")

The automotive industry globally is seeing a significant transformation due to technological innovations and the shift towards clean mobility. It’s driven by Personalization, Autonomous, Connected, and Electric mobility megatrends.

While global growth remains subdued, India continues to stand out due to its growing economy, rising per capita income, strong domestic demand, increasing localization, and electrification. The auto sector, which was sluggish in FY25, is poised for a recovery in FY26, aided by the recent reduction in goods and services tax (GST) and savings on account of income tax rationalization.

At the same time, government initiatives such as FAME India, PLI Scheme for the automobile and auto components industry, and the PM E-Drive Scheme are giving a further boost to the decarbonization agenda, driving demand for auto ancillaries. China+1 shift is also positioning India as a major beneficiary.

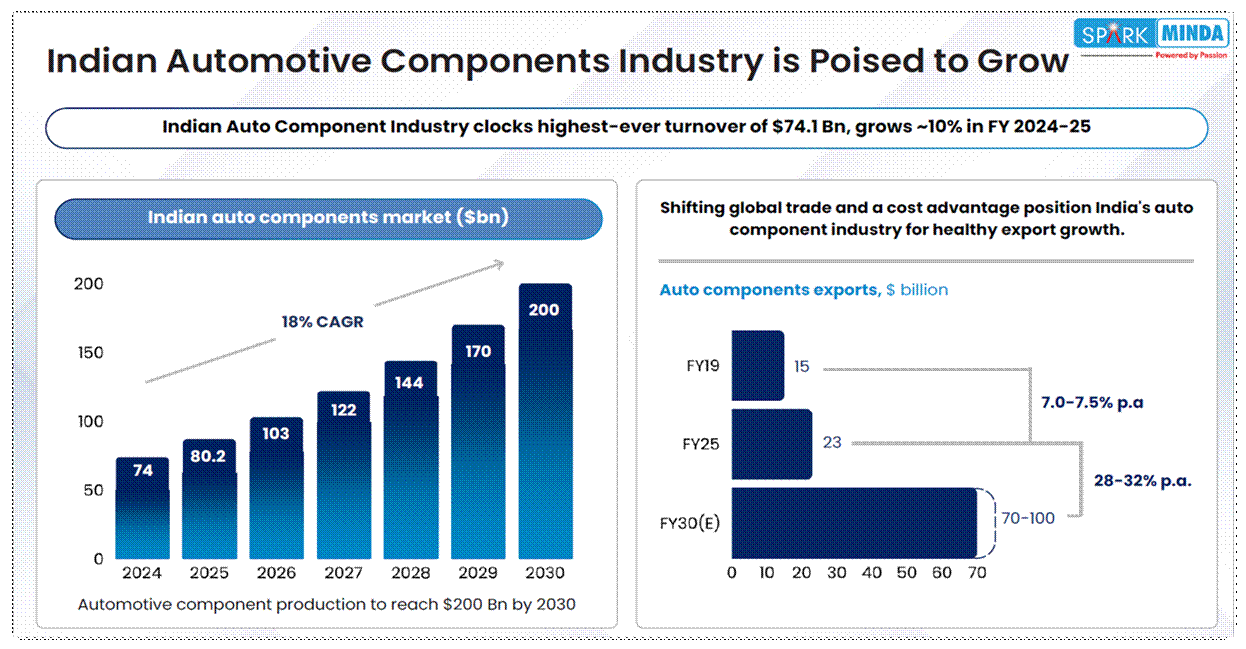

This creates a favorable environment for them, many of which are diversifying and expanding into newer product categories to capture higher value per vehicle. These figures also reflect this. The Indian auto component industry achieved its highest-ever turnover of $74.1 billion in FY2025. Minda Corp. estimates the Indian auto ancillary market to grow at an 18% CAGR from $74 billion in FY24 to $200 billion by FY30.

