")

With an expanding economy, people’s aspirations and income levels also grow. This growth fuels consumption across categories. Notably, in India, where a majority of the population lives in rural areas, their aspirations often begin with migrating to cities, followed by increased spending on lifestyle products. This shift continues to drive strong demand for retail products.

That’s where value retail has quietly carved its place. These retailers have become the face of organized consumption for millions of first-time shoppers who seek branded quality without paying a premium. And that demand is no longer confined to metros; it’s spreading steadily into tier-II and tier-III cities, where rising incomes and aspirations meet price sensitivity.

Value retailers have aced the art of faster inventory turnover. According to Vishal Mega Mart, the total addressable retail market is expected to grow to about ₹112 trillion by FY28, up from ₹72 trillion in FY23. Value retailers are poised to be big beneficiaries of this shift. Let’s take a look at three such players expected to gain from this shift.

#1 Vishal Mega Mart: The diversified titan

Vishal Mega Mart is a diversified value retailer serving the middle and lower-middle income groups in India. It targets the largest consumer segment, comprising 66% of the households in India. It is one of the top three offline-first diversified retailers in India by retail volume.

Expanding store network with wider reach

As of 30 June 2025, its store count stands at 717. The stores are geographically diversified with 228 in North, East (184), South (178), and West (67). Also, 193 of these stores are located in Tier I cities, 186 in Tier II, and 338 in Tier III, showing its focus on smaller towns. This also ensures a lower concentration risk.

Earnings momentum builds on strong operating leverage

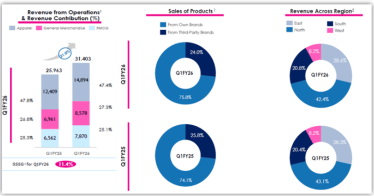

Vishal’s revenue rose 21% to Rs 31.4 billion in Q1FY26, led by an 11.4% increase in same-store sales. The apparel segment contributed 47.4%, followed by general merchandise (27.3%) and FMCG (25.1%).

Vishal’s own brands contributed 75.8% of revenue, while the remainder came from third-party brands. Quick Commerce (QC) continues to expand, with 670 stores in 445 cities. QC contribution to total store revenue is increasing, ranging from 2-3% in new and competitive cities to 6-8% in older and less competitive cities.

What sets Vishal apart is its large and loyal customer base of 151 million. Vishal operates a mobile-based loyalty program where consumers can enroll to earn and redeem points on all transactions. The group contributed 95% to gross revenue (revenue including GST) in Q1FY26.

Vishal Key Performance Indicator

On the margin front, its gross margin expanded by 20 basis points (bps) to 28.4%, while EBITDA margin rose by 50 bps to 14.6%. Net profit rose 37.3% to ₹2.0 billion. EBITDA stands for earnings before interest, tax, depreciation, and amortization.

Store expansion gains pace in new regions

Looking ahead, management expects margins to continue improving due to operating leverage. Under the private label strategy, the apparel business is already 100% private label and is expected to remain at this level. The contribution of private brands in general merchandise and FMCG will continue to improve in the coming years.

That said, the company expects the pace of growth to be lower than historically observed, as the easier and larger opportunities have already been tapped. Vishal is focused on expanding its footprint in existing and new states. In new states, the company’s pilot stores in Pune and Ahmedabad, opened in Q1FY26, have shown encouraging signs.

Therefore, the company is looking for additional properties in these two states. Its new stores typically break even in 18 months, turning profitable immediately. Vishal also aims to accelerate the rollout of smaller-format stores in Uttar Pradesh and Haryana.

#2 V2 Retail: The aggressive fashion expander

V2 Retail primarily operates in the value fashion market, with a primary focus on Tier II and Tier III cities. The company operates a chain of 216 V2 Retail stores across 165+ cities in 21 states, covering about 2.3 million square feet of retail space.

Efficient inventory and strategic store placement

The company currently holds an average inventory for meeting 10-12 days of sales, which it plans to bring down to 3-4 days. Most of these stores (60-70%) are located in high-performing clusters such as Uttar Pradesh, Bihar, Odisha, and Jharkhand. The rest are located in new markets like Maharashtra, Punjab, and Rajasthan.

The company plans to expand nationwide over the next three years. As of July 2025, V2 has 76 stores under discussion and has more than 150 properties shortlisted for potential openings. Store openings typically take 3 to 6 months from shortlisting.

Robust revenue growth and margins

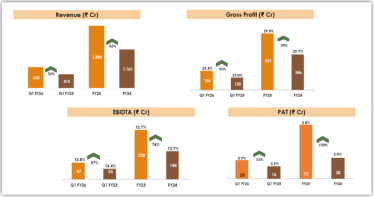

The company’s revenue in Q1FY26 increased 52% year-over-year to ₹6.3 billion, driven by 50% volume growth and 5% same-store sales growth. Its average selling price also increased 16.5% to ₹303, while average bill value increased 9.3% to ₹901.

