From a pure data perspective, 2025 has not been a great year when it comes to FIIs buying into Indian stocks. Of course there were purchases, but the sales outdid them. As per data on Trendlyne, the net FII outflow between January and October 2025 was Rs 256,201 cr. That is a huge number. At some point, analysts called this an exodus of sorts, with foreign investors pulling out and leaving. However, the domestic smart money was quietly filling in the gap that was created with net inflow of Rs 648,158 cr.

However, while this was happening two widely tracked Indian banks managed to still catch the attention of FIIs. Their FII holdings saw big jumps making investors take note. Mind you, these are large cap banks with over Rs 250,000 cr of loan books.

So, what is it that the foreign smart money sees in these banks and could it be an opportunity for investors? Let us look into the two banks.

Turnaround after the big banking disaster?

Incorporated in 2003, Yes Bank Ltd is engaged in providing a wide range of banking and financial services.

With a market cap of Rs 71,723 cr, it is the 6th largest private sector bank in total assets terms.

FII holding for Yes Bank was 27% for the quarter ending September 2024. This holding saw a dramatic jump due to a single, strategic deal. As per filings for quarter ending September 2025, Sumitomo Mitsui Banking Corporation bought a 24.21% stake in the bank making it the largest stake holder. This stake was sold by the DII consortium (including SBI, HDFC Bank, and others) that had rescued the bank in 2020. So, one big FII has replaced the domestic rescue team.

The DII holding on the other hand was 38% for the quarter ending September 2024 and for the quarter ending September 2025, it was at 21%. State Bank of India sold off its 13% stake between the quarter ending June 2025 and the one ending September 2025 to Sumitomo Mitsui Banking Corporation.

As for the financials, the bank’s revenues grew at a compounded rate of a mere 3% from Rs 26,052 cr in FY20 to Rs 30,919 cr in FY25.

According to the company’s latest investor presentation in October 2025, the bank’s total loan book crossed Rs 250,000 cr as it grew by 6.8% YoY.

The NII (Net Interest Income) grew from Rs 8,094 cr in FY24 to Rs 8,944 cr in FY25, which is a growth of 10.5%. The NIM (Net Interest Margin) was stable at 2.4%, the same as the last financial year.

The net profits for Yes Bank could be an area of interest for the FIIs and other investors. Between FY20 and FY25, the bank has shown a turnaround if we can call it so.

| Year | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 |

| Profits/Rs Cr | -16,433 | -3,489 | 1,064 | 736 | 1,285 | 2,447 |

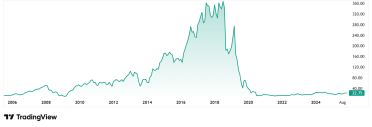

The share price of Yes Bank Ltd was around Rs 15 in November 2020 and as on 10th November 2025, it was Rs 23.

The bank’s share is trading at a PE of 25x, while the industry median is 15x. The 10-year median PE for the bank is 24x while the industry median for the same period is around 16x.

After reaching an all-time high of around Rs 404 in 2018, the bank saw what could only be called a crash. Under its co-founder and CEO, Rana Kapoor, the bank went on an aggressive lending spree, building a large loan book by giving huge loans to stressed companies and high-risk sectors. When large corporate groups like IL&FS, DHFL, Anil Ambani Group, and Essel Group began to default on their loans, Yes Bank had to pay the price.

Caught by the Rs 267,000 crore loan book?

IDFC First Bank Ltd is engaged in the business of Banking Services. IDFC FIRST Bank was founded by the merger of erstwhile IDFC Bank and erstwhile Capital First on December 18, 2018

With a market cap of Rs 69,759 cr, the bank serves 35.5 m active customers across 60,000 cities, towns, and villages in India and has expanded its branch network 5x, from 206 at the time of the merger to 1,002 branches by FY25.

The FII holding in the bank was 19.6% at the end of the quarter ending September 2024, and for the month ending October 2025, it was at 35.6%. Currant Sea Investments B.V bought a 9.5% stake and Platinum Invictus B 2025 RSSC Limited bought another 5% stake as per the exchange filings.

The bank’s revenues grew at a compounded rate of 18% from Rs 16,240 cr in FY20 to Rs 36,502 cr in FY25.

According to the company’s latest investor presentation in October 2025, the bank’s loan book grew by 20% on a YoY basis to Rs 267,000 cr.

The NII (Net Interest Income) grew from Rs 16,451 cr in FY24 to Rs 19,292 cr in FY25, which is a growth of 17%. The NIM (Net Interest Margin) however witnessed a small drop from 6.36% of FY24 to 6.09% in FY25. The bank noted that this was due to decline in the micro-finance business.

As for the net profits after logging losses in FY20, the bank recorded good progress till FY24, and once again a drop in FY25.

| Year | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 |

| Profits/Rs Cr | 2,843 | 483 | 132 | 2,485 | 2,942 | 1,490 |

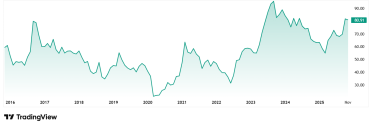

The share price of IDFC First Bank Ltd was around Rs 32 in November 2020, which has grown to its current price of Rs 81 as on 10th November 2025.

The bank’s share is trading at a PE of 49x, while the industry median is 15x. The 10-year median PE for the bank is 20x while the industry median for the same period is around 16x.

The bank intends to grow branches by only about 10% annually against an estimated deposit growth of approximately 25%. It also expects a minimum of 20% growth in its loan book.

Banking on the right stocks?

One thing to note here is that these deals appear to form a part of a larger pattern where foreigners are being permitted to increase their stake in Indian banks / NBFCs.

Indian banks and NBFCs will need capital as they grow. So far, they have relied on dometic sources, and to some extent on international borrowing. Now, it appears that the FII equity funding route is more open than before.

Coming to the two banks we dug into today, these among the biggest in the country with impressive loan books. However, when it comes to profits, the two banks show completely different stories. Yes Bank’s data shows a strong profit recovery. Yes Bank has cleaned up its books and returned to profitability. Perhaps this was one of the reasons the existing shareholders wanted to exit.

IDFC First Bank on the other hand has seen profits drop in the last fiscal year. Additionally, its loan book is growing fast. It therefore has a large need for fresh capital to keep its loan engine firing. This funding caters to that need.

Having done these deals, the FIIs have latched themselves to two of the leading mid cap banking players in India. These banks, now armed with clear ownership and strategy (Yes Bank) and fresh capital to grow (IDFC First), hold the potential to deliver on their promise of solid growth in the years to come.

How the banks will truly perform in the months and years to come will be an interesting ride to watch. But for now, it would be a smart decision to add them to a watchlist and follow them, to ensure that no opportunity or crash misses the eye.

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article. The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.