Indian auto component industry set for strong growth

Auto component export is also expected to grow at 28-32% per annum from $23 billion in FY25 to $70-100 billion by then. For investors, auto ancillary stocks also offer a way to participate in the broader growth of the auto sector. Here are three stocks that provide such an opportunity…

#1 Uno Minda: Aggressive expansion pipeline to drive multi-year growth

Uno Minda is a global technology leader in auto components and systems manufacturing. The company manufactures a variety of auto components, including lighting, switches, alloy wheels, horns, seating systems, sensors, controllers, and electric vehicle (EV) components. Over 95% of its portfolio is powertrain-agnostic, serving internal combustion engine (ICE), hybrid, & electric vehicles.

Diversified portfolio with a powertrain-agnostic edge

Its product portfolio serves two-wheelers (2W), three-wheelers (3W), four-wheelers (4W), commercial vehicles, and off-road vehicles. For Uno Minda, EVs are a key pillar of growth, driven by the growing demand from e-two-wheeler (E2W) and e-three-wheeler (E3W) companies. The company estimates the EV kit value potential at ₹37,636, which is three times its current ICE kit value of ₹11,936.

Expanding into high-value segments and new partnerships

To drive long-term growth, Uno Minda is investing in products that increase the value of content per vehicle. It has entered the vehicle sunroof segment in partnership with AISIN Corporation of Japan. Production is expected to begin in FY27, which will aid revenue growth. It is also focusing on advanced lighting, including OLED lamps and adaptive lighting systems.

