.")

A tug of war is currently going on between the Reserve Bank of India (RBI) and the government over Prompt Corrective Action norms for the Public Sector Banks. The Finance Ministry wants the central bank to relax its norms to enable more sanction of credit by PSU Banks, while the RBI wants to continue with tighter norms due to high non-performing assets (NPAs) ratio.

Media reports indicate that the FinMin has increased the pressure on the RBI to relax PCA norms amid liquidity issues in Non-Banking Financial Companies (NBFCs).

What is Prompt Corrective Action?

As the name suggests, Prompt Corrective Action is a quick corrective measure taken in case a bank is found to be having low Capital Adequacy Ratio (CAR) or high NPAs. RBI initiates PCA when CAR goes below 9% or NPA rises above 10%.

When RBI initiates PCA against a bank, it puts restrictions on fresh loans and dividend distribution. The actions could include stricter norms for lending, branch expansion, management change and asset reduction depending on the financial health of the bank.

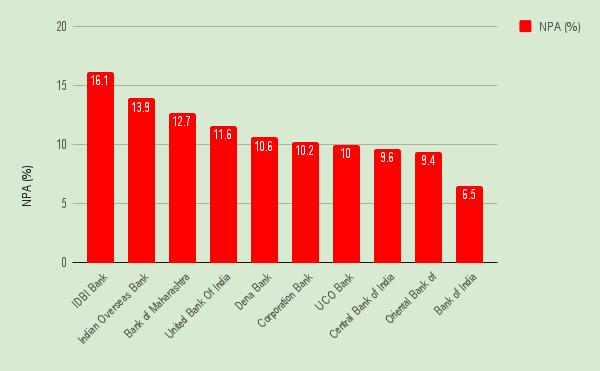

Why are 11 banks under PCA?

The RBI tightened the PCA norms when bad loans situation in the country got worse, with many PSU banks showing high NPA ratio. The RBI, so far, has put 11 PSBs under PCA with different degree of restrictions. These 11 banks are IDBI Bank, Indian Overseas Bank, Bank of Maharashtra, United Bank Of India, Dena Bank, Corporation Bank, UCO Bank, Central Bank of India, Oriental Bank of Commerce and Bank of India.

Rating agencies like Fitch have hailed the RBI’s decision to put stricter norms, saying that it would address the problems of struggling banks.

However, the government is of the opinion that the RBI should relax the PCA norms so that banks get to lend more amid the liquidity crunch in NBFCs following the crisis at Infrastructure Leasing and Financial Services (IL&FS).