We hosted Atul Daga, ED & CFO at UltraTech Cement (UTCEM), at our recent 17th Asia Annual Investor Conference 2019. Key takeaways include: (a) demand is expected to grow at 7-8% CAGR over next few years and with improving utilisation, prices are likely to improve; (b) UltraTech Nathdwara (UNCL, erstwhile Binani Cement) utilisation has been increased to 60% with Ebitda/te of >`600/te in Jan’19; targeting low-teen RoCE in next 3-4 years; (c) cement assets of Century Textiles (CENT) operating at average capacity utilisation of 75% with Ebitda/te of `500/te during 9MFY19; potential to improve profitability by `300-400/te through re-branding and cost rationalisations; (d) higher focus on improving overall cost efficiencies. Consolidated net debt is likely to peak-out at `220 bn in FY20e and reduce to `181 bn by FY21e. We maintain our FY19e-FY21e estimates with target price unchanged at `4,350/share based on 14x Dec’20 EV/E. Maintain Buy. UTCEM remains one of our preferred picks besides SRCM.

Management expects demand to grow at 7-8% over next few years led by higher government infrastructure and housing spends. UTCEM estimates industry demand growth of >11% in 9MFY19 and 8-10% y-o-y in Q4FY19 and expects 7-8% growth for FY20-21e. As capacity additions are unlikely to exceed 4-5% CAGR over next few years, prices are likely to improve with increasing utilisation.

Profitability at UNCL improving: Capacity utilisation at UNCL has been increased to 60% with Ebitda/te of >`600/te in Jan’19, mainly led by re-branding. Management sees potential to improve cost structure by `200/te with logistics advantage, use of pet coke and other cost efficiencies. UAE assets of 2mnte grinding unit are operating at almost full utilisation; while company intends to monetise assets in China. Factoring in potential brownfield expansion opportunity of 5mnte at UNCL at a capex of `17-18 bn, management targets low-teen RoCE over next 3-4 years.

Acquisition of 14.6-mnte cements assets of CENT likely to be consummated by Q1FY20: Management sees potential to improve Ebitda/te of the said assets by `300-400/te largely through re-branding (existing price gap of `10-15/bag with UTCEM brand) and other cost efficiencies.

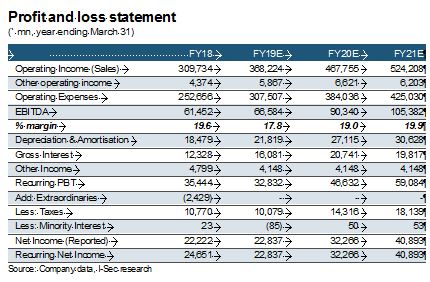

Increased focus on improving overall cost efficiencies via (i) improving blending ratio; (ii) setting up 36MW of WHRS sufficient for 15% of power requirements (vs 7% currently); (iii) increasing use of alternative fuels from current 3%; (iv) reduction in lead distance; and (v) higher operating leverage. Besides, fall in various input prices from their recent peak may provide cost savings of `60-70/te from Q4FY19. We expect UTCEM to post 20% Ebitda and EPS CAGR over FY18-FY21e led by 18% volume CAGR and factoring in consolidated Ebitda/te of `1,007/te by FY21e from `819/te in 9MFY19.