V2 Retail Financial Performance (Q1FY26)

In the revenue mix, men’s apparel contributed 41% to revenue, followed by women’s apparel (29%), children’s apparel (24%), and lifestyle (6%). Gross margin also increased marginally by 50 bps to 29.5%, while EBITDA margin expanded 40 bps to 13.8%. With strong revenue growth, PAT increased 51% to ₹250 million.

Aggressive Expansion to Capture India’s Value Fashion Market

Looking ahead, the management views the current period as a good time to gain market share and believes V2 is positioned to lead the next wave of growth in India’s value fashion market. The company aims to grow its revenue by 50% annually on a sustainable basis in the future. The long-term goal is to reach a 10% EBITDA margin within the next 2 two years.

This projected revenue growth is expected to be driven by store expansion (contributing 40% by opening 100 stores annually over the next 4-5 years) and same-store sales growth of 8-10% from existing stores. It also aims to achieve average national sales of ₹1,200 per square foot per month over the next three years.

#3 Baazar Style: The eastern India leader

Baazar Style is a leading value fashion retailer based in Kolkata. The company is known for its brands Style Bazaar and Express Bazaar. It sells readymade garments, accessories, and home decor. Like Vishal and V2, it caters to the aspirational middle class and lower-middle class living in Tier 2, Tier 3, and Tier 4 cities.

Expanding footprint across eastern India

As of 30 June 2025, the company operates 232 stores with 2.1 million rentable square feet across 9 states and 182 cities. West Bengal, Odisha, Assam, and Bihar are its core markets, from where it gets about 80.8% of its revenue. The balance comes from other states, including Jharkhand, Andhra Pradesh, Tripura, Uttar Pradesh, and Arunachal Pradesh.

Baazar Style Key Performance Indicator

Steady growth momentum in FY26

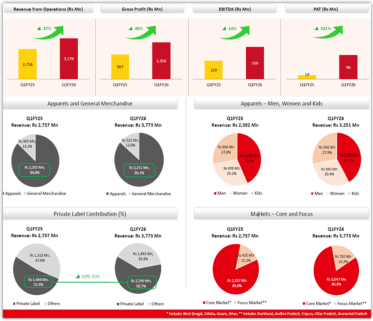

The company’s revenue in Q1FY26 increased by 37% year-on-year to ₹3.7 billion, driven by normalized same-store sales growth of 11%. Normalized here refers to the adjustment made, as the preponement of Eid shifted the benefit to Q4FY25. Apparel contributed 86.2% of revenue, with the remainder coming from general merchandise.

Private label brands are a core component of the business, enabling better margins and product differentiation. The company operates 11 private labels. Private labels contributed 61% to overall revenue in Q1FY26, up from 45% of total revenue in FY25.

EBITDA rose 14% to ₹250 million, but margin declined 134 bps to 6.6%. PAT in Q1FY25 was impacted by an exceptional loss of ₹108 million, which narrowed to ₹8 million this quarter. As a result, Bazaar Style’s PAT increased by a massive 531% to ₹90 million, albeit from a low base of ₹14 million.

In FY26, the company estimates revenue growth of 25%, same-store sales growth of 7-8%, and gross margin expansion of 50 bps.

Scaling up the store network

Looking ahead, the company has a vision of reaching 500 stores in five years. To this end, it plans to add enhanced cluster nodes across Eastern and Northern India, targeting 40–50 stores in FY26 and FY27, respectively. The expansion focuses on achieving market leadership in Eastern India.

Core markets (West Bengal, Odisha, Assam, Bihar) remain key focus areas, while growth is accelerating in focused states like Uttar Pradesh and Jharkhand. Within the store mix, the general strategy is to open approximately 75% to 80% of new stores in Tier 2, Tier 3, and Tier 4 markets, with approximately 20% in metro and Tier 1 locations.

Does the valuation leave room for error?

Value retailers could undoubtedly be the next big bet, as their rise is quietly reshaping India’s consumption story. As rising aspirations meet affordability, these retailers—Vishal Mega Mart, V2 Retail, and Baazar Style—are emerging as key enablers of the next wave of organized consumption. Their strategies may differ, but the playbook is the same: target the underserved, expand into smaller towns, and scale efficiently.

Valuation Comparison (X)

| Company | P/E | Industry |

| Vishal Mega Mart | 101 | 51.4 |

| V2 Retail | 99 | 41.8 |

| Baazar Style | 140 | 41.8 |

However, valuations are high, which leaves little room for any growth slowdown. Vishal is trading at a price-earnings (P/E) multiple of 101x, which is higher than the industry’s 51.4x.

Then, V2 P/E of 99x is also higher than its 10-year median (65.6x) and more than double that of the industry (41.8x). And, Baazar is outpacing both by trading at an astronomical 140x P/E, which is also higher than the industry’s (41.8x). We have not taken Vishal and Baazar median multiple due to limited trading history.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data was not available have we used an alternate but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.