Data centers are the hidden factories of the digital age. They are the places where servers store and process the information that keeps our digital lives running. Demand for data centers has been rising sharply in recent years, driven by the growth of cloud computing, the rapid expansion of artificial intelligence, and the vast amount of data generated by businesses and consumers every day.

Orient Technologies Annual Report states that the data center industry in India is expected to grow to ₹240-280 billion by FY27, from ₹84.5 billion in FY23. As a result, India has emerged as the second fastest-growing data center market in the Asia-Pacific region. Jefferies estimates that the capacity will quintuple to 8 GW over the next five years, driven by rising internet traffic.

Several factors, including regulatory mandates and data localization, digital consumption, cloud adoption, government policies such as the Data Center Incentive Scheme and the proposed Data Center Economic Zones, will drive this expansion. Next, apart from this little-known realty stock that is secretly building a ₹100 billion data center empire, these three stocks could be among the gainers. Let’s take a look…

#1 Orient Technology: Integrating cloud and IT infrastructure

Orient Technology began as an Information Technology transformation partner in 1997, evolving from a computer and telefax machine seller to a digital provider and transformation partner focused on IT asset lifecycle management. The company provides reliable IT infrastructure, managed services, and digital innovation.

Expanding Presence in Data Centre and Cloud Technologies

Within the data center, it offers a full suite of data center hardware and software components, and related services. This includes servers and storage systems, networking components, and collaboration solutions, including CCTV surveillance systems and video conferencing platforms.

Additionally, it is present in future-ready technologies such as hyperconverged infrastructure, virtualization, software-defined technologies, cloud and network solutions, virtual desktop infrastructure, and managed services.

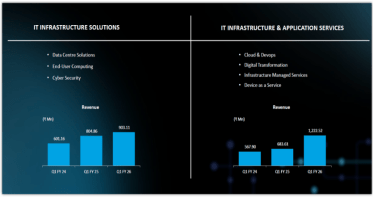

Orient has reorganized its business into two core business lines (LOBs) from FY26, aiming to balance their contributions. IT infrastructure solutions (including data center and cybersecurity) currently account for 65% of revenue, while applications and IT infrastructure services contribute 35%. Orient aims to achieve a 50:50 revenue split between the two LOBs over time.

Orient Segment Performance

Steady Growth Momentum in Q1FY26

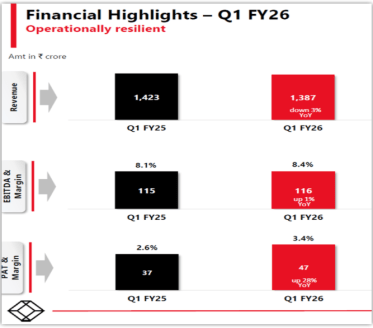

In Q1FY26, the company’s revenue rose 42.8% year-on-year to ₹2.1 billion. At the same time, EBITDA (earnings before interest, tax, depreciation, and amortization) surged 26.9% to ₹173 million, with a lower margin of 8.1%. Margins were impacted due to investments in establishing an integrated Net Operating and Security Operating Center, as well as increased employee costs for new skill sets.

As a result, profit after tax (PAT) rose by just 8% to ₹100 million. But management expects margins to improve starting from Q3FY26 once the SOC becomes operational. Orient reported a strong order book of ₹4.1 billion for the remainder of FY26, with ₹1.8 billion billable Q2FY26.

Strategic Shift Towards a Service-Led Growth Model

Looking ahead, the company is strategically moving towards a service-led business model, from single-product sales to bundled offerings that integrate value-added services. This approach aims to enhance customer value, achieve improved margins, and ensure long-term revenue sustainability through an annual recurring revenue-driven business.

Cloud and Digital Transformation remain key drivers for growth. The company provides solutions like SecOps (security on cloud) and SynOps (cloud financial management/FinOps) to help customers optimize their increasingly expensive cloud billing. Over the longer term, the company aims to become one of the top five System Integrator (SI) partners in India within three years.

While operations are currently concentrated in India, generating the predominant share of revenue from the country, OTL aims to expand its geographic footprint and cater to a broader customer base globally, targeting Asia Pacific countries or the Middle East within three years.

#2 Blackbox: Powering Global Data Infrastructure

Black Box operates as a global digital infrastructure integrator, offering broader technology solutions and services to global markets and across various sectors. It serves mainly through the Global Solutions Integration segment, which provides connectivity infrastructure, cybersecurity, and data center services.

Global Reach with a Glocal Operating Model

The company operates on a “glocal” model (think global, act local) to serve its more than 1,000 global clients. It has a presence in 35 countries across six regions, including North America, Latin America, Europe, Asia-Pacific, the Middle East and Africa, and India. North America is currently the largest growing market.

Hyperscale and Enterprise Data Center Capabilities

Blackbox provides hyperscale and enterprise data center solutions across various countries and continents. This includes building dense infrastructure, providing specialized capabilities such as high-speed networking, modular deployment models, retrofits, and developing energy-efficient, AI-ready infrastructure.

