")

Picture this. A quiet workshop in Pune where technicians solder circuit boards, test tiny radar gears, or write code for an upcoming satellite’s brain.

No showy showroom, no glossy car wrap, just LED panels, test benches buzzing, and researchers working with microscopes.

Does this place exist? Yes, it’s Data Patterns, one of the fastest-growing defence and aerospace electronics companies.

It doesn’t make military tanks or planes you see flying above. Instead, it manufactures the heart of these, radars, communication systems, and avionics, powering some of the most advanced security, planetary, and aeronautics projects in India.

For years, Data Patterns was known among insiders. But its numbers are making more investors notice.

With growing government spending on defence, a push for self-dependence, and robust execution, this company is striding out of the shadows. But, like all growth stories, it has its twists.

Before the leap

If we want to know more about its recent run, then we need to rewind. Five years ago, Data Patterns was steadily building defensive electronics.

But it struggled with sluggish product authorisations, long development cycles, and interruptions in customer approvals.

Revenue was growing, but viability was modest; export markups squeezed margins, testing overheads continued to increase, while working capital cycles grew long.

The company relied on DRDO and ISRO for most projects, but the work was often one-off, low-scale, and spread across lengthy development cycles. When orders got late or customer sign-offs were slow, factories sat idle; inventories rose.

The material and component costs, especially imported ones, were unpredictable. Its annual revenue in FY18 was only ₹57 crore, with a PAT of ₹1 crore. Margins were thin (16% in FY18), and the order book was tiny and erratic.

Unlike Hindustan Aeronautics Limited or Bharat Electronics Limited, the company didn’t have the brand presence, investor attention, or large contracts.

Its electronics were critical, but its role was invisible. A Tier-II vendor that powered systems behind the scenes. Investors saw possibilities but grumbled that the story was always “nearly there.”

The defence push that changed the game

Everything changed with India’s Make in India Defence and Atmanirbhar Bharat programs. The government preferred native electronics as it wanted to reduce the dependence on radar, avionics, and satellite subsystem imports.

Data Patterns that had always been in the background made a strategic shift. Instead of just building to spec, it focused on design-led solutions, providing everything from research & development, production, to testing and lifecycle support.

It meant fewer middlemen, improved quality control, and faster changes. Although this move meant taking on additional risks, investing in laboratories and skilled engineers to move up the value chain from a small parts supplier to a vital product system integrator.

Building tech from the ground up

Unlike its peers, who depend on foreign machinery, Data Patterns builds almost all crucial subsystems in-house, such as ground-based radar and mobile EW systems, Tejas fighter modules, and UAV control systems.

They also manufacture seeker head electronics, launch controllers, satellite payload boxes, and launch vehicle avionics for ISRO.

This design-first model is the reason its trailing twelve months (TTM) operating margins hover around 38%.

The numbers that tell the story

This quarter (1QFY26) saw the revenue at ₹99 crore, ~ -4.56% dip YoY from ₹104 crore in Q1FY25. More on this decline later on.

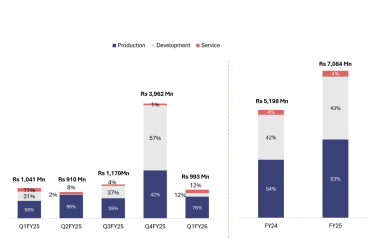

Diversified revenue profile

The Earnings before interest, tax, depreciation, and amortisation (EBITDA) for the same period was ~₹32.3 crore, with an operating margin of 32%.

The net profit for Q1FY26 excluding exceptional items was ₹25.5 crore, a decline of ₹22.23% YoY from ₹32.8 crore in Q1FY25.

The stock price grew at a compounded rate of 33% over the last three years, while the return on equity was an average of 15% for the same period.

Allies in ascent

However, long-term partnerships with DRDO and ISRO have given Data Patterns both authority and income visibility.

DRDO projects like the avionics for Tejas and electronic warfare systems make up a big share of repeat orders. And ISRO’s growing commercial and government launch pace provides tailwinds for its satellite electronics.

