Two Exits, One Entrance: The Kedia Playbook

When a promoter starts selling, the usual reaction in the market is to worry. But not for ace investor Vijay Kedia, who has recently been doing the opposite. One of India’s best-known small-cap savant has walked through two such exit doors as per recent filings, buying shares in open-market bulk deals from promoters who were heading out. The two names could hardly be more different. One is a red-hot logistics debutant. The other is a fifty-year-old mining equipment maker the market has left for dead.

Kedia needs little introduction here. Over three decades he turned a modest sum into a portfolio worth thousands of crores, with early bets on names like Atul Auto, Cera Sanitaryware and Tejas Networks. His style is hard to copy: he buys small, out-of-favour businesses, holds them for years, and lets time do the heavy lifting. So, when he shows up in the list of shareholders, people pay attention.

Let us dig into the 2 stocks to see if we can find a pattern that reveals Kedia’s gameplan. Difficult, but no harm trying.

The E-Way Bill to Riches: iWare Supplychain Services

Incorporated in 2018, iWare Supplychain Services is a pan-India logistics company based in Gujarat. It runs five lines of business: warehousing that includes third-party logistics and carrying-and-forwarding work, transportation, rail rake handling, business auxiliary services and rental income.

With a current market cap of just Rs 511 cr, its warehousing footprint runs to more than 8 lakh square feet spread across seven states, from Gujarat and Rajasthan to West Bengal and Delhi.

However, the stock is a recent listing from May 2026, that too on NSE’s SME Platform. And as usual, SME listings come with the warning of “Buyer Beware”. The restriction of trading in lots, liquidity issues etc make it difficult to get in or get out of the stock in tough times. Not to forget the more lenient reporting structures for SME listed companies.

Promoter Supply Meets Kedia’s Demand

As per the June 2026 exchange filings, Kedia came in through a preferential allotment, taking up 3% stake in the company which is about 345,600 shares. And a couple of days later, he went back for more this time through Kedia Securities. He bought another 345,600 shares and that made his total stake 6%. Which means Kedia is now committed to a business most investors had never heard of a year ago.

The interesting part is that Kedia’s buy in came around the same time the promoter holding fell from 74% to 69%, as a promoter entity called Inter India Roadways was selling. So, the fresh demand from Kedia was, in effect, being met by supply from the promoter group. That is a detail worth keeping in view.

Growth at What Cost? Unpacking iWare’s Cash Burn

The financials explain both the excitement and the caution. iWare has grown at an impressive pace, but off a very small base.

| Financial Year | FY21 | FY22 | FY23 | FY24 | FY25 | FY26 | 5Y CAGR |

| Sales (Rs cr) | 19 | 24 | 44 | 59 | 86 | 258 | 68% |

| EBITDA (Rs cr) | 2 | 3 | 6 | 11 | 17 | 29 | 71% |

| Net Profit (Rs cr) | 1 | 1 | 0 | 4 | 8 | 15 | 72% |

The growth rates look sensational, but iWare was earning only about Rs 1 cr in profit five years ago, so almost any progress shows up as a huge percentage. Off a base this small, the compounded number is closer to noise than signal. The real eye-catcher is FY26, when revenue jumped nearly three times, from about Rs 86 cr to Rs 258 cr in a single year. Net profit for the year came in near Rs 15 cr, almost doubling from the previous year’s Rs 8cr.

But growth this fast leaves marks. Operating margin fell from about 20% in FY25 to roughly 11% in FY26. More telling, the company reported negative cash from operations of about Rs 20 cr in FY26, even as reported profit rose. Borrowings climbed to around Rs 70 cr, and debtor days stretched from 66 to 85. For a young company scaling this quickly, that gap is the single most important thing to track.

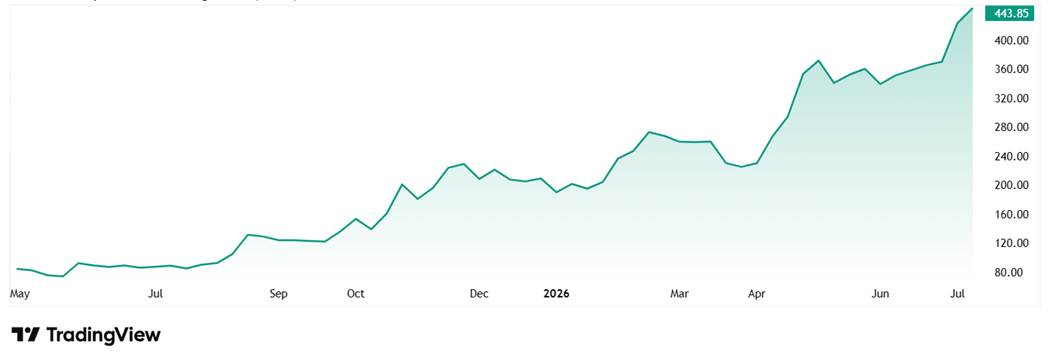

A 450% Surge vs. SME Liquidity Risks

The share price of iWare was around Rs 80 when listed in May 2026 and as on 13th July 2026 it was Rs 444 which is a jump of over 450% in just 2 months.

On valuation, iWare trades at a PE of 34x and close to 9 times its book value. The current industry median PE is 23x. Those are rich numbers for a logistics business, but there is no long history to lean on. As an SME stock listed only in May 2026, iWare has no ten-year median PE to compare against, and even a five-year average would mislead given how young it is.

Return ratios look strong, with ROE near 42% and ROCE around 28%, but on a small, fast-moving base. A board meeting on 15 July 2026 is due to review the first quarter of FY27. That print will tell investors whether the FY26 surge was a one-off or the start of a new run rate.

