")

Suzlon was reeling under massive debt, corporate governance issues, and declining significance in the past. However, it has staged a recovery that few could have predicted.

Once one of India’s most troubled renewable energy firms, the company is now posting healthy profits and eliminating its long-standing debt. It is building a robust order book, drawing investors and industry watchers alike.

In recent quarters, Suzlon has been at the centre of attention for both the right and wrong reasons, a regulatory closure by SEBI, a blockbuster promoter stake sale, and steady orders.

But is this revival here to stay? Let’s understand the fundamentals to know.

Why is Suzlon Making Headlines?

Suzlon has been prominently featured in financial headlines for several reasons.

#1 Performance

The company’s net profit increased from ₹281 crores in Q4FY24 to ₹1,181 crores in Q4FY25. The annual profits increased to ₹2,072 crores from ₹722 crores in the previous year. The stock price grew at a compounded annual rate (CAGR) of 120% in the last three years. The numbers exclude exceptional items.

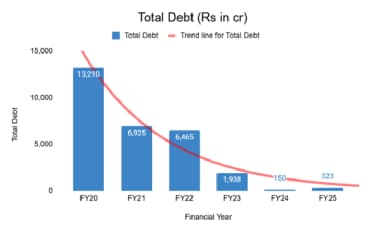

#2 Zero Net Debt

The company announced that it had turned debt-free. It was a change from its debt crisis a decade ago, when it struggled under a debt load of ₹13,210 crore in FY20.

#3 SEBI Case Resolved

SEBI closed its legal proceedings against Suzlon on June 30 this year. This change lifted investor sentiment that had fallen since FY22.

#4 New Wind Energy & Hybrid Orders

Suzlon has secured wind power orders from AMPIN, NTPC Green Energy, and Torrent Power in the last two quarters. It has also secured orders for hybrid (solar and wind) projects. Such orders show renewed confidence of PSUs and private players in Suzlon’s tech expertise.

Suzlon: Drivers of The Financial Turnaround

1. Zero Net Debt

The most remarkable thing about Suzlon’s revival is its journey from an indebted company to a debt-free company. Suzlon owed banks over ₹13,210 crores in FY20.

Through asset sales, aggressive cost control, and operational turnaround, the company was able to pay off its loans.

Suzlon has now eliminated interest-bearing debt. FY25 ended with ₹683 cr. cash versus ₹323 cr. borrowings, making it effectively net debt-free.

Removing interest obligations boosted its bottom line. Minimal debt improved Suzlon’s ability to take on fresh projects without equity dilution.

Suzlon Energy Debt Reduction

2. Profits Return

Suzlon’s FY25 financials show that the company is making money again. The company had a net profit of ₹2,072 crore in FY25, up from a loss of ₹65 crore in FY22, while the operating margin surged to 17% in FY25 from 14% in FY22. The numbers exclude exceptional items.

This profitability wasn’t a single quarter phenomenon. The company had twelve consecutive quarters of positive earnings, signifying a shift in the earnings trajectory.

The key drivers to this change have been timely project execution, low input costs for steel, copper, and operational efficiency. Suzlon’s revenues grew 73% YoY from ₹2,196 crore in Q4FY24 to ₹3,790 crore in Q4FY25, despite market instability.

3. Growing Order Book Increases Confidence

Suzlon’s orders crossed 1.5 GW capacity. They include more orders from NTPC Green, Jindal Steel, and other energy players in India. These orders are greenfield installations and hybrid projects (solar + wind). Such projects are popular among distribution companies (DISCOMs) and independent power producers.

ICICI Direct and Axis Securities believe Suzlon will turn the orders into revenue. Over the next 6–8 quarters, they predict a 20–25% topline CAGR through FY26.

Government-led auctions and the tightening of renewable purchase obligations (RPOs) have helped Suzlon. India plans to install 140 GW of wind energy by 2030, up from ~47 GW currently.

4. Efficient Operations

Suzlon has consciously moved to a business model that is asset-light. After its restructuring in 2020, the company focused on manufacturing turbines, operation and maintenance services (OMS), and EPC execution. It does not plan to own capital-heavy assets.

The S144 wind turbine, with a rotor diameter of 144 meters, is specially made for India’s low-wind regions. It is a key part of its product strategy today. The modular design lowers installation costs and increases power yield by 15–20%.

5. Corporate Governance and Strategic Moves

Suzlon has been criticised for a lack of transparency in its transactions before. The resolution of the SEBI case in June 2025 helped restore market confidence.

The recent ~₹1,300 crore stake sale by the Tanti family is perhaps something investors may question. Only time will tell whether there was anything more to it. For now, the stock price has held up rather well after this large sale.

Investors Must Keep A Check On

Suzlon’s turnaround seems to be supported by strong fundamentals. Yet, investors should keep an eye on a few key metrics and events

1. Execution Risk on New Orders

Suzlon must complete its government-scheme-led wind projects on time to generate revenue. Any interruptions in logistics, land purchase, or policies could affect operating margins.

2. Working Capital Cycle and Receivables

Suzlon faced long payment cycles from its clients, especially state-owned DISCOMs, in the past. You must keep an eye on the changes in debtor days and quarterly cash flows. For instance, debtor days increased from 102 in FY24 to 130 days in Mar 2025. That’s not great. Any further increase could stretch the company’s cash position. On the flip side, an improving number could unlock capital.

3. Sectoral Headwinds

Any supply chain issues globally or price increases in copper, rare earths, and steel could affect turbine costs. The Indian wind sector is still recovering. However, it faces tough competition from solar energy’s cost-efficiency.

4. Promoter Support

Promoters have reduced their stake in Suzlon. Further stake dilution or leadership changes must be monitored.

5. Valuation Premium and Expectations

Suzlon is not a penny stock any longer, with a market cap of ₹88,000+ crore. The market has considered Suzlon’s continued performance. So even minor execution misses could result in stock corrections.

Transient or Transformational?

Suzlon’s recovery is a genuine structural improvement. Debt reduction, consistent profitability, improved governance, and changes in the clean energy sector have been key drivers.

Global and PSU orders signal rising trust in Suzlon’s tech and executional capabilities. Suzlon is a crucial player in the Indian ESG and energy transition.

That said, a few milestones lie ahead. Order execution will be key. Faster receivable recovery, disciplined cost management, and promoter stability will be crucial. These factors will decide if Suzlon will become a stable mid-large-cap entity.

For now, in FY25, Suzlon hasn’t just bounced back; it looks set to sustain and grow. The next 12–18 months will define whether it truly sticks this landing.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Archana Chettiar is a writer with over a decade of experience in storytelling, and, in particular, investor education. In a previous assignment, at Equentis Wealth Advisory, she led innovation and communication initiatives. Here she focused her writing on stocks and other investment avenues that could empower her readers to make potentially better investment decisions.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.