The Indian stock market has witnessed increased volatility in recent months, driven by global macroeconomic uncertainties, rising interest rates and geopolitical tensions.

Amid this broader correction, the defence sector—once a market darling—has also seen a pullback.

Despite strong order books and long-term growth potential, several defence stocks have come under pressure due to concerns over execution delays, margin pressures, and a temporary slowdown in order inflows.

However, with the Indian government’s continued push for self-reliance in defence manufacturing and increasing capital expenditure in the sector, these stocks could be poised for a rebound.

Many defence companies continue to report steady revenue growth, high return ratios and strong balance sheets, even as their stock prices have declined significantly from their peaks.

This has resulted in some defence stocks now trading at attractive valuations relative to their historical averages.

In this report, we highlight four such undervalued defence stocks that have seen sharp corrections but remain fundamentally strong.

While short-term pressures persist, their long-term growth prospects and strategic importance in India’s defence ecosystem make them compelling investment opportunities.

Mazagaon Dock Shipbuilders

First on the list is Mazagaon Dock Shipbuilders.

Mazagaon Dock Shipbuilders builds and repairs warships, submarines and other vessels for the Indian Navy, Coast Guard, and ONGC.

The company’s diverse portfolio includes cargo ships, passenger liners, water tankers, fishing vessels, destroyers, submarines, and corvettes.

Shares of Mazagaon have corrected 27% from their recent highs of Rs 2,930, as order execution challenges and working capital constraints weighed on sentiment. Moreover, the company is saying that the revenue growth might slow down in the coming year.

However, with a Rs 347 billion order book, as of 31 December 2024 and a strong growth pipeline, the stock remains attractively valued.

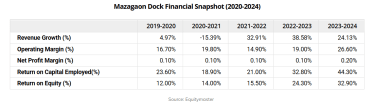

Between 2020-24, the company has reported consistent growth with sales and net profit climbing at a 5-year compound annual growth rate (CAGR) of 11.2% and 21.6%.

The company has achieved this growth without incurring any debt. The returns have also been admirable, with the Return on Capital Employed (RoCE) and Return on Equity (RoE) averaging at 24.4% and 16.3%, respectively.

Going forward, the company is planning heavy capital expenditure for its dry dock over the next 1.5 years, which could lead to higher sales and profits.

It is venturing beyond shipbuilding, exploring underwater heavy engineering equipment and offshore platforms.

Additionally, it is making efforts to export offshore patrol vessels to countries in Southeast Asia, Latin America, and Africa.

The stock is trading at a PE of 31.2, near its historical median but at a discount to its peak PE of 59.2.

Cochin Shipyard

Next on our list is Cochin Shipyard.

Cochin Shipyard holds a prominent position in the construction and maintenance of a wide range of maritime vessels, encompassing tankers, product carriers, bulk carriers, passenger ships, and defence vessels.

Shares of Cochin Shipyard have declined 18% in 2025 so far, and over 50% from recent highs. It’s weighed down by revenue fluctuations and margin pressures.

Despite this, the company remains a key player in India’s maritime defence sector, being the only shipyard in the country capable of constructing vessels with a deadweight tonnage (DWT) of up to 110,000 and repairing vessels of up to 125,000 DWT.

In addition to defence shipbuilding, it has diversified into inland and coastal shipping, the fishing industry and the cruise and ferry markets.

Over the years, it has built expertise in defence vessels, progressing from bulk carriers to smaller, technologically advanced ships, like platform supply vessels and anchor-handling tug supply vessels.

As of 30 June 2024, Cochin Shipyard’s order book stands at Rs 225 bn, providing strong revenue visibility. This includes Rs 215 bn for shipbuilding, with the balance designated for ship repair.

Looking ahead, the company is expanding at Cochin port with a Rs 20 bn investment. Industry analysts highlight the urgent need to increase India’s shipbuilding capacity as global shipyards are fully booked until at least 2028.

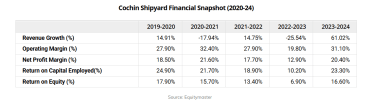

Between 2020-2024, the company’s sales and net profit have reported a CAGR of 15% and 30%, respectively.

In FY23, the company experienced a decline in revenue due to a weakened order book. This decline was primarily attributed to concerns stemming from the pandemic.

The 5-year average RoCE and RoE stood at 28.5% and 19.6%, respectively.

The stock is currently trading at a PE of 40.6, significantly lower than its all-time high of 91 but still at a premium to its historical median of 33.3.

Bharat Electronics

Third on the list is Bharat Electronics.

Bharat Electronics caters to the Indian armed forces providing radar, communication. and electronic warfare equipment.

The company’s product portfolio is quite diverse, encompassing defence and non-defence products such as software and electronic manufacturing services.

In addition to serving the domestic market, Bharat Electronics also exports its goods to various nations, such as Botswana, Indonesia, Sri Lanka, Russia, the United States, and South Africa.

Over the years, the company has established multiple growth drivers by developing a robust infrastructure, fostering strong relationships with government entities and venturing into non-defence sectors to create new avenues for expansion.

