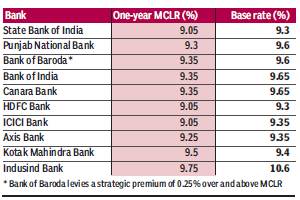

With the 10-bps base rate cut from private sector lender Kotak Mahindra Bank (KMB) coming into effect from Friday, it becomes the only bank at present to have a base rate that is lower than its one-year marginal cost of funds-based lending rate (MCLR).

While its one-year MCLR is currently 9.5%, the base rate is 9.4%. Before the current round of lowering of MCLRs, Bank of Baroda (BoB) also had a base rate that was lower than its effective one-year MCLR, primarily because it levies a 0.25% strategic premium over and above its MCLR for all advances.

KMB’s joint managing director Dipak Gupta said a base rate that is lower than the one-year MCLR is possible since different calculation methodologies are used for the two. “The MCLR is updated every month, but the base rate is not. The decision to cut the base rate effective Friday was mainly a function of the repo rate cut earlier this week. Anyway, our floating loans are linked to the six-month MCLR, which is at 9.2%, and not the one-year MCLR,” he added.

The Reserve Bank of India (RBI) has mandated banks to adopt the MCLR from the beginning of the current financial year because it enables faster transmission. The base rate allowed banks to calculate the cost of funds based on the average cost or marginal cost of funds or any other methodology.

This effectively meant they waited for deposits to be repriced and consequently rate cuts were delayed. While MCLR is also primarily a function of cost of resources, it is based on the marginal cost of money.

Despite the adoption of MCLR and the fact that the RBI has cut the benchmark repo rate by 175 bps since the beginning of CY15, lending rates haven’t kept pace with the drop in borrowing rates.

State Bank of India (SBI), for instance, has lowered the interest it pays on one-year term deposits by 135 bps during this period – from 8.5% to 7.15%. Its base rate, on the other hand, has dropped by just

70 bps during this period – from 10% to 9.3%. Even its one year MCLR is currently only at 9.05%.

Disappointed that banks are not passing on the benefits of lower policy rates to borrowers despite ample liquidity, former RBI governor Raghuram Rajan, at his last monetary policy meeting, had observed that lending rate cuts had only been modest. “Earlier, some bankers said that it was the lack of liquidity that was holding rates high, now I hear from some that it is fear of the FCNR(B) redemptions that is making them reluctant to cut rates. I have a suspicion that some new concern will crop up once the FCNR(B) redemptions are behind us,” Rajan had said.