")

Before one invests in a company, they mostly do their own research to try and find the pros and cons of the company. Most investors have a checklist that helps them pick stocks that fit the bill. But how about this activity is taken care of already?

You see, when the smart money, or investments from FIIs and DIIs flow into a stock, it is a given that these giants have already dug in enough into the stock. After all, they do not invest blindly and have a bigger and better checks & balances than all individual investors. So, when a company has a substantial stake by smart money, it deserves attention of smart investors.

Today we look at 2 stocks that are leaders in their own industries and are backed by FIIs and DIIs alike. Not to forget, they have recorded some solid profit growth in the last few years.

Dalmia Bharat Ltd

Established in 1939, Dalmia Bharat Ltd is engaged in the business of Manufacturing and Selling of Cement.

With a market cap of Rs 42,360 cr, Dalmia Bharat Ltd is the 4th largest cement manufacturer by installed capacity in India with more than 49,300 channel partners serving 23 states.

FIIs have an 8.3% stake and DIIs have another 17.4% stake in the company, making a combined total of a little over 25% by Institutional investors or smart money.

Names like Nippon India, Mirae Asset, SBI Mutual Fund and LICI Ulip hold stake when it comes to domestic institutional investments.

The sales for Dalmia Bharat grew from Rs 9,674 cr in FY20 to Rs 13,980 cr in FY25, logging in a compound growth of 8% in 5 years.

The EBITDA (earnings before interest, taxes, depreciation, and amortization) went from Rs 2,083 cr to Rs 2,407 cr in the same period, marking a compound growth of a 3%.

The net profits grew at a compound rate of 30% between Rs 238 cr in FY20 to Rs 699 cr in FY25.

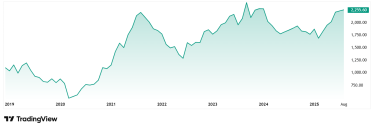

The share price of Dalmia Bharat Ltd was around Rs 775 in August 2020 and as of 11th August it was Rs 2,258, which is a growth of 191%. Rs 1 lac invested in the stock 5 years ago would be Rs 2.91 lacs today.

The company’s share is trading at a PE of a 46x, which is closer to the industry median which is 45x.

According to the company’s latest investor presentation from July 2025, Dalmia Bharat is entering a phase of aggressive, yet disciplined, capacity expansion with a clear focus on profitable growth, cost leadership, and brand strengthening. The company is navigating industry consolidation, regulatory uncertainties, and cyclical demand with a long-term, risk-managed approach. Management remains highly confident in India’s cement sector prospects and Dalmia’s ability to capitalize on them.

Great Eastern Shipping Company Ltd

Incorporated in 1948, Great Eastern Shipping specializes in the transportation of crude oil, petroleum products, gas, and dry bulk commodities.

With a market cap of Rs 13,301 cr the company is a major player in the Indian shipping and Oil drilling services industry. It is India’s largest private sector shipping company, owning, and operating 39 ships and 23 offshore assets.

Smart money holds almost a 40% stake in the company, with FIIs holding 25% and DIIs holding 15% stakes, respectively.

Government Pension Global Fund, City of New York Group Trust, Vanguard Total International Stock Index Fund are the foreign institutional investors in the list. And in case of DIIs- HDFC Funds, UTI Fund, Kotak Mutual Funds, ICICI Prudential and Bandhan Mutual Funds are the names that hold stakes.

The company’s sales jumped from Rs 3,687 cr in FY20 to Rs 5,323 cr in FY25 which is a compound growth of 8% in 5 years.

EBITDA also grew from Rs 1,217 cr in FY20 to Rs 2,677 cr in FY25, logging in a compound growth of 17%.

When it comes to Net Profits, the company saw losses in FY18 and FY19 but turned around to see profits of Rs 207 cr in FY20 and since then hasn’t seen any losses. In FY25, the company recorded profits of Rs 2,344 cr. That’s a compounded growth of an enviable 85% between FY20 and FY25.

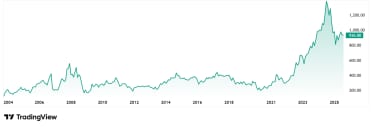

The share price of Great Eastern Shipping Company Ltd was around Rs 260 in August 2020 and as on 11th August 2025, it was Rs 932, which is a growth of almost 259%. Rs 1 lac invested in the company 5 years ago would have been close to Rs 3.6 lacs today.

Even at the current price of Rs 932, the company’s share is trading at a discount of almost 40% from its all-time high price of Rs 1,544.

The company is currently trading at a PE of 8x, which is lower than the current industry median of 12x. The 10-year median PE for the company is 7x.

According to the recent investor presentation in August 2025, Great Eastern Shipping delivered a resilient Q1 FY26 despite YoY normalization in rates, with strong cash generation, prudent cost control, and a conservative capital allocation stance. The company remains primarily spot-exposed and is focused on asset renewal, not expansion, in a market characterized by high volatility and shifting global trade patterns. Offshore rig market softness and high orderbooks in tankers are key headwinds, but management remains disciplined, with no aggressive capital deployment planned unless compelling opportunities arise.

The Investor Verdict: A Smart Bet or a Cyclical Trap?

Institutional Investors know their investments and they don’t invest easily. With strong processes that includes very stringent checks and balances, these investors ensure that only the most potent opportunities get the smart money. However, nothing is fool proof and there are always risks associated.

Will these 2 industry leaders who are profit pioneers as we saw, and delivered good stock price gains, be able to continue this streak of strong financials? Will they be able to sustain the investments from domestic and foreign institutional investors?

Only time will be able to tell that, but for now, the intelligent next step will be to add these industry leaders to your watchlist and keep a very keen eye on them.

Disclaimer:

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.