportunity, with orders growing 1.5 times in FY25. The company’s offerings, including substations, GIS, automation, and transformers, are poised to meet the growing demand in this sector. Hitachi will further benefit from its presence in the transmission sector.

This is supported by the planned investment of over ₹1 trillion on the Inter-State Transmission System network alone in the next two years to meet the 2027 National Electricity Policy Target. Industry tailwind translated into strong financial growth.

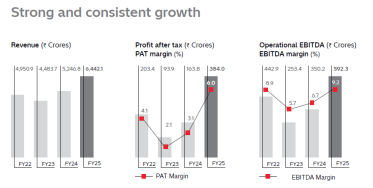

Earnings Momentum Strengthens with Expanding Margins

Hitachi’s revenue rose by 43.7% (absolute) in the last two years, from ₹44.8 billion in FY23 to ₹64.4 billion in FY25. Profit after tax has grown fourfold to ₹3.8 billion from ₹939 million during this period. Operating margin jumped with margin expansion from 5.7% to 9.2%, as operating leverage kicked in.

Strong Financial Growth

Robust performance continues in FY26 too. Revenue grew 15% to ₹33.1 billion in the first half of FY26, up from ₹28.8 billion in the same period last year. On the other hand, PAT increased 6.4 times to ₹3.9 billion, while margins more than doubled to 16%. Its share price has surged fivefold from about ₹4,000 on 6 November 2023 to ₹20,890 on 7 November 2025.

Capacity Expansion and Industry Visibility Keep Growth Intact

Looking ahead, to capitalise on strong demand, Hitachi is investing ₹20 billion to expand its existing capacity and broaden its product portfolio. These new capacities are expected to be operational within the next 18 months. It’s all vertical is poised for consistent growth, with data centres emerging as key segments.

#2 Force Motors: From focused restructuring to a fivefold rally.

Force Motors is India’s largest van manufacturer with a fully integrated automobile manufacturing system. It specialises in the design, development and production of light commercial vehicles (LCVs), multi-utility vehicles (MUVs), small commercial vehicles (SCVs) and super speciality vehicles.

Focused Restructuring Sparks a Strong Turnaround

Its rally is being driven by sustained, consistent growth in both topline and bottom line for 10 consecutive quarters, after a turnaround in FY24. In FY25, Force achieved its highest-ever four-wheeler sales and posted record exports. This came after a little restructuring after it exited the tractor and three-wheeler businesses to focus on its strength–the traveller segment.

New Product Launches and Exports Drive Record Growth

The company benefited from the market launch of new products like the all-new Urbania van and the new Gurkha product offerings. These new products achieved very good traction in the market. Meanwhile, the flagship Traveller platform maintained its market leadership. On top of that, its component business also showed very good growth.

In the auto ancillaries business, it also supplies engines and axles to Mercedes-Benz India and engines and cooling modules to BMW India, under a long-term partnership. It also operates a joint venture with Rolls-Royce Power Systems AG.

Sharper Margins and Market Share Gains Fuel a 5X Rally

Consolidated revenue grew 60.5% over the past two years to ₹80.7 billion in FY25 from ₹50.3 billion in FY23. PAT increased over fivefold to ₹8 billion from just ₹1.3 billion in this period as operating margins more than doubled from mid-single digits of 6% to 16%. This performance was driven by tight cost discipline and market share gain backed by new launches.

As a result of this performance, its share price has jumped 5.4X from ₹3,376 on 25 October 2023 to ₹18,300 now. The momentum is intact in FY26, too. Revenue grew 21.8% year-on-year to ₹22.9 billion in Q1FY26, while PAT grew 51.7% to ₹1.7 billion.

Looking ahead, the company aims to be among the top 10 van manufacturers in the world and become a leading provider of shared transportation solutions. It believes that the adoption of electric vehicles in commercial vehicles is slow. However, it continues to invest in multi-fuel platforms.

#3 Neuland Laboratories: API Tailwind Fueled Neuland’s 4.5x rally.

