By Tapan Doshi

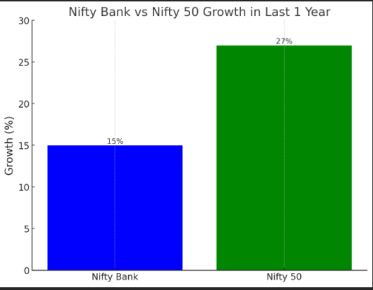

The banking sector is in a good time to shift gears. From last year, Nifty 50 was up by 27% and Nifty Bank has advanced by around 15%. Banks constitute an important 30% of the Nifty 50 index and have pulled the index down. Now that banks are appearing with renewed strength with the easing of challenges and a friendly economic environment, the Nifty 50 is in for an upbeat scenario.

Reduced Borrowing Costs

The reduced borrowing costs should give quite a boost to the banks, directly impacting the credit cost for banks. The U.S. Federal Reserve has already cut the rates by 50 basis points this year and is supposed to cut another two 25 basis points soon before Dec ’24. One would expect the RBI to do the same, perhaps between 25 to 50 basis points, either in early October or November.

Increase in Net Interest Margin (NIM)

Normally, rate cuts have the associated effect of reducing the cost of funds for banks which in turn allows them to lend at decreasing rates but without hurting their profitability at all. Increasing NIM based on these low-cost borrowing will also be based on a firmer foundation for the overall profitability of banks. Now with credit demand expected to rise primarily in the retail and corporate segments, banks shall be in an excellent position to increase their loan books and benefit from market opportunities themselves.

Strong Loan Demand

The bigger banks are also positive and expect higher loan growth for the coming quarters, benefiting from the interest rate cut effect.

- HDFC Bank had guided the steady growth of the loan portfolio, driven by strong demand and improved asset quality. The bank is well poised for growth with a healthy capital adequacy ratio.

- The management expects that growth in retail, as well as corporate loans, will continue to expand profit margins further since borrowed costs decrease.

- Besides, it will greatly benefit from cuts in rates and will be further blessed with high loan demand due to the huge operations.

- Kotak Mahindra Bank is expected to see improved margins and profitability as borrowing costs drop, driven by RBI’s anticipated rate cuts.

- Axis Bank is constructive about the quarters ahead with loan growth and the favourable market backdrop supporting profitability.

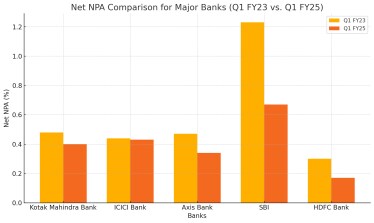

Net NPA at lowest levels

In the last two years, the major banks have recorded the lowest NPAs, which improved the asset quality plus brought down the risk. Improvement in asset quality along with increased profitability on account of rate cuts has made the banking sector a lot more robust going forward.

Overcoming Tight Liquidity

Of course, the biggest issue banks have faced is liquidity. However, strategic play in these areas seems to have fine-tuned balance sheets. Optimising the deposit mix, high-quality liquid assets, and enhancing the big digital platform has improved operational efficiency. The RBI’s additional risk weightage along with the LCR requirement certainly does impose pressure, but interest rate cuts might ease out liquidity constraints.

Online Banking and Operational Efficiency

Operational efficiency with more focused digitization has increased. Increased automation usage, reduction in manual interventions, and rising adoption of digital channels help cut costs and drive efficiency. Strategic cost controls in terms of improvement in the network of branches and overheads are also helping in profitability. Growth in CASA deposits remains moderate, though the induction of digital transformation is helping banks sustain profitability in a highly competitive scenario.

Brighter Future for Banks

The banking sector is very well set for a healthy bounce back. Rate cuts are expected and they will accompany the picking up of loan demand aided by strong NIMs. Investors and stakeholders remain on a growth trajectory, as the cost of profitability increases.

(Disclaimer: Tapan Doshi is a Chartered Accountant, Sebi registered Research Analyst and Founder of Thoughtful Investor Hub. Views, recommendations, and opinions expressed are personal and do not reflect the official position or policy of Financial Express Online. Readers are advised to consult qualified financial advisors before making any investment decisions. Reproducing this content without permission is prohibited.)