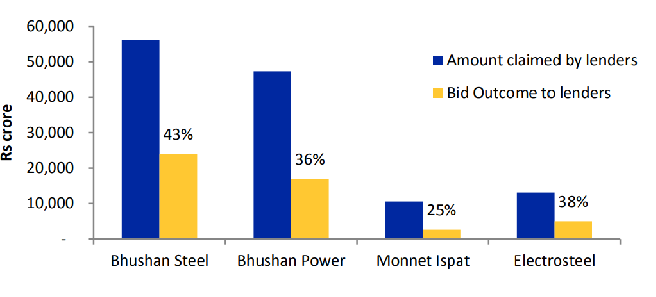

A month ago, India’s newly-adopted Insolvency and Bankruptcy Code (IBC) witnessed the first successful bidding process in which Tata Steel bagged the bankrupt Bhushan Steel, but data show that even in this case what lenders will end up recovering would account for only 43% of total Rs 45,000 crore loan given to the steel company, a research report showed.

Even as the IBC has been conceived with the right intent to seek resolution on distressed assets in a time-bound manner, what data collected by ICRA show that as against amount claimed by lenders, highest bidders have offered between 25% and 43% in case of top four bankrupt steel companies that were identified by the Reserve Bank of India (RBI) under its first list of big defaulters for immediate resolution.

The resolution process of these 12 companies has seen mixed success so far, however, ICRA feels that recovery from stressed accounts in the steel industry between 25% to 43% can be considered “strong bids”. “Acquisition of these debt-ridden companies would provide the stronger entities with operational plants that would immediately accrue to their operating profits compared to the setup of a greenfield project which typically would have a gestation period of 3-4 years,” ICRA said.

ICRA said that the resolution process for entities in some sectors has been disappointing. The two EPC (Engineering, Procurement, Construction) companies on the list, namely Lanco Infratech Limited and Jyoti Structures Limited, have seen limited bidding interest. The shipbuilding industry is another example of a sector plagued with sector-specific issues. Two of the prominent companies from this sector – ABG Shipyard Limited and Bharati Defence and Infrastructure Limited – are currently undergoing the resolution process under the IBC.

“ABG Shipyard Limited was part of the initial 12 companies referred to the NCLT under the RBI’s directive but has received only one bid closer to its liquidation value, which, too, has been rejected by its committee of creditors,” the report said.