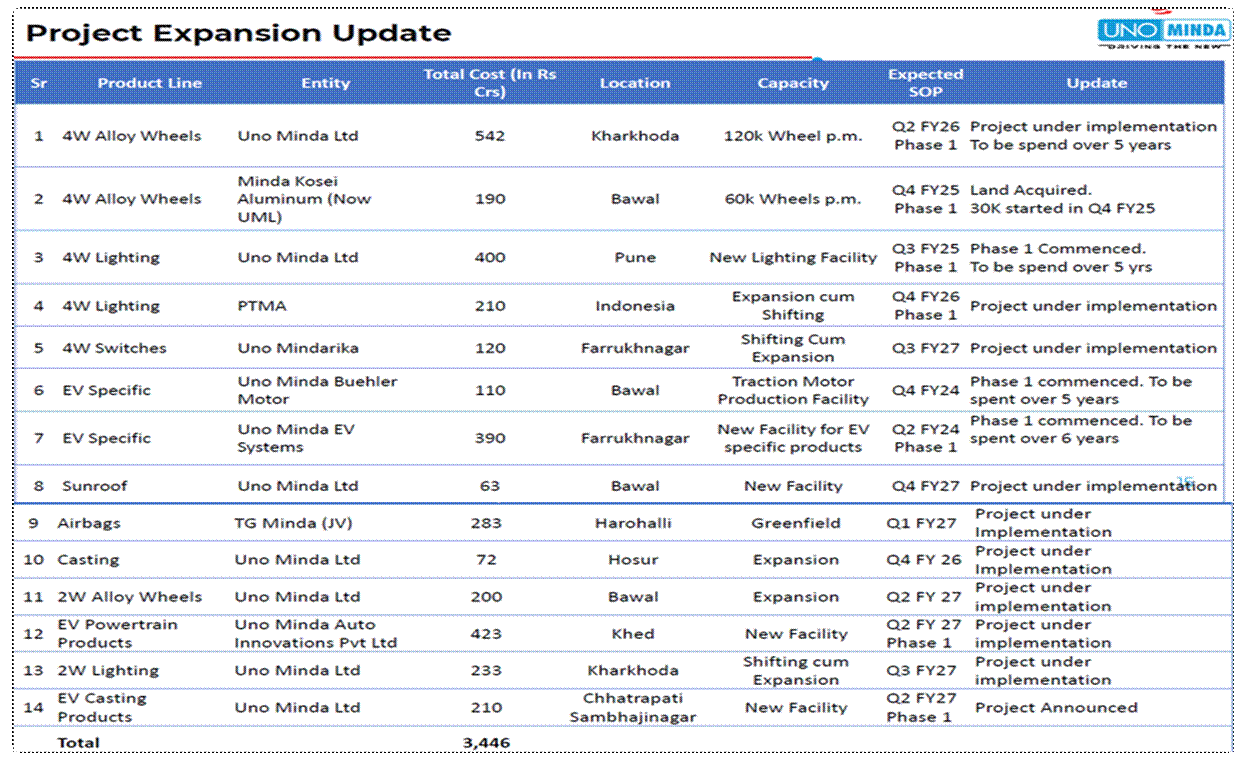

It is investing ₹34.5 billion in expansion over the next five years. This includes commissioning an additional 30,000 wheels per month capacity for 4W alloy wheels at Bawal and expanding the annual capacity of 2W alloy wheels at Supa to 8 million wheels. It is also integrating its 2W lighting plants in Sonipat and Bahadurgarh into a new integrated facility in Kharkhoda to improve operational efficiency.

Aggressive Expansion Pipeline

The company is expanding its EV portfolio for both 2W and 4W. Under 4W, Minda is focusing on high-voltage EV components such as EV inverters, motors, and e-axles for passenger and commercial vehicles. For this purpose, it is building a new greenfield plant in Pune, which is expected to be operational by the second quarter of FY27.

Uno Minda has also partnered with StarCharge for EV supply equipment. It has secured orders, and deliveries are expected to begin by Q3FY26. It has also completed the acquisition of the joint venture with FRIWO, which will strengthen its integrated offerings for the E2W and E3W markets. It is also investing ₹2.1 billion in setting up a casting division for EV components.