Despite strong fundamentals, shares of Bharat Electronics have declined 46% from their highs and over 23% in 2025, pressured by concerns over government order delays and prolonged working capital cycles.

However, it has a robust Rs 700 bn order book with expectations of an additional Rs 250 bn in orders by the end of FY25.

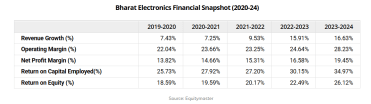

Between 2020 and 2024, the company reported a 5-year CAGR of 11.2% in sales and an impressive 16.4% in net profit. Its returns remain strong, with average RoCE and RoE exceeding 29.2% and 21.4%, respectively.

The stock is trading at a PE of 36x, below its historical median (5 year) of 25x and its peak PE of 61x.

Hindustan Aeronautics

Fourth on the list is Hindustan Aeronautics.

Hindustan Aeronautics (HAL) is a play on the growing strength & modernisation of India’s air defence. Its significant presence is evident, with approximately 80% of the defence force’s fleet being supplied or serviced by the company.

The company has been advancing its technologies, evidenced by the development of more sophisticated platforms.

What’s even more exciting is that it has successfully transitioned from manufacturing products through licensed production to establishing a range of homegrown designs.

This places the aerospace giant in a sweet spot to capitalise on the long-term, sustainable demand created by the government’s commitment to procuring indigenous defence aircraft.

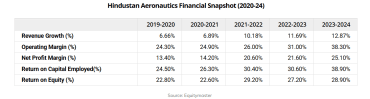

HAL’s sales have been growing smoothly. Between 2020-24, the sales and net profit have grown at a CAGR of 9.6% and 26%, respectively. The returns have been admirable, reporting an average RoCE and RoE of 30% and 26%, respectively.

Shares of HAL have declined 45% from their recent highs and over 25% in 2025, driven by near-term project execution concerns.

However, with a robust Rs 1.33 trillion (tn) order book as of December 2024—set to rise to Rs 2.5 tn by FY26—alongside Rs 1.65 tn in expected fresh orders over the next 12 months, the company’s long-term growth outlook remains strong.

It has also planned Rs 145 bn capex over five years for capacity expansion and modernisation.

HAL is poised for significant order inflows, with Rs 1.3 trillion worth of contracts for 97 LCA Tejas Mark 1A and 156 LCH Prachand at an advanced stage of clearance, expected to materialise within the next three to six months.

This, along with upcoming orders for the Su-30MKI upgrade, Indian Multi-Role Helicopter (IMRH) development, and regular maintenance work, will further bolster its order pipeline.

With Maharatna status, a healthy backlog and strong revenue visibility, HAL remains well-positioned to capitalise on India’s growing defence expenditure and push for self-reliance in manufacturing.

The stock is trading at a PE of 23.9, above its historical median but below its peak PE of 48.9x.

Avantel

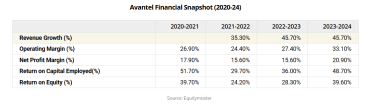

Avantel, a key player in wireless and satellite communication, designs and develops defence electronics, radar systems and network management software for aerospace and defence sectors. Despite a robust long-term growth trajectory, the company’s stock has faced headwinds recently.

Shares of Avantel have plunged 50% from their 1-year high and are down over 30% since the start of 2025, weighed down by weak earnings performance.

In Q4FY25, the company’s net profit declined 8.8% YoY, while sequentially, profits saw a steep 39% drop. The disappointing results triggered a sharp sell-off, with the stock hitting a 10% lower circuit post-announcement.

However, its long-term fundamentals remain strong.

Avantel has strengthened its order book with multiple contract wins, the most notable being a Rs 1 bn order from the Ministry of Defence on 30 May 2024, for SATCOM equipment. This follows earlier orders from Mazagon Dock Shipbuilders and Bharat Electronics in May, marking its third major deal within a month.

Over the past four years, Avantel’s revenue has grown at a CAGR of 68.7%, while net profit has more than tripled.

This has translated into impressive return ratios, with a five-year average RoCE of 40.9% and RoE of 30.4%. The company remains almost debt-free, with a debt-to-equity ratio of 0.07 as of March 2024.

The stock is trading at a PE of 41.3, well above its historical median but below its peak PE of 91.9.

Conclusion

As India reduces its reliance on imports for military equipment and domestic manufacturers secure advanced orders, the defence sector presents a compelling investment opportunity for those willing to conduct thorough research and analysis.

Despite its promising outlook, understanding the industry’s dynamics and associated risks is crucial before investing in defence stocks.

While the sector holds immense potential, it also faces challenges. Dealing with the government, its primary client, can be arduous due to high receivable days and orders that are heavily reliant on defence budget allocations.

Substantial capital outlays often necessitate external funding, impacting companies’ balance sheets.

Furthermore, Indian firms encounter obstacles in accessing advanced technology essential for developing modern defence equipment, posing a significant challenge in obtaining expertise at competitive prices.

Despite these challenges, the defence sector’s growth prospects remain robust, making it an attractive investment avenue for those prepared to navigate its complexities.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such. Learn more about our recommendation services here…

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.