Birla Corporation’s cement capacity surged from 9.8 MT to 15.4 post its acquisition of Reliance Cement Corporation (RCCPL). Since then, the company has consolidated the acquired capacity and ramped up production. While the cement industry struggled with volume growth in H1FY20, Birla Corp managed to report 4% volume growth. It ended FY19 at ~90% utilisation with stable Ebitda margins y-o-y compared to ~170 bps contraction in the margins of the I-direct cement coverage universe.

Strong retail presence leads higher share of premium products: Birla Corp has a strong presence on the retail front. Further, it has been pushing more of premium cement via its trade channels and higher ad spends. This has led premium products to form 35-50% of trade sales. In turn, this has seen realisations grow at 6% CAGR over FY16-19, putting it in the ranks of giants UltraTech and ACC. This, combined with 19% volume CAGR, has contributed to revenue CAGR of 26% over FY16-19.

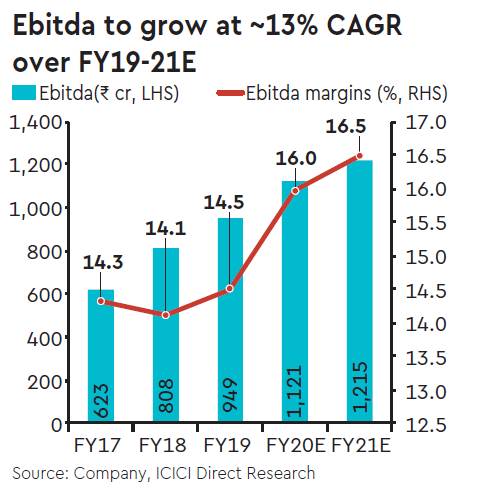

Valuation and outlook: Despite cost pressures, the company has managed to improve its Ebitda margins from 9% in FY16 to 14.5% in FY19, led by increasing sale of premium products. While the company had been saddled with debt owing to the RCCPL acquisition, over FY17-19, debt/equity has improved from 1.3x to 0.9x while debt/Ebitda is expected to improve as well from 5.3x in FY18 to 3.8x by FY21e. Current valuation of 7.5x EV/Ebitda on FY21e numbers make stock well placed for a meaningful upside. We maintain Buy with a TP of Rs 760/share.