Strong financial momentum and healthy margins

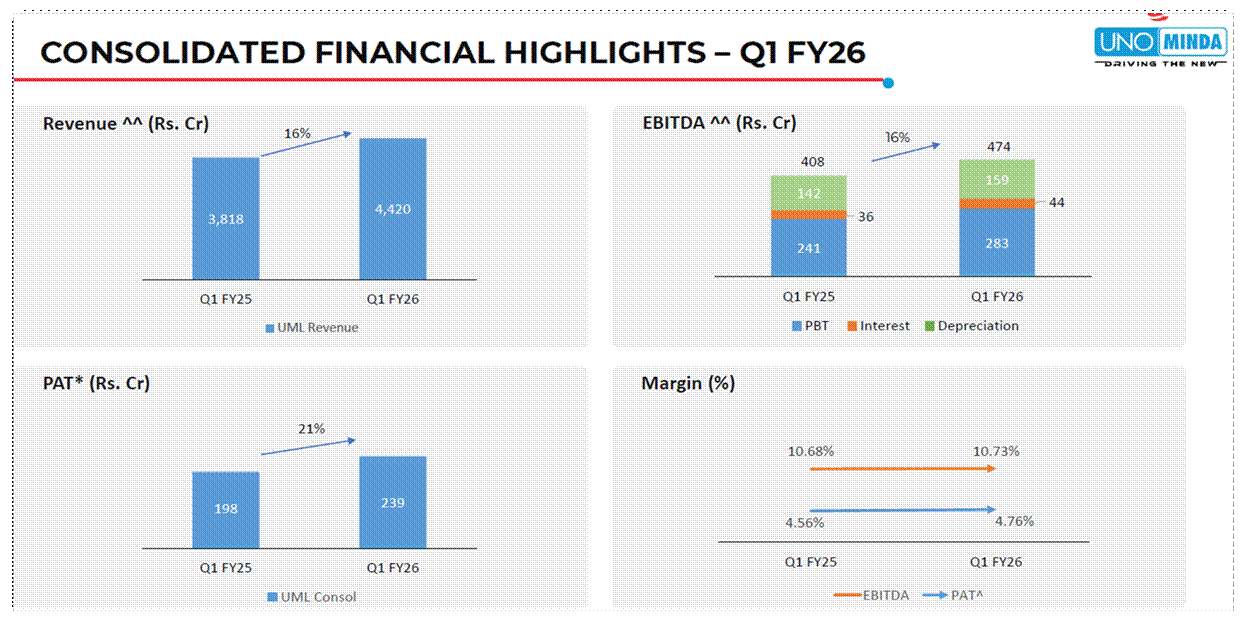

From a financial perspective, revenue in the first quarter of FY26 increased 16% year-over-year to ₹44.2 billion. This increase was driven by 30% growth in other segments (camera modules, sensors), seating (+17%), switches (+16%), lighting (+13%), and castings (+9.8%). This was offset by an 8% decline in acoustic devices due to lower demand in the European auto market.

Strong Financial Performance

Geographically, India contributed 89% of revenue, and international (11%). Channel-wise, Original Equipment Manufacturers (OEM) contributed 93% of revenue, followed by Aftermarket (7%). Segment-wise, 93% of revenue came from 2W (46%) and 4W (47%), while the remaining came from Commercial Vehicles (4%) and 3W (2%). EBITDA surged by 16% to ₹4.7 billion, with margins at 10.7%. Profit after tax (PAT) increased by 21% to ₹2.4 billion.

#2 Minda Corporation: Vision 2030 targets multi-fold revenue growth

Minda Corp is a significant player in the global automotive industry with a legacy spanning over six decades. Its primary business verticals are Electrical Distribution System, EV System & Electronics, Light Weighting & Plastics, Driver Information System, and Vehicle Access. Minda offers a diverse product range, including access systems, EV-specific components, electronics, lightweight plastics, and sunroofs.

A legacy player reinventing for the EV era

EVs are expected to drive a minimum 20-30% increase in content per vehicle. The combined kit value for Powertrain Specific e2W products offered by Minda is estimated to be ₹30,000-35,000. It offers extensive EV products, including EV Traction Motors, Motor Controller Units, DC-DC Converters, HV Wiring Harness Connection Systems, and TFT Instrument Clusters.

