Once written off, Reliance Power is one of the most talked-about and intriguing revival story of 2025 so far. Well-known for its delayed projects and massive loans, the company seems to be on its way to becoming profitable. It has raised capital, won clean energy projects, and is commanding a market cap of over ₹27,000 crore.

The share price of Reliance Power surged over 113% in the past year, generating humongous investor interest. But behind this sudden rise, is there a real business story that’s being written?

Is this turnaround rally for real?

Perhaps, no. You see, six structural changes happened at Reliance Power within the past 18 months. For this rally to be real, we need to know what lies ahead for the company.

Let’s dive deep and understand what’s driving Reliance Power in 2025 and what lies ahead.

The numbers tell the story

Reliance Power’s turnaround can be seen considering that from a loss of ₹377.6 crore in Q4 FY24 the company generated a profit of ₹125.6 crore in Q4 FY25. On an annual basis, it posted a net loss of ₹2,033 crore in FY24, which reduced to a loss of just ₹183 crore in FY25. All numbers exclude exceptional items.

The Earnings before interest, tax, depreciation and amortisation (EBITDA) in Q4 FY25 leaped to ₹ 590 crores from ₹186 crores a year ago. Meanwhile, the EBITDA margin rose to 30% from 9% the previous year. The yearly revenue was ₹7,583 crore.

This turnaround has driven market re-rating. The stock surged by over 113% in 12 months. It gained 48% in the past month alone, though profit-booking led to short-term corrections. As of June 2025, its market capitalization was ₹26,283 crore.

| Fundamentals at a Glance | ||

| Metric | FY25 | |

| Market Cap (June 2025) | ₹26,282 crore | |

| Share Price | ₹63as of 23rd June | |

| Consolidated Revenue | ₹7,583 crores | |

| Net Profit | – ₹183 crore | |

| Net Profit (Q4) | ₹126crore | |

| EBITDA (Q4 FY25) | ₹590 crore | |

| Installed Capacity | ~5,945 MW (5760 MW thermal & 185 MW Renewal Energy) | |

| Clean Energy Pipeline | 2.4 GWp Solar, 2.5 GWh Battery Energy Storage | |

What sparked the turnaround?

Numbers alone don’t explain the turnaround. To understand the recovery, we must understand the six factors driving the change.

1. Return to profitability after years of losses

Reliance Power had a consolidated net profit of ₹2,948 crore in FY25 (including exceptional items), a dramatic change from a loss of ₹2,068 crore in FY24. Efficient capacity use, lower costs, and profits from the Sasan UMPP drove these gains. (Financial Express)

Reliance Power: EPS Trend (FY20-FY25)

2. Explosive stock performance and market recognition

The stock delivered a 113% return over 12 months, climbing to a multi-year high of ₹71.24 on 11th June. The stock surged even under SEBI’s high-volume scrutiny

3. From thermal burden to clean energy leadership

Reliance Power was among the largest private coal-based power producers in India with a thermal operating capacity of 5,760 MW. Most of this capacity was from the Sasan Ultra Mega Power Project (UMPP) and other thermal assets. While these plants are still in use, they are no longer the sole drivers of growth.

The company has shifted to renewable energy, and not as a show but in significant capacities.

- A 350 MW solar project with SJVN and a 175 MW battery storage is one of the rare integrated project models.

- A ₹2,000 crore joint venture with Bhutan’s Druk Holdings. It will develop a 500 MW solar plant, the largest of its kind in the country.

- It won a 930 MW integrated solar project. It is one of Asia’s largest, with a 25-year agreement to buy power.

Together, these projects add to 2.4 GWp in solar and 2.5 GWh in battery storage systems. It gives Reliance Power one of the largest hybrid clean energy pipelines in India.

4. Capital infusion and promoter backing

In October 2024, the company raised ₹1,525 crore via a preferential share issue, and another ₹348 crore in May 2025. What’s important is the promoter’s participation with Reliance Infrastructure, increasing its stake.

What mattered here isn’t the money; it’s who backed the raise. Promoters, including Reliance Infrastructure, increased their stake, indicating high conviction.

