By Abhishek Kumar & Divya Srinivasan

Lately, banks in India have witnessed a bright patch, with the largest scheduled commercial bank in India—the State Bank of India—recording a growth in net profit of 74% in Q2FY23, while UCO Bank and Canara Bank have recorded profitability growths to the tune of 59% and 145%, respectively. Their gross non-performing assets ratio (GNPA) as a percentage of Gross Advances improved to a six-year low of 5.9%. With increasing profitability, banks have been able to make enough provisioning, and the net non-performing assets (NNPA) ratio fell to 1.7% in March 2022. After a long period of deceleration in credit growth, caused by the twin-balance-sheet crisis of the 2010s, banks’ non-food credit growth has been strong and has hit double digits beginning April’22. On a year-on-year (y-o-y) basis, non-food bank credit registered a growth of 18.3% in October 2022.

Also Read: Focusing on corporate loan book: South Indian Bank MD Murali Ramakrishnan

These favourable developments in the banking sector are important for restoring a higher growth rate, which had been sliding well before the Covid-19 pandemic. Hence, it is important to understand whether this is a turnaround time for the Indian banking system, from last decade’s high levels of NPAs. If so, it is important to understand what factors have led to these improvements. Can banks use these higher profits to build a reserve to protect themselves during periods of crisis in the future, such as those that adversely affected them over the last decade?

Commodity Prices & NPAs

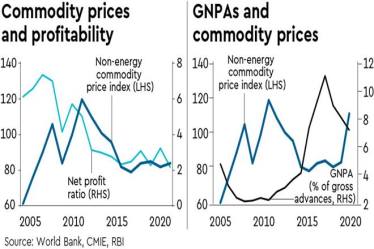

Since the beginning of the pandemic in March 2020, commodity prices have skyrocketed. According to data from the World Bank, the non-energy commodity price index has increased by about 80% between 2020-22, and metal prices have surged by over 105% in the same period. Costs have increased as well, although more slowly, leading to an increase in the average corporate profit margins from 13% in 2016 to over 15% in 2021. The profitability of corporates and NPAs in the Indian banking sector are tightly linked with global commodity prices (see graphic). The favourable outcomes for both banking and non-banking companies are driven by a recent surge in commodity prices. Kumar et al (2022) argue that a persistent decline in commodity prices between 2011-16 led to a decline in the profitability of firms in the commodity-sensitive sectors, rendering them unable to repay their debt (see graphic). Hence, the increase in non-performing assets of the banking sector. Banks did not have enough capital buffer, and, therefore, the scarcity of capital adversely affected credit growth.

The way ahead

Backed by the improved performance, banks have been generous in sharing their profits with their shareholders—in the form of dividends—in recent months. The government has been one of the biggest beneficiaries of this, with SBI alone paying a dividend of `3,600 crore. Like business cycles, commodity prices also undergo repeated cycles, but what is of importance to the financial sector and policymakers is that GNPAs and commodity prices are inversely related, with a correlation of -0.35. With commodity prices rising rapidly, it is important to be cognizant of the fact that, as with every cyclical movement, these prices will also cool down and may crash again as they did in the last decade. Now that commodity prices are on a rise, and profits are booming, banks should be prudent, unlike in the previous commodity boom.

Also Read: Yes Bank assigns Rs 48,000 cr stressed asset loan portfolio to JC Flowers ARC

Ben Bernanke, this year’s economics Nobel laureate, proved how bank failures could lead to financial crisis. In the previous episode of the commodity boom and the immediate afterwards, banks distributed most of these profits as dividends that later led to the scarcity of capital and build-up of non-performing assets when the commodity prices crashed during 2011-16. Analogous to the macro-prudential norms, it is advisable for banks to build a counter-cyclical commodity price buffer during upswings in commodity prices, which can be used during periods of downswings. As past experiences have taught us, inflation is harmful but deflation can be catastrophic. These buffers will reduce the commodity price risks and will provide banks with a cushion during a downturn in commodity prices, thereby reducing the adverse effects on financial intermediation.

The authors are Respectively, lecturer of economics, University of Southampton, and researcher, CSEP