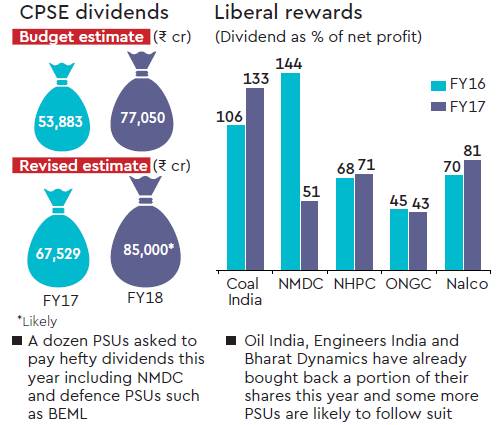

“Some of the PSUs have been asked to even pay more than 100% of their (anticipated) profit this year (as dividend),” an official with knowledge of the matter told FE. In a meeting convened recently by the government, about a dozen CPSEs, including NMDC and defence undertakings, were asked to scale up dividend payments. In FY17 too, the payouts exceeded the net profits at some state-run firms — Coal India, for instance, paid Rs 12,353 crore or 133% of its net profit in the year, after the government asked all cash-rich CPSEs to pay liberal dividends to bridge the revenue gap.

NMDC had paid 144% and 51% of its net profit as dividend in FY16 and FY17, respectively. Nalco, ONGC, NHPC and Bharat Electronics are among the other companies which announced huge dividends in the last two years (see chart). The government’s guidelines on dividends say every CPSE will pay a minimum annual dividend of 30% of profit after tax or 5% of net worth. The revised estimate of CPSE dividend of Rs 77,000 crore was 42% higher than budget estimate in FY17 and more than double of Rs 30,616 crore received in FY16. While sources said dividends from CPSEs could be at least Rs 17,000 crore more than the budget estimate this year, there are murmurs of protest among some firms about such hefty dividends being sought year after year, as these outgoes will hit their future capex. Though much depleted from the level two years ago, CPSEs that still have respectable surplus include Coal India (Rs 31,664 crore), BHEL (Rs 10,492 crore), ONGC (Rs 9,510 crore), Oil India (Rs 7,821 crore) and BPCL (Rs 7,557 crore).

Besides higher dividends, the government has also asked some CPSEs to undertake buyback of shares as per the new rules that mandated each CPSE with a net worth of above Rs 2,000 crore and “cash and bank balance” of over Rs 1,000 crore to exercise the option. The process added Rs 18,963 crore to the government’s disinvestment kitty last year. So far this year, Oil India, Engineers India and Bharat Dynamics have exercised the option to buy back shares worth Rs 2,243 crore from the government. More firms are likely to follow this route soon to enrich the government. The Centre’s non-tax receipts were weak in the first half of FY18 due to a Rs 27,341-crore shortfall in RBI dividend this year, even as concerns remain on the tax revenue front as well due to GST’s transitional problems and the likelihood of a slower-than-estimated growth in direct tax revenue, which grew 15.2% till October this fiscal against 17.5% in the April-August period. Despite the heavy dividend outgo, central PSEs and departmental undertakings had bucked the investment famine in the economy by investing about Rs 4 lakh crore in FY17. Their capex this year is budgeted at Rs 3.8 lakh crore but possibly might touch last year’s level.