Vision 2030 targets multi-fold revenue growth

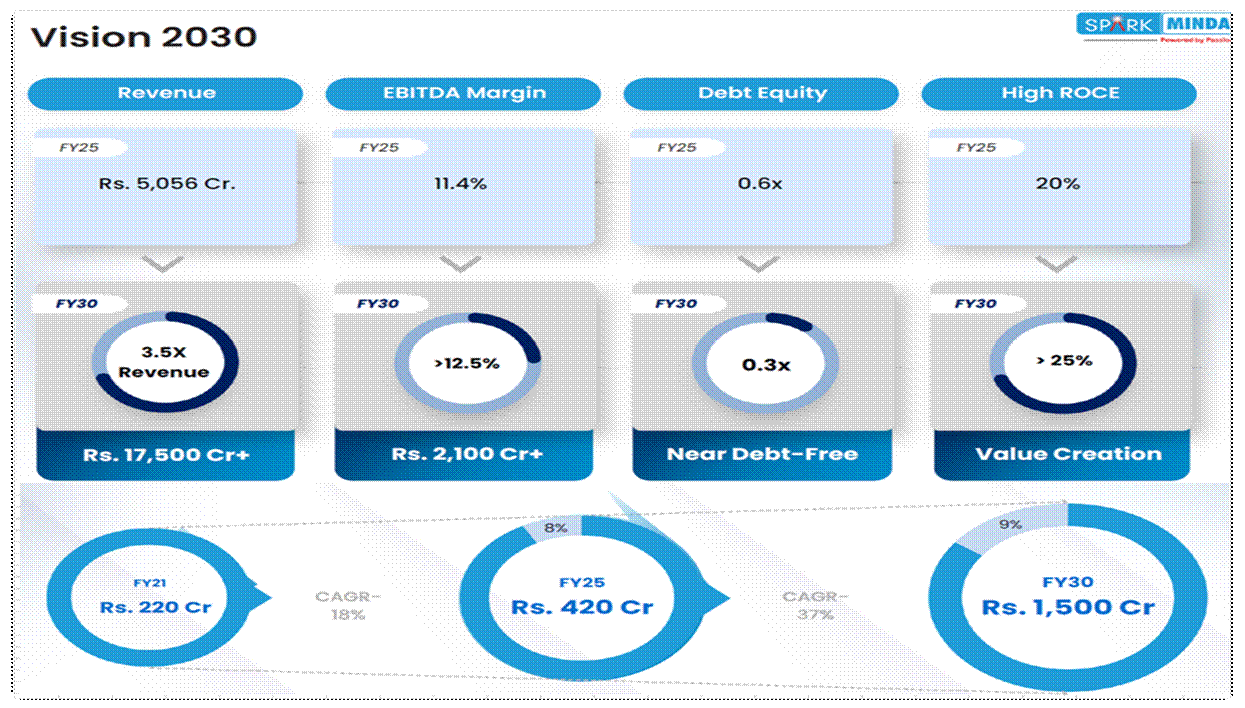

Minda Corp has implemented an aggressive expansion plan under its Vision 2030. Starting with balance sheet management, it plans to reduce debt-to-equity from 0.6X to 0.3X. It has reduced working capital days from 53 (FY22) to 31 in FY25, which is expected to generate ₹10 billion in cash by FY30. It also plans to invest ₹20 billion over the next five years.

Minda Corporation Vision 2030

Within the revenue mix, the plan is to increase the share of passenger vehicles to 25% by FY30, up from 14% in FY25. At the same time, the share of 2W/3W will decline from 47% to 40%, commercial vehicles (28% to 25%), and aftermarket (11% to 10%). Overall, the company plans to expand its revenue by 3.5X to ₹175 billion (₹50.5 billion in FY25) by FY30. Of this, ₹15 billion is expected to come from exports, up from ₹4.2 billion in FY2025.

With the changing revenue mix, EBITDA margins are also expected to increase from 11.4% to above 12.5% in FY30. With improved efficiency, return on capital employed is also likely to increase from 20% to over 25%. It is setting up two new greenfield plants in die casting and instrument clusters to support its expansion plan.

