")

India is entering a new phase. The Senior Care Report 2024, released from PwC–ASLI shows that by 2050 there will be 347 million Indians aged 60 and older, accounting for more than 21% of the total national population. This statistic correlates with the fact that approximately 19,500 people turn 60 every day, now called the “Silver Tsunami.”

This change is shaping economic and social priorities. Life expectancy rose from 62.5 years in 2000 to 70.8 years in 2021. Families are getting smaller, and as youth moves to bigger cities, an increasing number of elderly with no one to care for them are left behind. Collectively, these changes are driving retirement home, assisted living, home care, and technology-enabled eldercare services demand.

Previously worth $10–15 billion, India’s elderly care market is expected to grow to $30–50 billion in the next 10 years. For investors, it represents the emergence of the “Silver Economy”—an industry where aging populations are driving new and enduring business opportunities.

The selection in this article is based on a simple principle — direct participation in India’s senior-care market. Among listed entities, only a few have made tangible investments in senior living or assisted care.

As early adopters, Max India and Ashiana Housing are notable for taking distinct approaches to the opportunity: one through assisted living and integrated care, while the other through residential communities geared for seniors. Together, they represent the core of India’s emerging silver economy, offering investors a glimpse into how this long-term demographic theme is beginning to take corporate shape.

#1 Max India

Max India is the group holding firm of Max Group’s senior care business Antara, an integrated provider of all senior care services.

Having listed in August 2020 following its demerger from Max Ventures & Industries, Max India Ltd has become one of the few listed options to participate in India’s emerging senior-care opportunity. Through its Antara subsidiaries, it has its presence in senior living, assisted and transition care, and elder-centric consumer products under the brand AGEasy.

In FY26, Max India deepened its growth across all its verticals. Its senior-living segment registered good traction, with Gurugram selling out residential senior-living apartments in 11 months and fresh developments in progress in the National Capital Region and Chandigarh. These projects collectively constitute a robust near-term pipeline that can anchor revenue growth as soon as approvals and occupancy milestones are achieved.

In assisted care, capacity has grown to approximately 340 beds operational, with an additional 150 in fit-out. The segment’s top-line rose 2.2 times year-on-year to Rs 22 crore, while occupancy also rose from 14% in April to 23% in June.

Financially, though, the company continues to be under strain. Operating margins have been in negative territory for three years running at –62% (FY25), and ROCE is at –23.6%, showing capital intensity and minimal cash generation.

Net loss increased to Rs 139 crore in FY25, and sales dropped to Rs 156 crore. Management is hoping the consumer products business, AGEasy, will break even by FY27–FY28 with the help of internal accruals and treasury reserves of approximately Rs 320 crore, without having significant debt on books.

To fund this scale-up, the firm has anticipated a cash burn of approximately Rs 90 crore in FY26, financed by treasury revenues and non-core asset divestment proceeds, and fresh capital raised via a rights issue — with a further Rs 80 crore preferential issue in the pipeline.. Max India operates as a holding-cum-operating company, investing capital in its Antara subsidiaries with the balance sheet remaining debt-free to a large extent.

The coming 12–18 months will be critical to realize its expanding senior-care footprint into cash flows and operational breakeven.

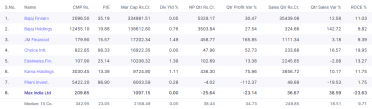

Relative to diversified holding peers like Bajaj Finserv, Edelweiss Financial, and JM Financial, Max India is smaller in size and different in structure. While peers generate stable returns from financial assets, Max India is creating long-gestation physical and service assets in an emerging industry. Its market cap of Rs 1,097 crore and negative profitability highlight both its stage of infancy and investor conservatism.

Peer Comparison of Max India With Other Financial Services Companies

For investors, Max India is still a long-term, high-risk bet on India’s “silver economy.” The company has gained operational credibility and unambiguous growth visibility, but execution pace, regulatory clearances, and operating leverage will establish whether its senior-care model can convert demographic winds into long-term financial returns.

In the past one-year Max India share price has tumbled 14.9%

Max India 1-Year Share Price Chart

#2 Ashiana Housing

Ashiana Housing is core business activity of the company is Real Estate Development.

Established in 1986, Ashiana Housing established a consistent presence in the mid-income and senior-living real estate space, with operations spread across North and West India. The company stands out from large-cap peers such as DLF and Godrej Properties on the basis of its focus on retirement and community housing — a segment gaining momentum in the wake of India’s ageing demographic trend.

Financially, Ashiana’s long-term performance depicts modest but rising fundamentals. Sales increased to Rs 698 crore (TTM), from Rs 529 crore in FY24, and operating profit also bettered to Rs 35 crore, which worked out to an OPM of 5%, from 3% in the previous year. The FY25 net profit of Rs. 36 crores was driven by increased project handovers and better pricing for the Bhiwadi and Jaipur projects. The company has also maintained a lean balance sheet with minimal debt (Rs 276 crore) and a robust reserve base of Rs 744 crore as a consequence of prudent financial management.

FY25 saw significant operational traction with the completion of previous low-margin projects (Anmol Phase 3, Malhar) and the launch of new projects in Bhiwadi, Chennai, and Jaipur. According to management, senior housing pre-sales would reach Rs 1,000 crore annually, and in FY26, development costs will double to Rs 425 crore. Additionally, it is aiming for 15–20% margins for FY27–FY30 with the aid of efficiency improvements and an improved project mix.

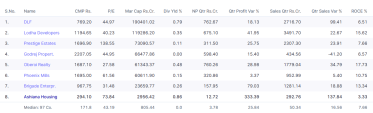

However, Ashiana’s return ratios are still poorly performing compared to its larger real estate peers. Large competitors such as DLF, Oberoi Realty, and Lodha substantially outperform Ashiana with ROCE levels of 6% to 17%. Ashiana has a diversified, senior living focused portfolio that reduces the risk of financial leverage, but it has still exhibited limited profitability and scalability.

Ashiana generates reliable and consistent cash flows, albeit not at the returns that other opportunities may offer given its solid track record, low leverage, and diversified senior living focus.

Peer Comparison of Ashiana Housing with Other Real Estate Companies

Due to its solid execution, low leverage, and focused senior living market niche, Ashiana remains a dependable but low-return investment for now. The extent to which the company can translate its operational momentum into sustainable shareholder value will depend on its appetite for monetizing its Rs 425 crore project pipeline, securing regulatory approvals faster, and accelerating margin recovery.

In the past one-year Ashiana Housing price is down 7.7%

Ashiana Housing 1-Year Share Price Chart

Conclusion

India’s elder-care story is no longer a story of social impact – it is becoming a potentially investable story. The demographic tide that once seemed far away is now rewriting balance sheets and business models in kind.

Players such as Max India and Ashiana Housing are pioneers in this sector, both operating at different points of the aging economy — one integrated care and assisted living, the other dedicated housing for seniors. While both have established well-credentialed operating bases and long-term project pipelines, profitability and returns are work in progress.

For investors, the “silver economy” is patience and promise. The potential is huge, but gestation is lengthy. Execution timelines, ramp-ups in occupancy, and regulatory clearances will decide how rapidly these pioneers can convert demographic tailwinds into sustained financial traction.

As India ages, the senior care market is only getting younger — and the firms that can marry economics with empathy might write the next decade of this stealthy but potent growth narrative.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Ekta Sonecha Desai has a passion for writing and a deep interest in the equity markets. Combined with an analytical approach, she likes to dig deep into the world of companies, studying their performance, and uncovering insights that bring value to her readers.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.