")

The world’s most successful and followed super investor, Warren Buffett, also called the Oracle of Omaha, is known across the globe for picking the right stocks and sticking with them. But for sticking with them through all the ups and downs, he needed to trust them. And for that, he had a list of criteria the stocks had to fulfil. While the full list is not known to anyone apart from Buffett, we do know it in bits and pieces.

There are 3 areas where a company had to perform if it even wanted to be considered to be a part of Buffett’s holdings. The Holy Trinity Checklist – Return on Equity, Low Debt and Profits. While these are just the tip of the iceberg, these give a fair insight into the company on a financial front.

So, we ran a screen to find such stocks in India and found a few, out of which the following are two stocks that are among the top of the list. In short, they pass the Holy Trinity Checklist right now. They deserve a closer look.Note: This is by no means an exhaustive list. You should use this as a trigger to screen stocks yourself and find which all companies pass the Warren Buffett “Holy Trinity Checklist”.

Shilchar Technologies Ltd

Incorporated in 1986, Shilchar Technologies Ltd is into manufacturing of Electronics & Telecom and Power & Distribution transformers. Recently, the company has also ventured into the manufacturing of Ferrite transformers.

With a market cap of Rs 4,959 cr, the company is a leading manufacturer of power & distribution transformers and electronics & telecom transformers in India.

The Holy Trinity Checklist Test

Shilchar Technologies has a current ROE (Return on Equity) of 53%, while the current industry median is just about 16%. Which means that for every Rs 100 of shareholder equity (money invested by owners and retained earnings), the company makes a profit of Rs 53. Its average competitor or contemporary, however, makes a profit of just around Rs 16.

Even in the long term, the company averages an ROE of 45% while the industry averages just about 15%. So, it would be safe to say that the company is 3 times as efficient as its peers at turning shareholder investments into net income.

The compounded profit growth the company has recorded in the last 5 years is an impressive 151%, while the industry median is 38%.

And all these profits are in addition to the zero-debt status the company currently holds. Zero debt makes the company free from any high interest payments that eat into profits. Giving the company freedom to use the profits for buybacks, dividend payments or infusing it back into the business for growth purposes.

In the past 12 months, Shilchar Technologies Ltd has declared an equity dividend amounting to Rs 12.50 per share.

So, for all the 3 criteria of the Holy Trinity Checklist, the company is significantly outperforming the competition.

Plus, the company also boasts of a current ROCE of 71%, while the industry median is 19%. In simple words for every Rs 100 Shilchar uses as capital, it makes a profit of Rs 71 on it currently, while the overall industry averages just Rs 19.

When it comes to core financials, the company has logged in a compounded sales growth of 54% in the last 5 years.

The EBITDA (earnings before interest, taxes, depreciation, and amortization) for Shilchar grew at a 128% compounded growth between FY20 and FY25.

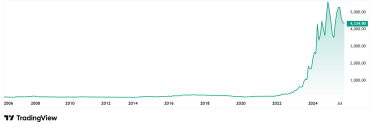

These numbers have helped the share prices of Shilchar Technologies, which was around Rs 60 in November 2020, to jump to Rs 4,335 as of closing on 31st October 2025. That is a jump of 7,125% in 5 years. Rs 1 lac invested in the stock 5 years ago would have been over Rs 72 lacs today.

Even at the current jump, the stock is trading at a discount of about 30% from its all-time high price of Rs 6,125 potentially creating a good entry point for interested investors.

As for valuations, the company’s current PE is 28x, while the current industry median is 39x. The 10-year median PE for Shilchar Technologies is, however, a modest 17x while the industry median for the same period is 27x.

In the FY25 annual presentation, the company’s Chairman & Managing Director, Alay Jitendra Shah said, “Our financial position remains one of our key strengths as we continue forward on this journey of growth and innovation. With a debt-free balance sheet and substantial net cash reserves, we are fully self-sufficient in pursuing future growth objectives through internal accruals alone”

Monolithisch India Ltd

Incorporated in 2018, Monolithisch India Ltd is a manufacturer of premixed high-quality ramming mass.

With a market cap of Rs 1,006 cr, Monolithisch is in the business of manufacturing and supply of specialized ramming mass, a heat insulation/lining material used as a refractory consumable for Induction furnaces installed in iron, steel, and foundry plants. The company also undertakes trading activities occasionally to meet excess and urgent customer demands.

The Holy Trinity Checklist Test

Monolithisch is recording a current ROE (Return on Equity) of 53%, while the current industry median is just about 13%. For the long-term view, the company averages an ROE of 55% while the industry peers average around 13%. Monolithisch is 4 times as efficient as its contemporaries when it comes to turning shareholder investments into net income.

The compounded profit growth the company has recorded in the last 5 years is 114%, which is much higher than the industry median of 20%. Just like Shilchar, Monolithisch is also operating at zero debt currently.

The one red flag, however, is that despite strong profits, the company is not paying out any dividends yet.

Apart from the 3 checks above, Monolithisch has a current ROCE of 61%, while the industry median is 17%. So, for every Rs 100 it uses as capital, it makes a profit of Rs 61 on it currently, while the overall industry averages just Rs 17.

Looking at the core financials, the sales of the company have grown at a compounded rate of 81% from Rs 5 cr in FY20 to Rs 97 cr in FY25. EBITDA jumped from Rs 1 cr in FY20 to Rs 21 cr in FY25, logging in a compound growth of 84%.

The share price of Monolithisch India at listing in June 2025 was around Rs 243, and as of closing on 31st October 2025 it was Rs 463, which is a jump of over 90% in just 4 months.

The company’s stock is trading at a PE of 57x, which is higher than the industry median of 40x. The 10-Year median PE for the industry is 26x, which we will have to wait and see how Monolithisch fares against in the long term.

Mukul Agarwal, one of India’s most followed super investors, bought a 2.3% stake in the company at listing in June 2025, which he has increased to 3% as per the filings for the quarter ending September 2025.

In the recent investor presentation from October 2025, the company’s Director of Investor Relations, Kritish Tekriwal said, “We are targeting somewhere around Rs 140 cr to Rs 160 cr revenue in this financial year… and somewhere around Rs 22 cr to Rs 24 cr in Profits After Tax”.

Time to Get the Warren Buffett Holy Trinity Checklist?

When it comes to picking stocks, most investors struggle to find what fits the best. In his 1988 letter to investors, Warren Buffett said, “Making the most of an already strong business franchise, or concentrating on a single winning business theme, is what usually produces exceptional economics”. And what we saw today are three themes that Buffett usually looks at.

Both the companies pass the test …making them contenders for anyone who follows Warren Buffett for investment intelligence. Add to this that both have strong future plans, which can be trustworthy given their performance in the last few years.

However, how these two stocks will fare in the short and long term is something that will be a great ride to watch. For now, how about adding them to a watchlist and following them closely?

Disclaimer:

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.