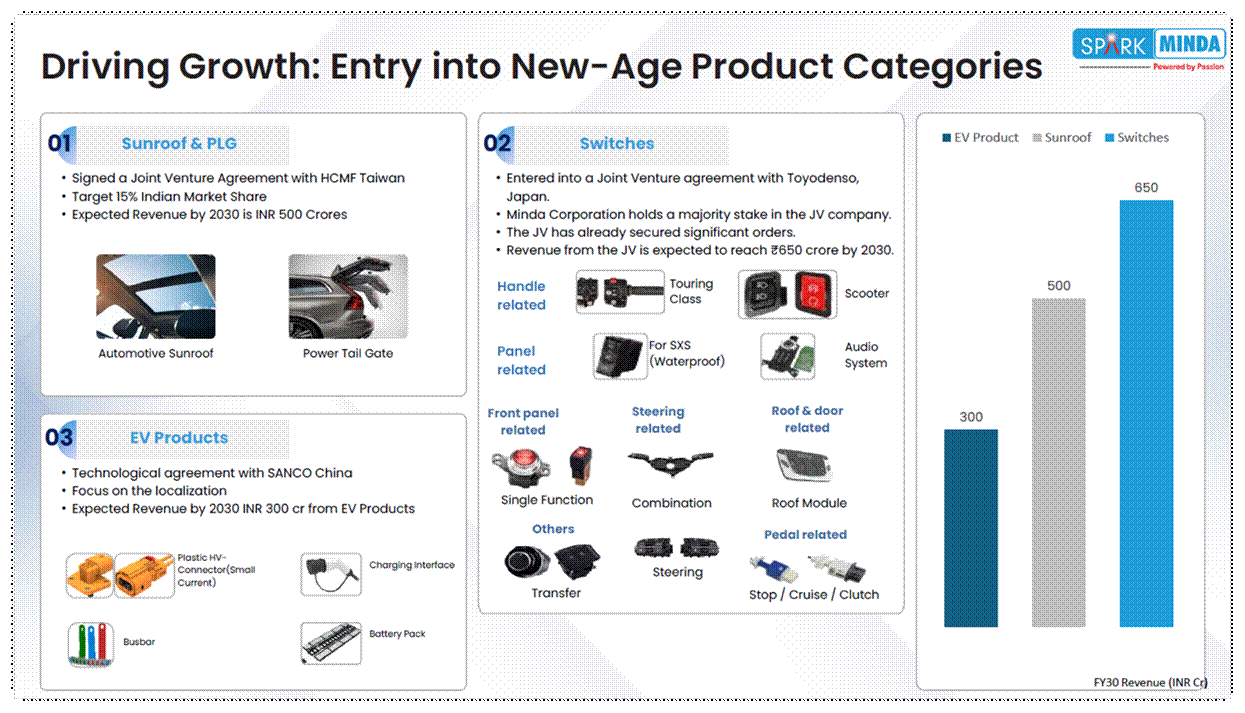

Portfolio Expansion Through JVs

To achieve its goal, Minda is also expanding its product portfolio through joint ventures (JVs). This includes a JV with HCMF Taiwan, aiming to achieve a 15% market share and ₹5 billion revenue by FY30. With a focus on localization, it has also signed a technology agreement with SANCO China, with a revenue target of ₹3 billion. Minda has also set up a JV with Toyodenso (Japan), targeting Rs 6.5 billion by FY30.

Financial growth supported by operational efficiency

From a financial perspective, revenue grew 16% year-over-year to ₹13.8 billion in Q1FY26. This growth was driven by a 19% increase in the Information & Connected Systems vertical and a 13% increase in the Mechatronics, Aftermarket & Others vertical. By end market, 2W and 3W contributed 47% to revenue, followed by Commercial (29%), Passenger Vehicles (15%), and Aftermarket (9%).

Wiring harnesses remained the largest contributor to revenue (30%), followed by accessories (23%), die casting (15%), clusters (15%), and others (17%). EBITDA increased 18.6% to ₹1.5 billion, while margins stood at 11.3% (+23 bps). However, due to a 230% increase in finance costs, PAT increased only 1.7% to ₹650 million.