Neuland Laboratories is a dedicated Active Pharmaceutical Ingredient (API) solutions provider. The company operates through two business segments: Custom Manufacturing Solutions (CMS) and Generic Drug Substances (GDS). It serves customers globally in 80+ countries.

From a niche API maker to a global player

As of FY25, 82% of the company’s total revenue was derived from exports, primarily to the US and Europe, which account for over 89% of its total exports. It holds a robust regulatory profile, with over 990 DMFs filed worldwide, including 72 Active US DMFs, 499 European DMFs, and filings across numerous other geographies such as Canada, Korea, Japan, and Australia.

CMS is a high-margin segment, contributing 42% to revenue in FY25 and 44% in Q1 FY26. It supports the development and manufacture of New Chemical Entity (NCE) APIs for biotech and pharmaceutical innovators, offering services from the Investigational New Drug stage through to commercial supplies.

GDS provides generic non-exclusive APIs, with a portfolio of over 100 APIs across 10 diverse therapeutic areas. GDS comprises two sub-segments. Prime APIs, which are large-volume and mature molecules, contribute 33% of revenue in FY25. Speciality APIs, which are low-volume, complex molecules with limited competition, contribute 18% of revenue in FY25.

Margins and earnings surge as new capacities come onstream.

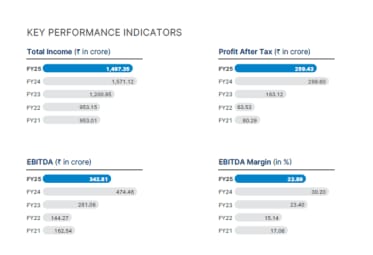

Neuland’s total revenue has grown about 25% in the last two years, from ₹12 billion in FY23 to ₹14.8 billion in FY25. PAT surged 59% to ₹2.6 billion, from ₹1.6 billion during the period. This growth was driven by margin expansion as new capacity drove operating profit.

Neulend’s Financial Performance

Consequently, its share price has surged 4.5X from ₹4,000 on 6 November to ₹18,000 now.

Neuland Laboratories Share Price

Peptide Push Sets the Stage for the Next Growth Phase.

Looking ahead, the company aims to deliver a 20% compounded annual growth rate over three to five years. This is expected to be driven by scaling commercial CMS programs, continued influx of new business from biotech customers, and the successful commercialisation of new capacities at Unit-II.

As a result, management anticipates continued buoyancy in the CMS business, expecting it to drive growth over the short, medium, and long term. It continues to see a big influx of new business from both existing and new customers. This new business is expected to fructify in the numbers over the course of the current and next financial year.

Neuland is making a large allocation to peptides, which is a high-growth opportunity globally. It is investing ₹2.5 billion in a new, large-scale, multi-product peptide facility. This expansion will increase reactor capacity from 0.5 KL to 6.37 KL by FY27. This will provide greater revenue momentum from the latter half of FY26.

Market optimism pushes valuations to the edge.

Valuation-wise, all of these stocks appear to have risen sharply, leaving little room for error. Hitachi is trading below its 5-year median price-earnings multiple, but more than double the industry. Neuland’s valuation is about 4 times both the 5-year median and the industry. Force Motors is near its median and industry valuations, offering comfort.

Valuation Comparison (X)

| Company | P/E | 5-Year Median P/E | Industry P/E |

| Hitachi Energy | 130.0 | 186 | 48.9 |

| Force Motors | 29.2 | 29.3 | 33.8 |

| Neuland Lab | 117.0 | 29.3 | 32.8 |

Despite the market’s prolonged weakness, the sharp rallies in Hitachi Energy, Force Motors, and Neuland Laboratories show how focused execution and industry tailwinds can still create multi-baggers. Each of them has leveraged its niche— power infrastructure, commercial vehicles, and APIs— to deliver strong earnings and market leadership. Yet, with valuations now stretched, boarding now could be risky.

Disclaimer

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data was not available have we used an alternate but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.