There is no doubt that India is strongly leading the global solar energy race. India recently surpassed Japan to become the world’s third-largest solar power producer, a feat to be proud of. Fuelling this surge are popular government policies like the National Solar Mission and the “PM-Surya Ghar” rooftop solar scheme.

India is shining when it comes to targets and is already achieving 50% of its installed electricity capacity from non-fossil sources years ahead of schedule, all while fostering a rock-solid domestic manufacturing ecosystem. India hosts some of the world’s biggest solar parks and co-leads the International Solar Alliance.

At such a time, 2 less known underdog solar companies are quietly turning the tide around for themselves. Let’s find out more about these companies. \

The Profit Champion – ACME Solar Holdings Ltd

Incorporated in 2015, ACME Solar Holdings is a renewable energy company in India with a portfolio of solar, wind, hybrid, and firm and dispatchable renewable energy (“FDRE”) projects

With a market cap of Rs 17,091 cr, the company is one of India’s largest renewable energy-independent power producers (“IPP”) and among India’s top 10 renewable energy players in terms of operational capacity.

The company has a current ROCE (Return on Capital Employed) of 8% which is same as the industry median. This simply means for every Rs 100 the company invests as capital expenditure; it makes a profit of Rs 8 on it.

Let us look at the other financials now, which is interesting because the yearly numbers and the recent quarterly numbers paint a completely different picture.

The company’s sales were at Rs 1,777 cr for FY20 and in FY25 it fell to Rs 1,405. However, on a YoY basis, it grew from Rs 310 cr in June’24 to Rs 511 cr in Jun’25, which is a jump of 65%.

The EBITDA (earnings before interest, taxes, depreciation, and amortization) for ACME fell from Rs 1,625 cr in FY20 to Rs 1,235 in FY25. On a YoY basis, it grew from Rs 272 cr in Jun’24 to Rs 458 cr in Jun’25, logging a growth of 68%.

The net profits climbed form Rs 86 cr in FY20 to Rs 251 cr in FY25, logging in a compound growth of 26%. However, when we look at the YoY figures, it shows nothing short of a turnaround.

| Quarter/FY | Jun-23 | Sep-23 | Dec-23 | Mar-24 | Jun-24 | Sep-24 | Dec-24 | Mar-25 | Jun-25 |

| Profits/Cr | 82 | 39 | 44 | 532 | 1 | 15 | 112 | 122 | 131 |

After a good quarter ending Mar’24, the profits dropped to just Rs 1 cr in Jun’24. However, from then the company recorded a solid upward trajectory. On a YoY basis, purely as a result of the base effect, the profits jumped by a huge 93x between Jun’24 and Jun’25, driven by driven additions and improved capacity utilization.

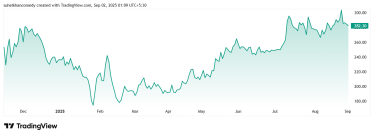

The share price of ACME Solar Holdings Ltd at listing in November 2024 was around Rs 253, and as of closing on 1st September 2025 the price was Rs 282, which is a jump of 12%. In the same period, the share price saw an all-time high of Rs 310 and low of Rs 168.

The company’s share is trading at a current PE of 42x, which is higher than the industry median of 30x.

ACME is scaling renewable and storage capacities, backed by a clear strategy to de-risk execution via early connectivity and prudent capex/debt management. The company also maintains a strong focus on technology, reliability, and long-term O&M partnerships, while the management proactively looks to capture in merchant market upsides, leveraging early commissioning of BESS (battery energy storage systems).

Leading Solar PV Module Manufacturing – Alpex Solar Ltd

Incorporated in 2008, Alpex Solar Ltd (ASL) manufactures photovoltaic modules and provides all-inclusive solar energy solutions.

With a market cap of Rs 2,980 cr, the company is among North India’s largest PV Module Manufacturers. Company manufactures solar PV modules, solar power plants, aluminium frames, IPP, GH2, and AC/DC water pumps. It also undertakes EPC projects. Moreover, ASL trades in circular knitting needles, yarn, air purifiers, water pumps and solar panel. It has installed 15,000+ solar pump installation till date.

The company boasts of a strong ROCE of 52% while the industry median is 19%. Which means that for every Rs 100 the company spends as capital expenditure, it makes a profit off Rs 52 on it, while the rest of the industry averages just Rs 19.

The company’s sales have jumped from Rs 98 cr in FY20 to Rs 780 cr in FY25, which is a compound growth of an enviable 51% in 5 years.

EBITDA has seen a jump from Rs 7 cr in FY20 to Rs 125 cr in FY25, logging in a compounded growth of a huge 78%.

The net profits also have consistently grown at a compounded rate of 94% from Rs 3 cr in FY20 to Rs 83 cr in FY25.

For the quarter ending Jun’24 (last year), the company recorded a profit of just Rs 1 cr, which was a decline from the previous quarter figure of 6 cr.

However, for the quarter ending Jun’25, the company recorded profits of Rs 42 cr. As a result of a base effect, the YoY profit growth shit up to 41x. Other than the base effect, growth was driven by robust module sales and improved pricing. The improved sales volume, combined with higher selling prices (realisations), greatly boosted income and margin.

The share price of Alpex Solar Ltd was around Rs 362 on listing in February 2024, and as of closing on 1st September 2025, it was Rs 1,218. That is a jump of 237% in less than 2 years.

Rs 1 lac invested in the stock at listing would have been around Rs 3.36 lac today.

The share is trading at a PE of 24x which is considerably lower than the current industry median of 39x.

Alpex is successfully executing large-scale, multi-layered expansion with strong order book visibility, solid margin outlook post-integration, and clear alignment with all government policy. The company’s management is positive thanks to strong financials, sturdy capital structure, and deep industry experience. The company is positioning itself as a leading integrated solar manufacturing platform in India, that has a confident but also cautious approach towards future growth and profitability.

Time to Light Up Your Portfolio?

As India steams forward in the race for becoming a global green energy leader, backed by government initiatives and innovation, the industry seems like hot property to many investors. The two companies we saw today are strong players from the Solar industry.

While ACME Solar Holdings turnaround with over 93x jump in YoY profits is definitely an attention grabber, Alpex Solar Ltd’s 40x YoY profit growth clubbed with industry high ROCE of 52% makes it a strong contender in the race as well. Now, we know that this is a result of the base effect, but even if you ignore that for a moment, the companies have delivered strong 5 yr growth numbers.

The risks also have to be considered here in the case of the solar sector of India. Since the sector is heavily influenced by government policies, even a small change in these policies, subsidies, or tax incentives could significantly impact the profitability and growth prospects of solar companies. Plus the government is pushing for domestic manufacturing, which will fuel competition within the sector. This could lead to price wars and put pressure on the profit margins of companies.

Will these 2 solar stocks light up their financials, along with the portfolios of its investors? It is something time will tell. But for now, it would be wise to add these stocks to a watchlist and keep a track on them.

Disclaimer

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.