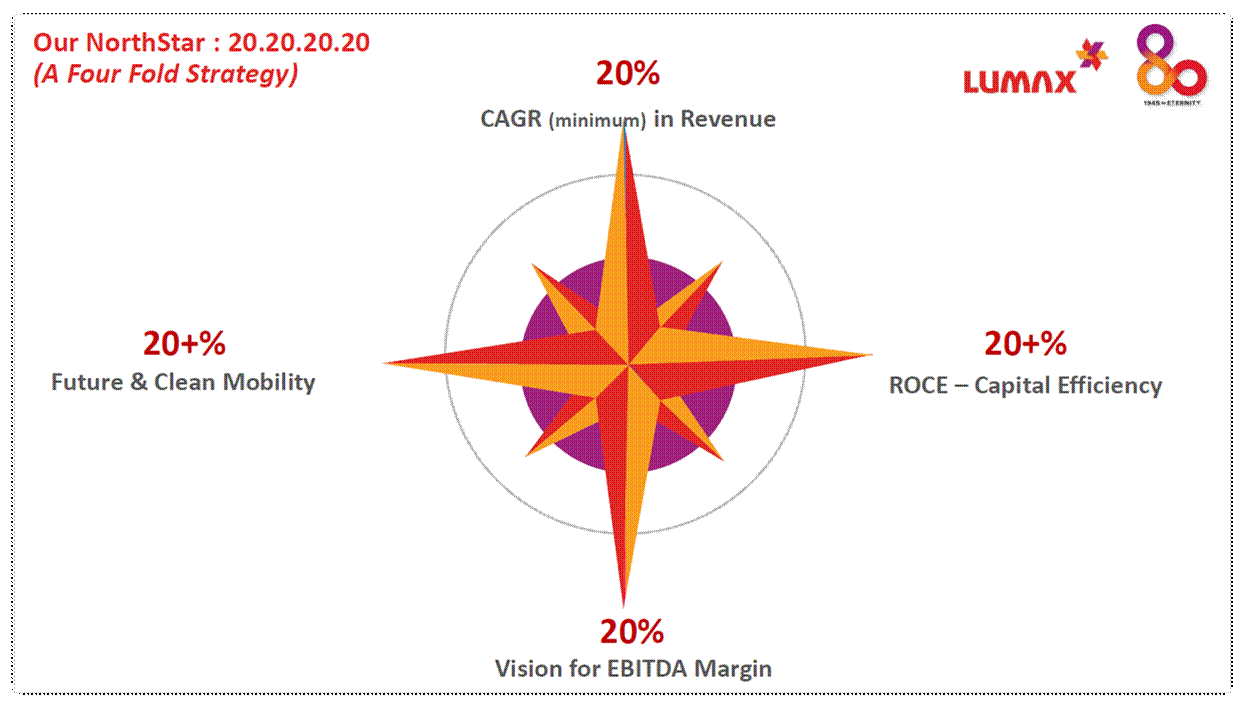

#3 Lumax auto technology: NorthStar strategy charts the road to long-term growth

Lumax Auto is part of the DK Jain Group of Companies. The company’s product portfolio is EV-agnostic, covering four main areas: Advanced Plastics (56% of revenue in FY25), Structures and Control Systems (19%), Mechatronics (11%), Alternative Fuels (8%), and Aftermarket (8%).

Northstar strategy aims for transformational growth

Segment-wise, Lumax primarily serves the PV (passenger vehicle) sector, which accounted for 55% of FY2025 revenue, followed by 2/3W (25%), aftermarket (11%), and commercial vehicles (9%). To drive its next phase of growth, Lumax has unveiled a mid-term plan for FY26-31, called the “20-20-20-20 Northstar” strategy.