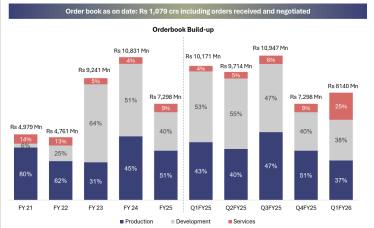

As of the first quarter, the order book was over ₹814 crore, which meant the company would be bringing in revenue for the next few years. These associations have helped Data Patterns scale while keeping margins and reducing the risks from one-off orders.

Annual and Quarterly order book breakup

Drivers Of Growth

Data Patterns is undergoing significant growth and progress in its industry.

Healthy order line-up:

The company already has ₹814 crore in firm orders, with several others being negotiated. This growing number offers visibility into its potential future income.

Future plans

Data Patterns plans to move up the value chain using full systems built with reusable building blocks.

Strategic capex

It has invested over ₹100 crores in new product development and ₹160 crores in capital expenditure over the last five years.

Also, it will invest an additional ₹150 crores in CAPEX over the next two years to develop in-house tech and products to increase its total addressable market, build capacity, and move more into serial production.

Serial production (making several units) gives the benefits of scale, unlike manufacturing custom one-offs.

Defence policy tailwinds

The government’s push for Indian tech, improved defence budgets, and fondness for local supply play well into Data Patterns’ forte. Its previous certificates, permissions, and work make it a preferred partner compared to new entrants in this sector.

Margin controls

Improved product mix (higher-value work), better utilization, fewer delays, and stronger internal testing all help margins.

Roadblocks to watch

No growth is without potholes. Data Patterns has a few barriers that investors must keep an eye on.

Q1 FY26 showed a revenue drop as some customer sanctions or product dispatches were overdue. Orders may be there, but timely execution is crucial.

The company has high days receivable (money owed by customers). As of FY25, it had a trade receivable balance of ₹199 crores. When orders are large and payments are late, the cash flow can get tight.

The stock’s P/E is high (~71.8 per Screener) compared to the industry median of 70.5. It means expectations are baked in. Sudden underperformance or a drop in margins could affect investor confidence.

New subsystems, electronics, or technologies in defence need authorisations, quality control checks, and sanctions, which can be slow. Any interruptions could stall income.

Supply chain issues (imported components), foreign exchange movements, and budgetary limits in government spending can affect distributions and cost-effectiveness.

The investor view

Data Patterns’ IPO in Dec 2021 priced the stock at ₹585. Since then, it has surged past ₹2,752 as of 3rd October 25, showing the market’s appreciation of a design-first, high-margin growth story.

For someone looking to invest, here’s why Data Patterns is catching interest.

It offers a mix of steady and growing revenue (defence electronics + aerospace), with rising profitability. It’s making the most of India’s self-reliant defence manufacturing push.

Its margin profile is improving as they are shifting from one-off customs, low-scale work, to larger repeat orders, which will eventually unlock its operating leverage. Moreover, it has low debt, so financial risk is lower.

The bigger picture

According to the Ministry of Defense (MoD) press release on 1st Feb 2025, India’s defence budget for FY26 is over ₹6.81 lakh crore for capital expenditure.

The major focus will be on modernisation of electronics-heavy projects like UAVs, radars, and missiles, and local procurement. ISRO, meanwhile, has expanded commercial launches, creating spillover demand for subsystem makers.

For Data Patterns, this means it sits right at the juncture of defence electronics self-reliance (cutting imports), space commercialisation (new private contracts), and UAVs and next-gen systems (CATS Warrior, swarm drones)

A story of patterns, not just data

Data Patterns could have stayed a niche firm in the defence electronics world, a name only insiders recognized.

But with timely execution, higher margins, and a clear roadmap, it’s becoming a stronger player among India’s “next wave” of defence-tech companies.

If you’re thinking long term, attracted to companies that benefit from government policy, technical depth, and rising margin strength, Data Patterns may be one of those tales that starts silently but ends up turning heads.

For India’s push toward 500 GW renewables, hypersonic, and deep-space exploration, design-led private companies like Data Patterns are essential.

For investors, the takeaway is clear: this is not a mass-market stock like BEL or HAL, but a specialist play on defence electronics, with both high-growth possibilities and high execution risks.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Archana Chettiar is a writer with over a decade of experience in storytelling, and, in particular, investor education. In a previous assignment, at Equentis Wealth Advisory, she led innovation and communication initiatives. Here she focused her writing on stocks and other investment avenues that could empower her readers to make potentially better investment decisions.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.