The Debt-Free Mining Veteran: Eimco Elecon

Incorporated in 1974 and listed in 1992, Eimco Elecon (India) makes equipment for underground and opencast mines. Think side dump loaders, load haul dumpers and rocker shovel loaders, the heavy machines that dig and move rock.

With a market cap of Rs 1,028 cr, the company works out of Vallabh Vidyanagar in Gujarat and traces its roots to a joint venture between Elecon Engineering and an American mining group. For decades it has been a quiet, profitable, unglamorous business.

One interesting bit that catches the eye is the balance sheet. Eimco is almost debt free, carries a book value of around Rs 810 per share, and holds an investment book of roughly Rs 205 cr. A large chunk of its yearly profit comes from that pile of investments rather than from selling machines.

The Foreign Promoter Exit and the Rs 205-Crore Cash Pile

Kedia’s entry here as well is tied directly to a promoter leaving. In late September 2025, a foreign promoter entity, Tamrock Great Britain Holdings, sold its entire 24.68% stake through an offer for sale on the exchanges. That single event pushed promoter holding down from 73.64% to 48.96%. It also, for the first time in years, put a large block of Eimco shares into public hands.

As per the exchange filings for June 2026, Kedia stepped in with a 1.45% stake which is currently worth Rs 15 cr.

The five-year record shows a business that recovered strongly and then stumbled. Here are the standalone numbers

| Financial Year | FY21 | FY22 | FY23 | FY24 | FY25 | FY26 | 5Y CAGR |

| Sales (Rs cr) | 126 | 84 | 173 | 228 | 246 | 231 | 13% |

| EBITDA (Rs cr) | 11 | 9 | 24 | 40 | 56 | 43 | 31% |

| Net Profit (Rs cr) | 11 | 9 | 21 | 40 | 49 | 39 | 29% |

Two things stand out. First, the recovery from FY21 to FY25 was real, with sales almost doubling and profit rising several times over. Second, FY26 went the wrong way. Revenue slipped to Rs 231 cr and net profit fell to about Rs 39 cr, down from the FY25 peak of Rs 49 cr.

Because FY21 was a weak, pandemic-hit base, the five-year compounded figures flatter the trend. On a strict five-year view, the profit growth works out to roughly 29%, but the recent direction is clearly down, not up.

There are structural issues too. Return on equity has hovered near 8%, modest for a cash-rich company. Working capital is heavy, with inventory and receivables tying up money for long stretches. And with Tamrock gone, Eimco no longer has a strong technology-linked foreign promoter, though the remaining promoter group still holds close to 49%.

The bull case is simple: a cash-rich, debt-free maker of mining gear, bought cheap during an earnings dip, can re-rate as mining capex picks up. The bear case is just as simple: it stays a low-return value trap.

Is Cheapness Enough? Weighing the Value Trap Risk

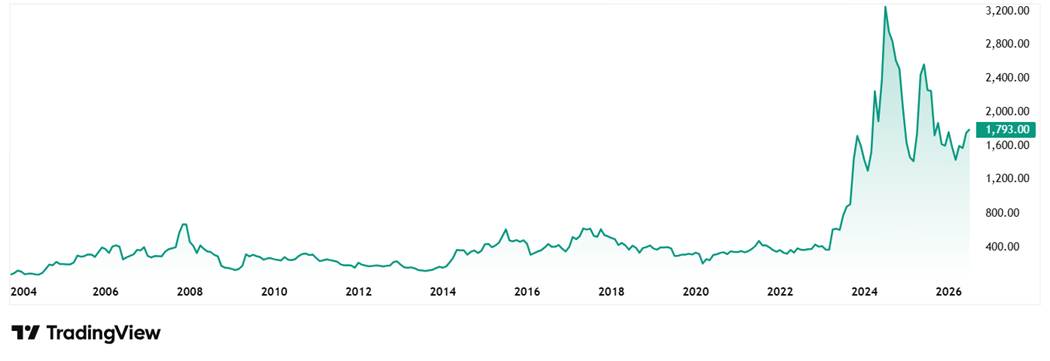

The share price of Eimco Elecon was around Rs 500 in July 2021 and as on 13th July 2026 it was Rs 1,805, which is a jump of over 260% in 5 years.

However, the stock has been through a tough time in the last year as prices fell from over Rs 2,500 in July 2025 to its current price of Rs 1,805. At this price, the stock is trading at a discount of 48% to its all-time high of Rs 3,499.

Regarding valuation, the share of the company is trading at 26x and the industry median is currently 33x. The 10-year median PE for the company is 17x while the industry median for the same period is 27x. Now that is not cheap for a company whose earnings just fell and whose ROE is in single digits.

Adjusted for its large investment holdings, you are paying a full price for the operating business and getting a big cash pile alongside. Whether that cash ever gets put to work, rather than sitting idle, is the question that will decide any re-rating.

Momentum vs. Value – Which Way to Go?

Look at these two buys together and a possible pattern shows up. In both cases Kedia bought from a promoter who was selling. In both cases he chose niche, under-researched industrial and logistics names rather than crowded market favourites. And in both cases the exchange bulk deal data, not a company press release, is what told the story first.

But the two stocks ask retail investors to believe very different things. iWare is a momentum pick, where the worry is that the price has already run hard and the cash flows still need to catch up with the reported profits. Eimco is the opposite, a sleepy value stock where the worry is that cheapness alone does not create returns.

For investors, the sensible takeaway is not to blindly copy a big investor. It is to understand why he bought, and to watch the same signals he watches. For iWare, that means the cash flow and the 15 July results. For Eimco, it means order inflows and whether that idle cash finally goes to work. Add both to a watchlist and keep a vigilant eye on them.

Disclaimer:

Note: We have relied on data from http://www.Screener.in and http://www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, he was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article. The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein.