Kavach – India’s Automatic Train Protection System is positioned as the nervous system for safe railway operations. Kavach is indigenously designed, patented, and manufactured in India, with 14 years of intellectual property rights, which is jointly owned by Indian Railways and three Original Equipment Manufacturers (OEMs).

Kavach automatically applies the brakes when crossing a signal at danger or at excessive speed, helping avoid accidents. Furthermore, it also imposes temporary speed restrictions, increasing flexibility and operational safety. With so many use cases, deployment of Kavach is a key focus area under the Government of India’s Mission Raftar initiative, which aims to enhance both speed and safety in train operations.

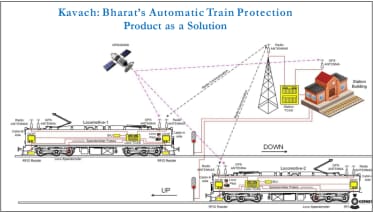

This is how Kavach Operates

India’s total rail network spans approximately 85,000 kilometers. Of this, Indian Railways plans to implement the Kavach project in a phased manner on over 40,000 kilometers. The project’s primary focus is currently on high-density and high-speed corridors, which are expected to be completed by 2030-32. According to Concorde Control Systems, it has a market potential of around ₹450-500 billion.

Several lesser-known companies are quietly gaining from this homegrown technology and could emerge as long-term winners. Let’s take a look at three of them…

#1 Kernex Microsystems (India): Early mover in Kavach technology

Kernex is a leading company engaged in the manufacture and sale of security systems and software services for railways. The company is deeply involved in high-growth sectors such as railway security, telecommunications, and defence. However, its core business is focused on rail security equipment and services, which is its sole business segment.

Riding on the Kavach Opportunity

Kernex’s flagship product is Kavach, India’s automated rail protection system. Its production capacity is 450 Kavach units and 10 level crossing gates per month, which can be expanded to 23 units per month. The company is also actively developing Kavach 4.0, with hardware and software implementation complete.

The company is also developing new generation MIE 3.0 cards based on Microchip/Xilinx FPGAs, which will enable the foundational components for Moving Blocks and Communications-Based Train Control (CBTC) systems. The prototype platform is expected by Q3FY26. Kernex is also developing Network Monitoring Systems and Pulse Generators.

The company’s total order book stood at ₹21.2 billion, which provides revenue visibility of little over ten years, as per the FY25 revenue of ₹1.9 billion. Kernex has also submitted bids totalling ₹30.2 billion, covering 9,505.2 km. Future bids worth ₹8.9 billion are also identified, covering 4,250.9 Kms.

In addition, Kernex has supplied and commissioned Level Crossing (Lx) gates for Egyptian National Railways. The original project scope was shortened from 136 Lx gates to 124 Lx gates. Final Handover (FHO) is ongoing, and completed for 81 out of 85 currently operational sites.

Margins expand as growth accelerates

From a financial perspective, Kernex’s revenue nearly doubled from ₹286.8 million in Q1FY25 to ₹559.3 million in Q1FY26. Operating profit margin expanded 558 basis points (bps) to 22.5%, while net profit doubled to ₹74.1 million from ₹35.7 million in Q1FY25.

#2 HBL Engineering: Key supplier in railway safety push

HBL Engineering manufactures and services a variety of batteries, e-mobility, and other products. The company relies on mobilizing engineering talent to develop both products and customized internal components. This approach reduces capital costs, enabling production even at low initial volumes.

Diverse portfolio anchored in engineering strength

The company’s operations are divided into three distinct business segments: the Industrial Battery segment, the Defense Business segment, and the Industrial Electronics segment. The Industrial Electronics segment includes rail signaling, electric drive train (motors and other vehicle electronics for trucks), and other industrial electronics products.

Early mover in India’s Kavach journey

HBL began developing Kavach in 2005 in response to a request from the Research Designs and Standards Organization (RDSO) for investment in developing an indigenous rail collision avoidance system. However, no initial funding was received from RDSO. HBL successfully demonstrated the concept, using specification v3.1, on 27 October 2012. Kavach took 20 years to go from idea to success.

After HBL’s initial demonstration, two more companies joined the effort, and interoperability among all three firms had to be established before trial orders were placed by the Railways between 2019 and 2021. Currently, HBL is one of only two companies qualified with the new Version 4.0 specification, out of five companies that received orders from the Railway Ministry.

Electronics segment drives earnings growth

In Q1FY26, the company’s revenue increased 15.7% year-over-year to ₹6.0 billion, driven mainly by the electronics sector. Revenues from the industrial batteries sector remained flat at ₹3.3 billion, accounting for 55% of revenue. The electronics sector revenue increased 106.6% to ₹1.8 billion, contributing 30% of revenue.

