")

Porinju Veliyath is a well-known and highly followed super investor, who deserves to be on our list of Indian Warren Buffetts. With a holding of 12 stocks worth Rs 212 cr, he has time and again proved his expertise in making the right moves at the right time.

He is also the founder of Equity Intelligence India Pvt Ltd, a portfolio management service (PMS) provider. Known for his value investing approach and contrarian investment strategies, Porinju is widely renowned for bold investment decisions.

He has recently made three big changes to his holdings, that have caught the attention of investors across. These changes include a fresh addition, increased stake in one existing holding and shockingly enough, buying back into a stock he sold off last quarter.

The U-Turn – A bet on a turnaround?

Incorporated in 1983, Ansal Buildwell Ltd is in the business of promotion, construction and development of integrated townships, residential and commercial complexes, multi storied buildings, flats, houses, apartments.

With a market cap of Rs 76.9 cr (yes, it’s tiny), the company has trade offices in Moscow, Russia; Dubai, UAE; Bangkok, Thailand and Dhaka, Bangladesh.

The company was facing a CIRP petition (Corporate Insolvency Resolution Process) filed by IDBI Trusteeship Services Ltd. However, on 13th March 2025, NCLT (National Company Law Tribunal) allowed IDBI Trusteeship Services Ltd. to withdraw its CIRP petition. As a result, the insolvency proceedings were dismissed, which came as a huge relief for Ansal Buildwell.

Porinju Veliyath held a stake in the company through Equity Intelligence India Pvt Ltd since at least as far back as March 2016 (as per Trendlyne). At the quarter ending March 2025, the holding was 2.7%, which went below 1% when the filings were done for the quarter ending June 2025. Which meant a complete or partial exit.

However, as per the exchange filings for the quarter ending September 2025, Veliyath has once again bought 2.7% stake (worth Rs 2.1 cr), through Equity Intelligence India Pvt Ltd. This makes it more interesting as we try and decode the strategy behind the sell and the re-entry.

Especially because the past financials at best present a mixed picture.

The company’s sales saw a drop from Rs 63 cr in FY20 to Rs 49 cr in FY25. The EBITDA however saw a compounded growth of 5% as it went from Rs 11 cr to Rs 14 cr in the same period.

When it comes to profits, the company has shown some promise and a solid turnaround if we can call it that. From profits of Rs 46 lacs in FY20 to Rs 8 cr in FY25, the profits grew at a compounded rate of 80%.

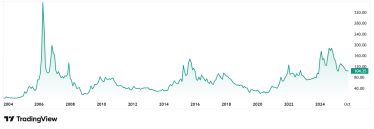

The share price of Ansal Buildwell jumped from around Rs 31 in November 2020 to its current day price of Rs 104 as of closing on 7th November 2025.This is a jump of 235% in 5 years. Rs 1 lac invested in the stock 5 years ago would have been Rs 3.35 lacs today.

At the current price of Rs 104, the share is trading at a discount of 79% from its all-time high price of Rs 460.

The company’s share is trading at a PE of 52x while the current industry median is 40x. The 10-year median PE for Ansal is 7x and the industry median for the same period is 25x.

In the last annual report, the management said they are hopeful and optimistic about long-term prospects, positioning the company to contribute to growth in NCR and other infrastructure-linked cities. The focus areas will be luxury gated communities, integrated townships, and commercial destinations.

The company also declared an equity dividend of Rs 1 per share with a record date of 19th September 2025.

So while the historical data offers a mixed picture, the company appears to be on the mend, and this super investor wants to make the most of the opportunity.

A loss-making fresh buy in the alcohol industry

Tinna Trade Ltd, a listed company acquired Fratelli Wines Pvt Ltd. Following the transaction, the company was rebranded as Fratelli Vineyards Ltd, and its shares are now traded on the Bombay Stock Exchange (BSE).

With a market cap of Rs 606 cr, the company is India’s leading premium winemaker, established in 2007 with operations spanning vineyard cultivation, wine production, and distribution. The company operates on a “grapes-to-bottle” model, owning 400 acres of active vineyards and maintaining a production capacity of 5.3 million litres.

Ace investor Porinju Veliyath bought a 1.2% stake in the company worth Rs 7 cr, as per the exchange filings for the quarter ending September 2025.

This fresh pick by Veliyath has raised quite a few eyebrows, as the company’s financials are not very attractive. Take a look.

The company’s sales saw a drop in the last 5 years, from Rs 295 cr in FY20 to Rs 276 cr in FY25.

The EBITDA (earnings before interest, taxes, depreciation, and amortization) which was Rs 1 cr in FY20, saw a turnaround in FY24 when it reached Rs 29 cr. But in FY25, the figure fell to a loss of 6 cr.

As for the net profits, the last 5 years, the company has seen profits only in FY24 (Rs 9 cr) and has seen a string of losses other than that. In FY25, the company logged in losses of Rs 17 cr.

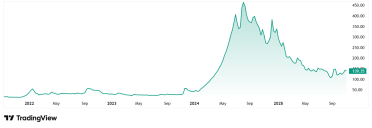

The share price of Fratelli Vineyards Ltd was around Rs 20 in November 2020, which has jumped to its current price of Rs 139 as of closing on 7th November 2025. That is a jump of almost 600% in 5 years. Rs 1 lac invested in the stock 5 years ago would have turned close to Rs 7 lacs today.

At the current price, the share is trading at a discount of about 72% from its all-time high price of Rs 495.

The company’s share is trading at a negative PE due to the string of losses, while the current industry median is 33x. The 10-year median PE for Fratelli is 4x and the industry median for the same period is 20x.

According to the company’s latest investor presentation from August 2025, while in Q1 the company faced temporary headwinds, management remains confident of a 15–20% topline growth in FY26 and margin expansion with the help of cost optimization. The company is entering the wine hospitality space strongly, balancing capital allocation with brand-building initiatives. Structural industry barriers, robust market share, and an expanding product portfolio underscore the management’s optimism despite the near-term challenges.

A stake hike in existing holding

Incorporated in 1998, Apollo Sindoori Hotels Ltd has a current market cap of Rs 332 cr and is in the business of managing food outlets at hospitals and reputed organizations. It also undertakes outdoor catering services, skilled manpower to hospitals, etc.

Porinju Veliyath just hiked his holding in the company from 2.1% to 2.3% making it a holding worth Rs 7.7 cr.

The company’s sales grew at a compounded rate of 23% between FY20 and FY25.

The EBITDA saw a compounded growth of 19% in the same period. As for the net profits, the company has logged a compounded drop of 12% from Rs 15 cr in FY20 to Rs 8 cr in FY25.

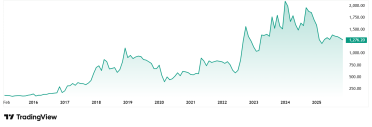

The share price of Apollo Sindoori Hotels Ltd was around Rs 585 in November 2020 and as of closing on 7th November 2025, the price was Rs 1,276. A jump of 118% in 5 years.

At the current price of Rs 1,276, the share is trading at a discount of 52% from its all-time high price of Rs 2,652.

The company’s share is trading at a PE of 33x while the current industry median is 34x. The 10-year median PE for the company is18x and the industry median for the same period is 38x.

Turnaround stories in the making?

The three changes that Porinju Veliyath has made to his portfolio are an interesting story to follow, given that Veliyath is known to pick and drop stocks at the right time, a strategy that has proven profitable.

Well, we will have to wait and see which way these companies scale up. But with Veliyath’s interest, the companies we saw today warrant a keen eye to be kept on them. Add to a watchlist, maybe?

Disclaimer:

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.