")

In a busy stock market, many small events go unnoticed. Yet, when Waaree Energies sold a 2.4% stake in its company, Indosolar Limited, people paid attention. At first, it looked like a routine step to follow SEBI rules. However, the sale tells us more than that.

Waaree Energies is not just any company. It’s India’s largest solar panel manufacturer. It has just reported strong profits with a y-o-y quarterly profit growth of 129.68%, and increased its capacity to 13.3 gigawatts. And is now exporting to big markets like the United States.

So, how does this sale, though small, fit into a much bigger plan – becoming the Reliance Jio of Solar?

This move shows Waaree is becoming more open, more organized, and ready to grow globally. It’s not just about making more solar panels; it’s about building a company that can lead India’s clean energy future, the way Tesla did in the electric car world.

The OFS Wasn’t About Compliance Alone

Waaree Energies sold 10 lakh shares of Indosolar through an Offer for Sale (OFS), reducing its holding by 2.4% at ₹265 per share.

On paper, this sale was meant to bring Indosolar closer to SEBI’s 25% minimum public shareholding norm, with the current public float at just 3.85%.

But take away this SEBI requirement, and the transaction will show you its bigger intent.

Waaree wants to create liquidity for Indosolar, make sure of its future monetization options, improve corporate governance, and reallocate Indosolar’s capital purposefully.

Just last month, Waaree had sold a 1.15% stake in the same subsidiary. This planned stake dilution tells you the parent is making Indosolar OFS-ready, and in the end, market-ready.

Market Stayed Steady, But the Volume Surged

Waaree Energies’ stock traded flat in the early hours when the OFS was announced, but gained ~ 9% in the two sessions leading up to the news.

Analysts believed the buying spree could be due to the stake sale news and strong earnings, which beat investor expectations on every front.

But Why Now?

Waaree acquired Indosolar in April 2022 as a part of the resolution plan submitted under the corporate insolvency resolution process (CIRP).

Why, then, did it launch the OFS now?

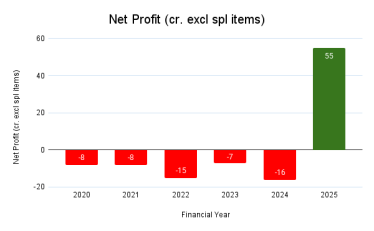

It’s because after Indosolar’s bankruptcy, for the first time in FY25, it reported a revenue of ₹ 324 crores, up from a revenue of ₹13 crores in FY2019. And course, as can be seen in the chart below, the company declared a profit too.

Indosolar’s Net Profit Trend (FY2020-2025)

It also helps that the market is bullish on renewable energy stocks. The Indosolar OFS follows a remarkable financial year for Waaree Energies.

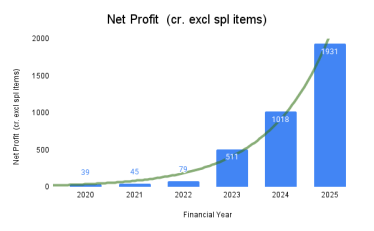

For FY25, Waaree Energies reported a consolidated net profit of ₹1,931 crore, compared to the ₹1,018 crore in FY24. Sales revenue stood at ₹14,444 crore, marking a healthy 26.73% year-on-year increase. The numbers exclude exceptional items.

The operating margins expanded significantly from 14% in FY24 to 19% in FY25. Waaree reported earnings before interest, taxes, depreciation, and amortization (EBIDTA) of ₹2722 crore in FY25, up from ₹1,575 crore in FY24.

The profit growth was driven by strong demand from domestic and overseas customers, competitive manufacturing costs, and increased manufacturing capacity utilization.

Net Profit Growth (FY 2020 -2025)

It doesn’t seem like a stressed company selling a stake to stay afloat. Waaree is flush with cash, generating consistent margins and growing fast. Q1 FY26 alone saw 1.2 GW of U.S. export orders.

Waaree still holds a 96% stake in Indosolar, though SEBI requires a minimum 25% public holding. The company, Indosolar, is still being revived, and Waaree will gradually reach the SEBI threshold.

This stake sale, then, is part of a bigger transition: from promoter-led, closely held capital to an established, liquid, and profitable entity. In short, if things go as planned, then investors could look forward to more OFS in the future.

Reading Between the Lines

Think of the Indosolar stake sale as more than a transaction. It is a signal of how Waaree Energies is preparing for four changes:

1. Restructuring Subsidiaries

Indosolar, once a stressed player, is now restructured under Waaree. It could create value without a formal spin-off by gradually reducing its stake. Doing so will allow the company to reposition Indosolar as a dedicated manufacturing arm or a PLI scheme recipient.