The remaining came from defense and aviation batteries. Operating profit margin also expanded by 1100 basis points to 32%, while net profit increased by 78.7% to ₹1.4 billion.

Kavach to anchor long-term growth

HBL aims for total sales of ₹45 billion by FY30, up from ₹19.7 billion in FY25. Rail Signaling, including Kavach, is projected to be the single largest business for HBL by FY30, up from 28.9% of the electronics segment in FY25. The company is seeing a flood of Kavach orders. HBL received contracts worth about ₹40 billion.

The contracts cover 6,980 kilometers of track, 2,425 locomotives, 758 stations, and 460 level crossing gates. Kavach sales are expected to be about ₹13-15 billion per year during FY26, FY27, and FY28, with a potential dip thereafter. HBL believes that the full implementation of the entire Indian Railway network is expected to take longer than 5 years.

It has also entered the E-Trucks segment. HBL identified a technology gap in imported critical components (motors, batteries, electronics) for EVs in India. The strategy is to fill this gap and sell trucks directly to users in lower volume niche markets with higher margins, rather than supplying drive train technology to truck makers (a low margin business). Sales of new trucks (of 35 and 55 Tons) are expected to begin in October 2026.

In Lithium-Ion Batteries, HBL is focusing on low-volume, customized, engineering-intensive, higher-margin markets, such as Vande Bharat trains. HBL has also taken a capex plan of about ₹1 billion in CY25 to make high-energy-density cells in-house, following an earlier investment of ₹400 million on a pilot plant.

#3 Concord Control Systems: Emerging player in rail automation

Concord Control focuses on manufacturing and supplying Coach-related and Electrification products for Indian Railways and other Railway Contractors. Concord is currently transitioning from being primarily a Product/Equipment Supplier to a Solution Provider for Indian Railways. It operates 4 manufacturing facilities located at Lucknow, Bangalore, and Hyderabad.

Its core manufacturing includes coaching-related and Electrification products, such as Emergency Light Units, Inter-vehicular couplers, and modern Brushless DC Carriage Fans. In the Traction segment, it supplies various ratings of Battery Chargers, Control/distribution Panels, and the specialized Tensile Load Testing Machine for insulators.

Concorde is involved in the Kavach business through its subsidiary Progota India, in which it holds a 26% stake. It sees an opportunity worth ₹400 billion till FY30 from the Kavach system. Its unexecuted order book stood at ₹ 2.1 billion as of 31 March 2025, which is nearly 1.7x the FY25 revenues.

In FY25, revenue increased by 90% year-on-year to ₹1.2 billion, with margins at 23.8%. Net profit also rose 76.8% to ₹226.5 million. Concord reports half-yearly earnings. It aims to grow at around 40-50% annually for the next 3 to 5 years, starting FY26. They intend to maintain Margins in the range of 22-25%.

Beyond Kavach, Concord is focusing on expanding its new businesses, including the Metro Business (Overhead Monitoring systems) and the DPWCS (Distributed Power Wireless Control System) business. DPWCS allows many freight trains to be combined as a single train, and offers a market opportunity worth ₹25 billion over the next 5-6 years, driven by safety norms and speed requirements for freight transportation.

Do these Kavach stocks justify the ticket price?

Though Kavach offers a big opportunity over the coming 6-7 years, valuations are already running ahead of time. HBL is trading at a price-to-earnings multiple of 71.3x, almost double the 10-year median (38.9x) and industry P/E (31.7). Similarly, Concord trades at 74.9x, above the 3-year median of 45.4x, and double the industry (36.5x). Kernex, however, is trading at 35.1x, in line with the 10-year median of (33x), and the industry P/E of (34.7x).

Valuation Comparison

| Company | P/E | 10-Year Median | Industry P/E |

| HBL | 71.3 | 38.9 | 31.7 |

| Kernex | 35.1 | 33 | 34.7 |

| Concord | 74.9 | 45.4 (3-Year) | 36.5 |

While valuations across Kavach-linked stocks have run up sharply, the broader opportunity remains significant. The government’s focus on rail safety, automation, and speed — under initiatives like Mission Raftar — provides a long growth runway. Yet, investors need to recognize that the Kavach rollout will be phased and capital-intensive, with execution timelines stretching beyond this decade.

HBL Power Systems appears best placed to benefit from scale and diversification, while Kernex offers a more direct but concentrated play on the Kavach theme. Concord, though smaller, could surprise as it transitions from a product supplier to a systems partner for Indian Railways.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data was not available have we used an alternate but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.