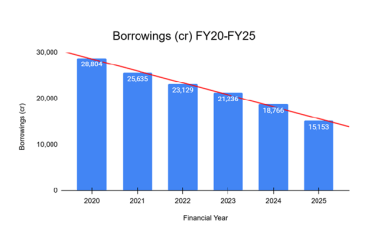

5. Balance sheet repair and debt reduction

The company has reduced debt, cutting it from ₹ 28,804 crores in FY20 to under ₹15,153 crores by FY25.

This isn’t financial engineering. The debt reduced as Reliance Power monetized its assets, controlled costs, and improved its receivables. The company’s debt-to-equity ratio stabilized, and interest coverage improved. Thanks to improved cash flows from the Sasan UMPP and Rosa thermal plants.

Reliance Power: Debt Reduction (FY20-FY25)

In FY25, the company improved its working capital cycle. It increased collections from state utilities and lowered corporate overheads. Such efforts rarely make headlines, but are essential to sustainable profits.

6. Legal clearance on bidding eligibility

In 2025, the Delhi High Court let Reliance Power bid for government tenders again. The company bid in central and state-backed solar auctions and hybrid storage projects. These were projects that they could offer at competitive costs.

Investor interest: Not just traders anymore

The rally in Reliance Power stock was sharp and volatile. The share price more than doubled in 12 months. Then corrected in June 2025 after hitting a short-term peak. NSE put the stock under Additional Surveillance Measures (ASM) due to high volumes.

But beneath this froth, the shareholder base is changing. FIIs now own a larger chunk of the company as compared to just a couple of years ago. The public shareholding, on the other hand, has declined.

Why it still demands caution

Even well-executed turnarounds come with risk. For Reliance Power, there are three investor red flags to keep an eye on:

Execution risk: The 930 MW and Bhutan solar projects are complex. Delays in commissioning or cost escalations could dent credibility and margins.

Profit consistency: FY25’s profit included gains from one-off writebacks and debt restructuring. FY26 will need to prove that this is sustainable, operational profit.

Market volatility: The stock rose over 113% in a year, as per Screener. A decrease in earnings or negative news could mean share price corrections.

Investors must look for consistent profits, better receivables management, and project updates. Not price action.

What investors must still watch out for?

Even with these tailwinds, Reliance Power is not risk-free. Here’s what investors must check before considering this turnaround stock:

1. Execution of mega projects

The company may have won large, complex projects. But the timely execution of these projects is a must. Any delay or cost overruns could dent profitability and strain their credibility.

2. Debt sustainability and repayment plan

Though debt has declined to ₹15,153 crores in FY25 is still a sizable amount. Investors must watch for upcoming maturities. They must check working capital financing and capital expenditure on new projects. It could increase debt unless managed.

3. Earnings quality and recurrence

FY25 saw one-time recoveries and writebacks. But, consistent earnings in FY26 derived from power generation and sales are what you must watch for.

4. ASM framework and volatility

The stock has been under NSE & BSE Additional Surveillance Measures (ASM). Short-term volatility may remain high, especially due to market events and changes in investor sentiment.

5. Project financing and equity dilution risks

Large projects need massive capital expenditure. Issuing more shares to meet these costs can dilute shareholder value. But only if Reliance Power increases its revenue and margins.

6. Regulatory and political uncertainty

Energy is a regulated space. Tariff policy, green energy incentives, or international rules can impact the project. Keeping an eye on these changes would help investors make the right decisions.

7. Promoter involvement and cross-holding risks

The company’s management may have improved, but investors are cautious of its past dealings. Continued transparency will be critical.

8. Sectoral competition

The company competes with NTPC, Adani Green, ReNew, and Tata Power. Winning Power Purchase Agreements at sustainable tariffs will be a challenge Reliance Power must overcome.

9. Sustainability of clean energy margins

Solar + Battery Energy Storage Systems are capital-intensive. Investment returns will depend on effective capacity use and foreseeable grid access. The company’s operating margins could change during the execution of these projects.

What’s next: Execution, not euphoria

Will Reliance Power execute its projects, reduce loans, and maintain consistent profits? There are risks, and managing those will be crucial for Reliance Power.

Disclaimer

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Archana Chettiar is a writer with over a decade of experience in storytelling, and, in particular, investor education. In a previous assignment, at Equentis Wealth Advisory, she led innovation and communication initiatives. Here she focused her writing on stocks and other investment avenues that could empower her readers to make potentially better investment decisions.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.