Each time there is a big default/fraud, regulators promise action against the promoters, auditors who certified incorrect accounts and even agencies that gave top-notch ratings. Since IL&FS is India’s biggest collapse—the group’s debt is Rs 1.3 lakh crore—Sebi is once again talking of taking action against rating firms and finding other ways to fix the system. Certainly, rating agencies need to be put under the scanner, to ensure ratings are not being bought. Clawing back fees is one option, as is banning some agencies from ratings for some time—RBI has done this to some auditors in the past.

Yet, it is important to keep in mind rating agency failures are part of India’s overall poor standards of governance. If auditors don’t catch siphoning off of funds, one of the big reasons for default, how are rating agencies to catch this? It is, of course, important to find out how credit rating firms that gave IL&FS a good rating for its Rs 75 crore issue, as recently as August, failed to catch the fact that, while the holding company earned Rs 584 crore of profits in FY18, the IL&FS Group’s losses were Rs 1,887 crore; the liabilities of IL&FS at a standalone basis were Rs 17,757 crore while those of the group were Rs 116,447 crore, as a result of which the leverage for the holding company was a reasonable 2.6 but it was over 13 for the group.

But why did the company’s board fail so spectacularly? Rating is not just about hard numbers, it is also about the quality of governance and, to that extent, rating agencies would probably believe the boards of firms—and especially the independent directors on them—are ensuring such standards are met. While IL&FS’s consolidated debt more than doubled between 2014 and 2018, its risk management committee met just once between 2015 and 2018—in July 2015. LIC’s managing director Hemant Bhargava—LIC has a 25.3% equity stake in IL&FS—chaired the committee. Other members included Maruti Suzuki chairman RC Bhargava and former shipping secretary Michael Pinto.

If the audit committee not flagging this is a serious lapse, how did RBI and Sebi’s surveillance system not even get alerted when the audit committee didn’t meet as often as it should have? So while rating agencies have to be penalised for bungling, there has to be an overall improvement in governance standards everywhere; and if that means, as it will, a sharp increase in the staffing budgets for regulators, the government has to provide that immediately.

That said, there are specific steps Sebi and RBI must take to help raters do their job. For one, Sebi has to revive its August 2017 circular that made it mandatory for all listed companies to disclose all defaults in payment of interest and repayment of the principal within one working day. This was to come into effect last year, but pressure from corporates as well as banks resulted in Sebi postponing it. Indeed, this rule needs to be made mandatory for unlisted firms as well. Much of the problem in the IL&FS case, for instance, lay in the unlisted subsidiaries/associates. This is where RBI comes in. In the past, as the CIC notice to the RBI Governor makes clear, the central bank wasn’t keen on making defaults data public. If the entire ratings model is about predicting default, how can raters fine tune their model if they don’t know that a default has taken place, much less the actual date of the event?

And while examing rating agencies, Sebi needs to move beyond the standard data most agencies give on the actual 5-10 year defaults by the firms they rate. The fact that, say, no AAA-rated firm has defaulted over 5-10 years is a great thing, but how much of this is due to the fact that, just before the default, the company was rapidly downgraded to B or C by the rating firm? In other words, Sebi needs to look at the rating firms’ sharp changes in ratings as well.

No rating holds in perpetuity since business conditions change, and the business environment can suddenly deteriorate as well—raters can’t be blamed for the sharp downturn in a Tata Power’s fortunes after Indonesia suddenly hiked the price of coal exports; exports Tata used to power its Gujarat plant. But, a standard disclosure could include giving the names of rated firms that have defaulted and what they were rated 6-12 months before the default.

Moving to models like getting Sebi to pay for all ratings instead of the firms themselves—or perhaps even letting investors like UTI pay for them—sounds good since it seems to take away the conflict of interest inherent in a company paying for its own rating. But the problem with a Sebi paying for a rating is that the emphasis will no longer be on which rating agency is better; all the rating agencies will qualify, and then whoever quotes a lower fee will win the rating contract. Getting a UTI or a Franklin Templeton to pay means the rating will remain with just a few players instead of being disseminated to everyone as happens today.

The government must mandate that every firm has to put out some data on the group’s financials—consolidated sales, profit, leverage, default status—since the parent company’s financials will affect ratings of even step-down subsidiaries. Also, the number of layers of subsidiarisation needs to be relooked; IL&FS found it easy to hide the truth since its 347 entities were held via four levels of step-down subsidiaries; there were 142 entities at Level 4!

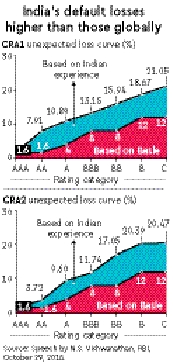

To avoid another IL&FS, these changes are needed ASAP. Even the government-RBI fight is related to this since, as RBI deputy governor NS Vishwanathan points out, one reason for its seemingly higher capital-adequacy norms—this is a bugbear for the government—is the higher losses due to default in India as compared to those used in the Basel norms (see graphic).