NorthStar: A Four-Part Strategy

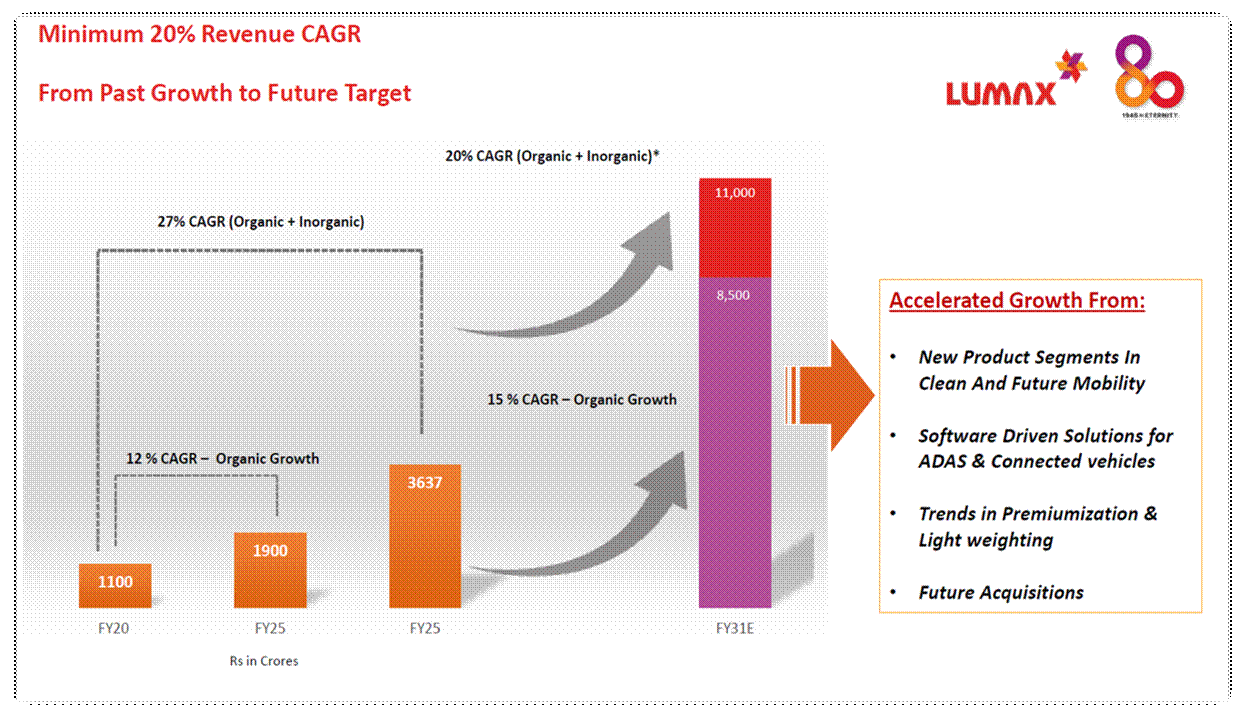

The company plans to grow its revenue at a minimum of 20% CAGR, which could triple its revenue from ₹36.3 billion (FY25) to ₹110 billion by FY31. This is expected to be driven by new product segments in clean and future mobility, software-driven solutions, premiumization, and acquisitions. Clean mobility is expected to contribute 20% to total revenue, up from 6% in FY25.

Revenue Growth of Minimum 20% CAGR

Next comes margins, which are expected to increase from 14% (FY25) to 20% in FY31, and return on capital employed 18% to over 20% by then. In the clean mobility space, the company acquired Greenfuel, an industry leader in alternative fuel systems. Greenfuel is expected to add ₹3-3.5 billion to Lumax’s revenue in FY26. Lumax’s other subsidiaries, such as Lumax Alps, Lumax Yokowo, and Lumax Ituran, are also expected to grow 30-40% annually.

Strong start to FY26 with double-digit growth

The company delivered a strong performance in the first quarter of FY26. Revenue grew 36% year-over-year to ₹10.2 billion, driven by aftermarket growth (+16%) and new product launches. EBITDA increased 19% to ₹1.3 billion, while margins stood at 13.2%. Profit after tax (PAT) increased 28.6% to ₹540 million.

Is the growth story already priced in?

From a valuation perspective, all three stocks are trading at a premium not only to their historical benchmarks but also to the industry average. Uno Minda is trading at a price-earnings (P/E) multiple of 66.8X, which is higher than the 10-year median (48.1X). Similarly, Minda and Lumax are trading at twice their 10-year median. All three are also trading significantly higher than the industry median.

Valuation Comparison (X)

| Company | P/E | 10-Year Median |

| Uno Minda | 66.8 | 48.1 |

| Minda Corp | 52.7 | 25.1 |

| Lumax Auto | 41.7 | 19.4 |

| Industry Median | 32.1 | NA |

There’s no denying the growth potential, but valuations continue to trade at a premium, even after factoring in their leadership in the industry. Now, it all depends on consistent execution, which must translate into guided growth. Any setbacks in this could disappoint Dalal Street. On the other hand, if growth continues as planned, valuation may sustain.

Disclaimer

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data was not available have we used an alternate but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article. The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.