Pulak Ghosh

The discourse over a jobs debate has never been so shrill. The economy is currently expanding at 6.6% (with a downside bias), but still more than other competing economies, and it is only a matter of sheer conjecture whether it is translating into enough jobs or not? The latest leak of the NSSO data has only added to the confusion as it estimates a 10% drop in employment. With the economy growing at 7.5% for the last five years, such a sharp envisaged drop in employment implies close to 20% rise in labour productivity. Thus, it is imperative that we estimate labour productivity to understand the real story on jobs.

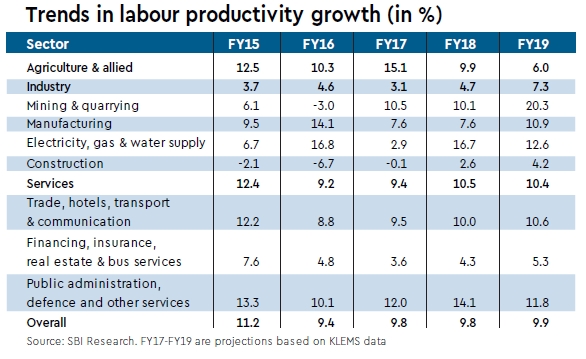

Using the KLEMS data, we estimated productivity of various sectors during FY17-19. Our results show the overall productivity growth remains relatively stagnant (9.4% to 9.9%) in the last five years, barring FY15. Let us take up each of the sectors one by one.

Growth in agriculture productivity has been following a downward trend, which is a cause for concern. It thus appears that the agricultural sector has been witnessing growth in output while at the same time people are leaving agriculture as a source of profession, thereby leading to rise in productivity, but only at the margin. The limited rise in agricultural productivity has also an interesting connotation. Contrary to popular perception, the decline in across-the-board food prices thus cannot be solely attributed to the rise in agricultural productivity. Vegetables, fruits, pulses, eggs and sugar are, in fact, witnessing deflation in the recent months, and it seems that the decline in food prices reflects structural break in food prices over a longer term. This could be the result of prudent supply management or even a change in the behavioural habit of people.

Also read| Rahul Gandhi’s NYAY: Raghuram Rajan tells why it’s not easy to implement minimum income scheme for poor

What is more intriguing is that the growth in manufacturing productivity has slowed down in the recent past. However, what is more interesting is that the productivity gains in India were more significant prior to 2008, reflecting in part the exponential growth in global trade. In effect, trade redistributes the allocation of resources and thereby affects the distributive share of labour, specifically when the markets are imperfect. Using the disaggregated data of Indian industries from 1998 to 2008, an ADB study has found that labour bargaining power drops with the interaction of trade. Labour share, measured as a percentage of gross value addition (GVA), drastically dropped from 28% in 1980 to 10% in 2007-08 in the industrial sector. The drop itself seems to represent the weakening bargaining position of workers and thus productivity gains were significant. Therefore, a drop in bargaining power along with a rise in mark-up of industries explains the gradual decline in labour share, which, in turn, explains a rise in productivity, prior to 2008. Interestingly, post-2008, with slowdown in global trade, labour productivity growth has declined as per our estimation.

We believe that the recent slowdown in manufacturing productivity growth finds ramification in the series of aggressive stock buybacks by Indian corporates, which allows them to boost their earnings without having to invest in productivity gains. This is more possible as corporates have been undergoing deleveraging in the last couple of years, and therefore finding innovative ways to boost earnings. During 2018 and 2019 (till now), Indian companies have bought back 1,952 lakh shares.

The services sector has registered good productivity gains, reflected by its over-7% growth registered in all three quarters of FY19. The services sector has registered a productivity growth of 10.5% in FY18 and is expected to log in a growth of 10.4% in FY19. However, there are worrying signs, too. Within the services sector, real estate, dwelling and professional services—which form the bulk of services—have shown a declining trend in GVA. This is disturbing as the IT services, which are our primary exports, are included in this.

The slow growth in productivity clearly manifests in low wage growth. Our estimates show that wage growth has also been witnessing signs of moderation, on yearly as well as sequential basis. This moderation in wages also implies important lessons that can be deciphered from policy setting. For example, if wage growth is slow, it implies that familiar wage-price nexus is not working and this could result in moderation of inflation expectations. Thus, it is a futile debate to argue regarding jobless growth. We would rather say that in the absence of commensurate productivity and wage gains, we must strive to improve the quality of jobs offered. The current debate should clearly focus on wage growth as a binding constraint.

We would also, however, caution the policymakers of a slower productivity growth. For example, persistent low productivity encourages over-borrowing by corporations and households; in turn, it represents a big risk to economies and fiscal systems. A similar logic applies to the social and political impact of low productivity growth.

Before we end, a word about payroll data. Beginning September 2017, India has been publishing non-farm payroll data every month from EPFO, ESIC and NPS establishments. This is a remarkable upgrade over survey-based quarterly results in terms of data quality and frequency. Although the data from these establishments is still evolving (frequent data revisions), but a similar exercise for other countries shows that it will take time to stabilise. The good thing is that EPFO seems to have now realised that such data revisions could be the result of non-uniform treatment of persons joining and exiting EPFO. Thus, as per EPFO, persons leaving the age band till date included the members who also joined prior to September 2017, but exited only during the period after September 2017. This was strange, as we were using flow data for joining, but stock data for leaving, and hence such drastic revisions. But January figures now look stable after incorporating such changes.

We recommend that EPFO now starts releasing the non-farm productivity (as in the US) at least for those sectors for which we have output data from CSO’s GVA database. This will fill a huge lacuna in productivity estimates in India.

Authors are Group Chief Economic Advisor, State Bank of India, and Professor, IIMB, respectively. Views are personal