By Chirayu Sharma and Dr. Badri Narayanan Gopalakrishnan

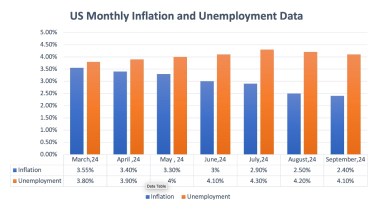

In the inflation data for September 2024, the overall inflation rate stood at 2.4%, showing a slight decrease from 2.5% in August. For July 2024, the Consumer Price Index for All Urban Consumers (CPI-U) increased by 0.2% on a month-over-month (MoM) basis, aligning with expectations, after a 0.1% decline in June. On a year-over-year (YoY) basis, the CPI dropped to 2.9% in July from 3% in June, representing the smallest annual increase since March 2021, despite high price levels.

The Federal Reserve’s objective of getting inflation down to its 2% target is in line with this decrease in headline inflation, which shows that price pressures are lessening. Although there was a little increase in U.S. consumer prices in July, the possibility of the Federal Reserve lowering interest rates at its meeting in the next meeting is increased by the annual inflation rate slowing down to below 3% for the first time in almost three and a half years. These changes should increase the Fed’s confidence that inflation is gradually returning to its objective, paving the way for possible monetary policy easing in the near future—likely at the Federal Open Market Committee’s next meeting.

Unemployment has been steadily rising since March 2024, with only a slight decrease in the most recent jobless data following a recent rate cut. However, if we look at the trend up to September, unemployment consistently increased, suggesting that there is still room for additional rate cuts. This supports the growing anticipation of a potential rate reduction by the Federal Reserve. Historically, unemployment and inflation have shown an inverse relationship: as unemployment rises, consumer spending and wage pressures tend to decrease.

When combined with July/September’s less-than-expected unemployment, the recent decline in inflation points to the economy entering a phase when inflationary pressures are easing and the labour market is loosening. The US economy is heading towards a more balanced state, as seen by the convergence of growing unemployment and weaker inflation. This might lead the Federal Reserve to contemplate loosening monetary policy in the near future.

Also read: US CPI data released, inflation rate picks up

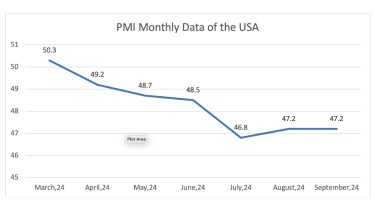

Since March 2024, the U.S. Purchasing Managers’ Index (PMI) has been continuously decreasing, although in recent months it has slightly increased because of the rate cut still it is falling short of the critical 50-point level. A PMI rating below 50 is noteworthy because it denotes a slowdown in output and manufacturing, which is indicative of an economy in decline. There are concerns over the overall state of the economy due to this extended period of declining PMI data, which indicates that economic activity is slowing down.

The sustained drop in PMI not only reflects shrinking industrial output but also serves as a potential warning sign of an impending recession. Extended periods of lower output are associated with fewer corporate investments, lower employment rates, and lower consumer spending, all of which are factors in economic downturns. As a result, the continuous fall in the PMI highlights the problems the US economy is facing and might portend far worse economic times ahead. There is still room for a rate cut to stimulate the economy.

Gold has increased by nearly 15% in the last three months since the start of 2024, making it the best-performing asset class this year as on April 2024. Silver has also done well, rising more than 13% since January 1. The expectation of further rate reduction by investors is a major factor driving the increase in gold prices. Due to a number of beneficial developments, including the possibility of monetary easing by major central banks and the continuation of rising inflation, analysts forecast that both gold and silver will continue to rise.

On May 1, 2024, the yield on 10-year U.S. Treasury securities was 4.964%. By August 16, 2024, it had dropped to 3.913%, fuelling concerns about a possible near-term recession as the decline in long-term bond yields reflects growing uncertainty in the economy. This trend also signalled the potential need for further rate cuts to encourage economic growth. So, we have also seen the rate cut in September after that, the yield curve began to rise again, reaching 4.28% as of October 29.

If the U.S. Federal Reserve decreases interest rates, it might potentially entice more international investors to Indian markets. India can become a more attractive investment destination if the spread in interest rates between the U.S. and India increases. The inflow of foreign money is anticipated to augment the performance of the Indian market and augment the nation’s foreign currency reserves.

The value of the Indian rupee may appreciate in response to an inflow of US dollars. More than 80% of India’s imports are oil, making up a sizeable share of its overall imports. The cost of importing oil can be decreased by an appreciation of the rupee, which will assist in lowering the fiscal deficit. Lower fuel prices often contribute to the management of inflation by lowering the cost of other imported products and services, transportation costs, and the production costs of the businesses that utilise crude oil, and gasoline as a raw resource.

Cheaper imports can help businesses that depend on imported subsidiary items or raw materials since they enhance their entire performance and cost structure. A stronger rupee will reduce the cost of servicing India’s foreign debt, which in turn improves the country’s debt-to-GDP ratio. Decreased interest rates in the United States make dollars more accessible, which encourages investment in Indian markets. Indian businesses now have greater liquidity thanks to this foreign capital inflow, allowing them to increase their investments and boost overall commercial activity. Lower rates also make loans for education and international trips more accessible.

(Chirayu Sharma is a Research Associate with Infinite Sum Modelling LLC, and Dr Badri Narayanan Gopalakrishnan is Fellow, NITI Aayog. Views are personal.)