2. Governance Premium

SEBI’s minimum public shareholding (MPS) rules are for monitoring, but obeying them willingly before the deadline, without a steep discount, sends a message. Waaree wants to be seen in the same league as large institutional-friendly businesses like L&T or Tata Power Renewables.

3. Unlocking Valuation

The solar sector is buzzing. Companies like Borosil Renewables, ReNew Energy, and Servotech are all trading at stretched multiples. A separate valuation for Indosolar would help Waaree increase transparency in its group structure and command a better sum-of-the-parts valuation.

4. Capital Recycling

With a ₹265 floor price, the OFS raised ~₹26.5 crore. Small amount? Yes. But symbolic. It freed up capital, trimmed promoter concentration, and set an example for future, larger transactions.

Waaree’s Deeper Competitive Moat

While several solar firms in India are dependent on imports, Waaree Energies has built a rare vertically integrated model from wafers, solar panels, to EPC services. Its current module capacity is over 12 GW with a planned expansion of 20 GW by FY27. Indosolar will be an integral part of Waaree’s this PV capacity expansion master plan.

Compare this with Adani Solar with a ~4 GW, Vikram Solar with ~3.5 GW, and Tata Power Solar with ~4.3 GW capacity for solar cells and modules, and you realise. Waaree is quickly becoming the Reliance Jio of solar manufacturing, determined, disruptive, and structurally ahead of its competitors.

Waaree Energies is also aligned with India’s decarbonisation goals. The government wishes for 280 GW of installed solar capacity by 2030, compared to the ~73 GW now, with half of it sourced locally. Waaree is not just joining in this trend; it’s defining it.

Global Expansion – The Next Step

Not content with domestic dominance. Waaree is expanding globally, particularly into the U.S., where supply diversification and anti-China sentiment have opened doors for Indian solar players.

Waaree commenced operations at its 1.6 GW solar plant in Texas in January 2025, making it the first Indian company to manufacture modules in the US. It will compete with First Solar, QCells, and Canadian Solar in the US market.

It secured a 599 MW solar module supply contract for a U.S. project, with a pipeline of ~1.9 GW in booked export orders as of Q1 FY26. It is in early-stage discussions with distributors and EPC players in Germany, Spain, and Italy, markets that are pushing for clean energy after the Russian energy crisis.

These projects will not only expand its revenue streams but also shield the company from seasonal domestic policy changes. However, it also brings exposure to currency instability, trade compliance risks, and local ESG norms.

What Investors Should Watch For

As Waaree moves from a high-growth domestic story to a globally visible energy tech player, new risks and factors will come into play. Here are six areas investors should watch for

1. Currency and Interest Rate Exposure

With significant export orders and upcoming operations in the U.S., Waaree will face USD-INR fluctuations. The company’s dollar-denominated contracts and potential cost inflation in the U.S. due to labor and logistics could affect margins. Rising U.S. interest rates may raise the cost of capital for its foreign projects.

2. PLI Scheme and Policy Change

While the Indian government’s production-linked incentive (PLI) scheme provides capital subsidies for solar cell/module manufacturing, it also expects strict localisation and execution benchmarks. Delays in fund payouts or changing government priorities could disturb planned capacity expansions.

3. External Growth Execution Risks

Setting up a U.S. plant is a capital-intensive move with multiple execution bottlenecks such as local compliance, labor shortages, and delays in approval. Mistakes here could affect the consolidated profit & loss and disrupt investor prospects.

4. Global Price Pressures

The global solar industry prices are declining due to oversupply from China. While Waaree’s backward integration may help on costs, it must keep pace on productivity, size formats (e.g., TOPCon or bifacial panels), and customer customization to sustain pricing power.

5. Sustainability & ESG

With growing interest from external investors, especially ESG-focused funds, Waaree must build credible sustainability disclosures. Tracking its carbon emissions, water use in manufacturing, and supply chain sourcing will gradually become more important if the company wants to be globally relevant.

6. Valuation Risk

At a P/E of ~49.1×, Waaree is priced for continuous earnings growth. Any instability in order inflows, execution, or external shocks like U.S. policy shifts or global supply chain disruptions could lead to sharp re-ratings.

Waaree’s Bigger Vision

The Indosolar OFS is not just a transaction; it’s a rebirth. From a promoter-heavy holding structure to a cleaner, institution-friendly entity. The solar economy is entering a new phase.

Waaree wants to lead that charge, not just in gigawatts, but in governance, growth, and global credibility. How much Indosolar will contribute to Waaree’s module expansion remains to be seen.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Archana Chettiar is a writer with over a decade of experience in storytelling, and, in particular, investor education. In a previous assignment, at Equentis Wealth Advisory, she led innovation and communication initiatives. Here she focused her writing on stocks and other investment avenues that could empower her readers to make potentially better investment decisions.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.