By Suhel Khan

As the world’s largest supplier of generic drugs, renowned for its cost-effective vaccines and generic medicines, India plays a very important role in global medicine. The Indian pharmaceutical industry has transformed into a flourishing sector, currently ranking third globally in terms of production volume and 14th in terms of value. Over the past decade, the industry has grown at a compound annual growth rate (CAGR) of 9.43%.

With highest number of pharmaceutical manufacturing facilities approved by the US Food and Drug Administration (USFDA), India is home to around 500 active pharmaceutical ingredient (API) producers, accounting for approximately 8% of the global API market.

India supplies over 50% of the world’s vaccine demand, 40% of the generic drug demand in the United States, and 25% of all medicines in the United Kingdom. The pharmaceutical sector is a significant contributor to India’s economy, representing about 1.72% of the country’s GDP.

A report by EY and FICCI highlights that the Indian pharmaceutical market is projected to reach a valuation of US$ 130B by 2030, reflecting its robust growth trajectory and expanding global influence.

No wonder some of the leading DIIs in India have placed big bets on these 2 pharma giants.

#1 Wockhardt Ltd

Wockhardt is a global pharmaceutical and biotechnology organization engaged in manufacturing finished dosage formulations, injectables, biopharmaceuticals, orals and topicals (creams and ointments).

With a market cap of Rs 26,567 cr, the company is amongst the top 3 Indian generic companies in the UK and the 6th largest generic supplier in the retail and hospital channels in Ireland.

As of the quarter ending September 2024, the company had a DII holding of 5.08% which is now up to 9.82% as per the exchange filings made for the quarter ending December 2024. That’s a big jump within just three months.

3p India Equity Fund 1, HDFC Large and Mid-Cap Fund, Tata Small Cap Fund and ICICI Prudential ELSS Tax Saver Fund have all bought over 1% stake in the company just in the last quarter.

What is surprising is that Wockhardt’s sales have seen a drop from Rs 3,566 cr in FY19 to Rs 2,798 cr in FY24. The company’s December 2024 numbers are not out yet, but until the quarter ending September 2024, the company had recorded sales of Rs 1,439 cr. Perhaps a clue lies in its drug pipeline, which consists of one drug that has the potential to be a blockbuster.

The Profit after tax (PAT) has also slipped to bigger numbers with the company waiting to see a positive year after FY21. In FY19, the company had recorded losses of Rs 217 cr which have grown to Rs 472 cr in FY24.

EBITDA (earnings before interest, taxes, depreciation, and amortization) is an area where the company sees some silver lining. Form a negative Rs 38 cr in FY19, it grew to Rs 91 cr in FY24. The operating profits margin (OPM) also improved form a negative 1% to 3% in the same period.

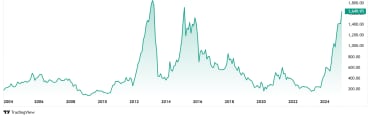

Wockhardt’s current share price is Rs 1,635 (as on 6th February 2025) which is a big 414% jump over its 5-year-old price of around Rs 318.

The stock is trading at a negative P/E and hence the same is not available on screener.com. However, the industry average is currently at 33x.

Wockhardt is restructuring its U.S. business by shutting down its Illinois facility and shifting to contract manufacturing, resulting in US$12 Mn in cost savings. The company also plans to expand into vaccines beyond COVID-19, integrating drug substance and product manufacturing.

#2 Cipla Ltd

Up next we have Cipla Ltd, which is the 3rd largest in the India domestic Rx market, 1st rank in Respiratory medications and amongst the top 5 in Urology and Anti-infectives.

With a market cap of Rs 1,18,703 cr, Cipla has a diversified product portfolio of 1,500+ products in 50+ dosage forms and 65 therapeutic categories.

Cipla too like Wockhardt above has seen a jump in the DII holdings in the last quarter as it went from 23.95% in September 2024 to 27.49% as of the quarter ending December 2024.

As you can see, the investments saw a big jump for the quarter ending December 2024.

Axis ELSS Tax Saver Fund, Kotak Healthcare Fund and UTI ELSS Tax Saver Fund have all bought over 1% stake in the company in the last quarter.

HDFC Manufacturing Fund has also bought a 5.11% stake, but at the same time HDFC Arbitrage Fund has sold its 5.11 stake in the same quarter. So, in all the overall DII holding is not affected by this change.Top of Form

Coming to financials, the company’s sales grew at a compounded rate of 10% from Rs 16,362 cr in FY 19 to Rs 25,774 inFY24.

Net profit also grew from Rs 1,492 cr in FY 19 to Rs 4,154 in FY24, making it a compounded growth of 25%

EBITDA more than doubled from Rs 3,097 cr in FY19 to Rs 6,291 cr in FY24, which is a CAGR of 15%.

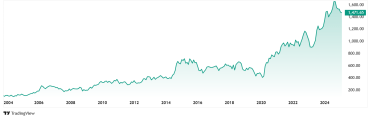

Cipla’s share price is currently trading at Rs 1,470 (as on 6th February closing) which is huge 232% jump over the 5-year-old price which was around Rs 443.

The company’s shares are trading at a PE of 28x, which is a lower than the industry average when compared to peers, which is 33x. The 10-year median PE for Cipla is 31x, while the industry median for the same period is 27x.

Cipla is expecting a growth of ~20% CAGR till 2030 and aims to be the 2nd Largest Pharma company in Rx Market in India. It also aims to be the largest in SAGA (South Africa, Sub-Saharan Africa and Cipla Global Access region) and the 2nd largest in North America.

Bitter Pill to Swallow?

While the financials for Cipla Ltd have shown some solid numbers for DIIs to turn their attention to it, on the other had Wockhardt seems to be on shaky grounds in terms of sales and profits. That’s until you factor in its potential blockbuster drug that’s in the approval process.

According to IBEF (India Brand Equity Foundation), the market size of India pharmaceuticals industry is expected to reach US$ 65B by 2024, ~US$ 130B by 2030 and US$ 450B market by 2047.

It would be a great idea to keep a close eye on these stocks to see how these projections and the DII investments work out in the short and long term.

Disclaimer

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.