Mukul Agrawal is amongst the top super investors in India when it comes to following in the investor circles. The founder of Param Capital Group, Agrawal is widely known for his bold investment strategies. No wonder he is a part of our list of the Warren Buffetts of India.

Agrawal currently holds 71 stocks in his portfolio worth almost Rs 7,500 cr. But two of these stocks that he recently added to his portfolio have caught the attention of smart investors, as something to look closely at in 2026. With 81% and 140% gains already just in this year, they do warrant a look at now and in 2026.

Let us dive into these 2 stocks.

Tatva Chintan: The EV & Pharma turnaround bet

Tatva Chintan Pharma Chem Ltd was incorporated in 1996 and is a manufacturer of a diverse portfolio of structure Directing Agents, Phase Transfer Catalysts, electrolyte salts for batteries, and Pharmaceutical and Agrochemical Intermediates and other Speciality chemicals.

With a current market cap of Rs 3,647 cr, the company has a portfolio of 214 products catering to a long list of clientele that includes Laurus Labs, Atul, Asian Paints, SRF, Otsuka, Divis Nutraceuticals, Merck, Navin Fluorine International Ltd, etc.

Mukul Agrawal bought a 1.3% stake in the company worth Rs 34.4 cr as per filings for the quarter ending June 2025. This holding has now gone up to 2.1% making the holding worth Rs 78 cr.

Tatva Chintan’s sales have grown at a compound rate of just 8% in the last 5 years from Rs 263 cr in FY20 to Rs 383 cr in FY25. For the current FY, until the end of September 2025, the company has recorded Rs 240 cr in sales.

The EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) has seen a drop from Rs 55 cr in FY20 to Rs 34 cr in FY25. And for the period of April 2025 to September 2025, the logged EBITDA is Rs 39.5 cr, which points at a better year already.

The net profits also dropped from Rs 38 cr in FY20 to Rs 6 cr in FY25. However, between April and September 2025, the company has already recorded net profits of Rs 16.6 cr, hinting at a stronger financial year in terms of profits.

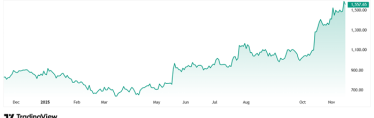

The share price of Tatva Chintan Pharma Chem Ltd was around Rs 860 in January 2025, and as of 18th November it was Rs 1554, which is a jump of 81% in just 9 months. If you look at the chart below, it is showing signs of a turnaround.

The company’s share is currently trading at a PE of 205x, while the industry median is at 30x. The company was listed in 2021, so it would be too soon to look at the 10-year median for it, but the industry median for a 10-year period is 28x.

According to the recent investor presentation in November 2025, Tatva Chintan is exiting a prolonged downcycle with clear traction across high-barrier verticals (SDA, Electrolytes, Semiconductor) and a growing docket of multistage agro/pharma intermediates.

Monolithisch India: Riding the steel cycle boom

Incorporated in 2018, Monolithisch India Ltd is a manufacturer of premixed high-quality ramming mass.

With a market cap of Rs 1,251 cr Monolithisch into the manufacturing and supply of specialized ramming mass, a heat insulation/lining material used as a refractory consumable for Induction furnaces installed in iron, steel, and foundry plants.

The company also undertakes trading activities occasionally to meet excess and urgent customer demands.

The company was listed in June 2025, and Agrawal bought a 2.3% stake in the company worth Rs 24 cr. A holding that has now been increased by him to 3% worth Rs 34.5cr.

The sales of the company have grown at a compounded rate of 81% from Rs 5 cr in FY20 to Rs 97 cr in FY25. The company files in half yearly financial statements and according to the last one in September 2025, the company had already recorded sales of Rs 57 cr in FY26.

EBITDA went from Rs 1 cr in FY20 to Rs 21 cr in FY25, logging in a compound growth of 84%. In the first 2 quarters of FY26, the EBITDA is already Rs 12 cr.

As for the net profits, the company has shown a big turnaround as it went from making zero profits in FY20 to net profits of Rs 14 cr in FY25, which is a compounded growth of 114%. Between April and September 2025, the company has recorded profits of Rs 9 cr.

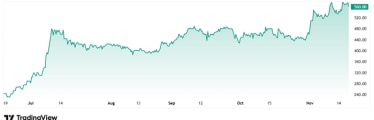

The share price of Monolithisch India when it was listed in June 2025 was around Rs 240. As on 18th November 2025 the price was at Rs 576, which is a jump of 140% in just 3 months.

The company’s stock is trading at a PE of 71x, while the industry median is 41x. The 10-Year median PE for the industry is 27x.

Monolithsch also boasts of a current ROCE (Return on Capital Employed) of 61%, which means it is making Rs 61 in profits on every Rs 100 it invests as capital in the business. The industry median ROCE when compared to peers is about 17%, which means Monolithisch is doing a better job of making profits from capital investments than its peers.

In the October 2025 investor presentation, the Executive Director, Kritish Tekriwal, said, “Over the past two years, the company has demonstrated a strong and consistent growth trajectory. Revenue has expanded at a compound annual growth rate of 52%… Looking ahead, we remain focused on sustaining this momentum with revenue CAGR FY 25-28 projected in the range of 60%.”

Geared for a bigger 2026?

The two stocks that we saw today were picked up by Mukul Agrawal in 2025 and he has in theory already started to profit from them. Which proves that when Agrawal picks stocks, they are not hunches or emotional decisions, but well researched stocks with strong potential.

The big question here is do these 2 stocks still have fizz left for them to continue or even outperform what they recorded in FY25 all the way to 2026? Remember, both the stocks are showing signs of a solid turnaround and are already looking at a good quarter and financial year.

Well, as 2025 draws to an end, it is time when smart investors will start making their watchlist for 2026. If you too are making one, these two Mukul Agrawal approved stocks deserve a place in there.

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.