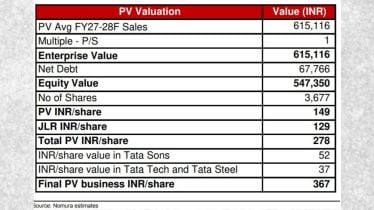

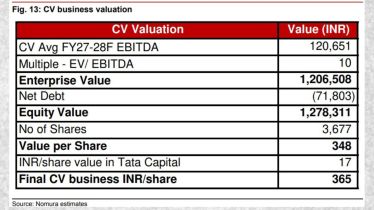

The Tata Motors share price has been in focus as the valuations got adjusted after the record date for the demerger. As the Commercial Vehicle (CV) and Passenger Vehicle businesses begin their independent stock market journey, the question is, what is the right value for the stock? The fair value post-demerger is a crucial number to follow. Nomura’s target price is split almost evenly between the two entities at Rs 365/share for the CV entity and Rs 367/share for the PV entity.

Tata Motors Group Automotive Business

| Tata Motors Commercial Vehicle | Tata Motors Passenger Vehicles | Jaguar Land Rover (Part of PV biz) |

| TML CV Holdings Pte. | TML Holdings Pte | Jaguar Land Rover Group |

| TML Smart City Mobility Solutions | Tata Auto Comp | |

| Tata Motors Body Solutions | Tata Passenger Electric Mobility | |

| Tata Daewoo Mobility Company | Fiat India Automobiles | |

| TML CV Holdings BV | Tata Technologies | |

| PT Tata Motors Indonesia | Group Investments and Others | |

| Tata Motors Finance Holdings | ||

| Tata Marcopolo | ||

| Tata Cummins | ||

| Tata Hitachi | ||

| ACGL | ||

| Nita Co Ltd | ||

| TMIBASL |

Tata Motors PV entity: What’s included

The first step to understanding the value of the shares is knowing what the business comprises. Tata Motors’ PV entity will consist of the domestic PV business, Jaguar Land Rover, the company’s stake in other Tata Group entities like Tata Sons, Tata Steel, and Tata Technologies, and other investments.

Tata Motors PV Business: Nomura lists the big drivers

Nomura listed out the big drivers for Tata Motors’ PV business, including the ongoing boost to the festive season as a result of the GST new rates.

GST new rates: The momentum in the domestic passenger vehicle space has definitely seen some uptick after the GST cut as festive and pent-up demand kicked in. Nomura added that the “premiumisation trend remains evident, with a surge in bookings for compact and micro SUVs including the Punch and Nexon.”

New launches: The passenger vehicle sales have got a boost as a result of the recent launches too. The recently unveiled Harrier EV has also seen an encouraging initial response, with bookings surpassing early expectations. The management targets double-digit EBITDA margins in the medium-term from 3.9% levels in Q1FY26. Nomura pointed out that this will be “aided by richer mix, improved pricing, and cost efficiencies.”

JLR operations resume: In good news for the Tata Motors luxury vehicles arm, operations have now started in phases across different facilities of Jaguar Land Rover after the shutdown following the cyberattack last month. “While demand has not had any significant impact, as per management, production should pick up in coming weeks,” Nomura added. Their “FY26 and FY27F EBIT margin estimates for JLR are 6.2%/7.6%.” According to the international brokerage house, “the management guidance is 5-7% EBIT margin for FY26 and zero free-cashflow. This might have some downside risk.”

Tata Motors CV entity: What’s included

A look now at the CV entity. This will consist of Tata Motors’ domestic CV business, Iveco (acquisition to be completed in 2026) and the stake in Tata Capital, the NBFC arm of Tata Group that made a debut on Dalal Street recently.

Tata Motors CV Business: Nomura lists the big drivers

In terms of growth drivers, the Tata Motors’ management expects the overall CV industry to grow 5% in FY26. According to Nomura, this “implies 10% growth in H2FY26 helped by GST reduction.”

The CV business will also include the Iveco acquisition from April 2026. The 3.8 billion acquisition is set to be financed through debt initially and 40% equity later. At this stage, Nomura is not assuming any “value creation from this acquisition.” They pointed out that the company has guided a 5% revenue growth annually on a compounded basis and EBIT margin growth to 7.5% from 5.4% between 2024-2028.

According to Nomura, “Iveco’s H1CY25 results indicate its performance has slipped YoY with a revenue decline of 9% and EBIT margins ex-Defence of 3.7% (Vs 6.3% in H1CY24).”

Overall, Nomura is maintaining a Neutral rating and will update estimates once pro forma financials are available post-results. However, they pointed out that the “reduced weight in indices could pose a technical risk for the share price.”