The company aims to evolve from a transactional provider to a strategic partner for its data center customers. To this end, the data center vertical is one of five high-growth areas of BlackBox’s market entry strategy. Blackbox currently executes large-scale mandates for three of the top five hyperscalers worldwide. Hyperscaler means a large cloud service provider.

The company engages directly with major hyperscalers (such as Meta) for contracts in certain sites and geographies (like in Europe & the US). In addition, it also works with their large master contractors in other areas. In Q1FY26, BlackBox secured two significant data center orders in the US. Of this, one order was from a global hyperscaler and the other from a top-10 global core location provider.

Strong Order Book and Data Center Growth Outlook

BlackBox estimates that its data center orders should represent around 20%-25% of its total order book. This means that, based on the company’s target of achieving a $1 billion order book in FY26, data center orders are expected to exceed $200 million. To achieve this goal, the company has appointed a dedicated leader to lead the data center vertical.

Additionally, the company is leveraging its global experience with hyperscaler clients to establish leadership in the Indian digital infrastructure ecosystem. Its current order pipeline exceeds $2 billion, and it aims to achieve a total revenue of $2 billion by FY29.

Robust Order Book Sets Stage for Sequential Growth

From a financial perspective, revenue from operations fell 3% year-on-year to ₹13.8 billion. The performance was affected by client-driven delays in equipment procurement due to the prevailing tariff situation. These delays pushed out revenue recognition and consequently affected operating margins.

Financial Performance

Operating profit increased by just 1% to ₹1.1 billion, while margin expanded by 30 bps to 8.4%. PAT, however, rose 28% to ₹470 million. The total order backlog remained strong at $518 million in Q1FY26, which is estimated to reach an order book of over $700 million by the end of FY26. Blackbox continues to focus on attracting large-sized contracts and high-value customers.

Blackbox management expects the upcoming quarter’s performance to be significantly better than Q1, as the strong order book will translate into revenue. It estimates revenue and order book momentum to grow between 15%-20% sequentially in the coming quarters.

#3 E2E Networks: Fueling the AI Compute Revolution

E2E Networks is primarily an AI-focused hyperscale cloud platform. The company operates its cloud infrastructure through data centers, providing services such as accelerated Cloud GPUs and managed hosting solutions. Within data centers, E2E includes cloud computing services to Indian data centers in Noida, Chennai, and Mumbai.

Expanding Data Center Footprint and GPU Capacity

Historically, E2E operations have been concentrated around Delhi-NCR. In 2019, the company established a new data center in Delhi-NCR and expanded GPU deployment. It maintains a total of 10 MW of datacenter IT power capacity and 3,900 GPUs. Recently, it added GPU capacity in Noida, which is operational and available for proof-of-concept and revenue generation.

Additionally, it has expanded into Chennai to strengthen its infrastructure presence across India and enhance regional latency for enterprise and AI workloads. E2E has deployed GPU clusters at Larsen & Toubro’s state-of-the-art data center in Chennai, with a capacity of 1,024 single large GPU clusters. This capacity boasts a total capacity of 20,000 GPUs, allowing for future capacity expansion as needed.

Short-Term Financial Pressure from Capacity Build-Out

From a financial perspective, revenue declined 12.6% to ₹361.1 million in the first quarter of FY26. However, EBITDA decreased 61.5% to ₹105 million, while margins fell 3689 basis points to 29.1%. The company swung from a profit of ₹101.4 million to a net loss of ₹284 million. Fixed operating costs impacted financials due to capacity build-out in Chennai.

Positioning for Growth in Generative AI and High-Margin Expansion

Looking ahead, E2E views the Generative AI sector as a high-value niche that could grow into a $1.3 trillion market by 2032, positioning E2E as the backbone cloud platform for enterprises. E2E also intends to invest in NVIDIA Blackwell GPUs (such as B200 or B300/GB300 series) with capacity expansion potentially occurring in Q4FY26.

Management is currently targeting an exit Monthly Recurring Revenue (MRR) of about ₹320 million to ₹380 million by March 2026, based on current capacity utilization goals. Operating margins are expected to improve from current levels. Management anticipates achieving an EBITDA margin between 65% and 75%.

What about Valuation?

The growth story is undoubtedly strong, which is already factored into sky-high valuations.

E2E is trading at a massive price-to-earnings (P/E) multiple of 189x, more than double the 5-year median of 71x. Blackbox trades at 33x, in line with the 10-year median of 31x, while Orient is trading at 37x. We have not compared Orient’s valuation historically due to its limited trading history. But, all three companies are trading at well-above the industry median of 32.5x.

Valuation- Comparison

| Company | P/E | Industry |

| Orient | 37 | 32.5 |

| Blackbox | 33 | 32.5 |

| E2E | 189 | 32.5 |

While the valuations appear stretched, any delay in execution or slower-than-expected demand normalization could trigger a de-rating in the near term. Investors may need to wait for earnings to catch up before these valuations look more reasonable, even though long-term fundamentals for India’s digital infrastructure story remain intact.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data was not available have we used an alternate but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.