Porinju Veliyath, the brains behind Equity Intelligence India, is not your average investor. This Indian fund manager has made a name for himself by betting against the crowd and digging deep to find undervalued gems in the stock market.

His bold calls and unconventional strategies have paid off handsomely, making him a well-known figure in Indian investing circles. Veliyath is not shy about sharing his thoughts either – he is a regular on the media circuit and keeps his followers updated on his views through social media.

He recently bought into 2 companies and the move has created ripples in the investment circles.

Let us dig in to see what it in these companies is that could have grabbed Porinju’s attention.

Praxis Home Retail Ltd (PHRL)

Praxis Home Retail Ltd, incorporated in 2011, is in the business of Home Retailing through departmental stores, under various formats.

With a market cap of Rs 195 cr, PHRL operates brick-and-mortar stores of home furniture and home fashion under the brand name ”HomeTown” and caters to the home retail segment in India.

Porinju’s decision to buy a stake in PHRL under his wife Litty Thomas’s name is surprising. Mainly because PHRL is incurring losses for the past many years and its entire net worth has eroded. Also, its current liabilities exceed its current assets.

He has bough 10,00,000 shares of PHRL on the 21st of February 2025 at Rs 13.10, making it a total transaction value of Rs 1,31,00,000. In the past, he held 1.06% stake in the company through Equity Intelligence India Private Ltd, which was sold as per filings made for September 2022.

PHRL’s sales are also something that makes the question mark just bigger on why Porinju bought into the company. Sales have fallen from Rs 683 cr in FY19 to Rs 220 cr in FY2024. This is a drop of 68%.

Even between April 2024 and December 2024, the company has been able to make sales of just Rs 92 cr, raising speculations of a possible bad last quarter and eventually a bad financial year.

The EBITDA (earnings before interest, taxes, depreciation, and amortization) has also been in the negative for PHRL. In FY19 it was a negative Rs 22cr and in FY24, it was a negative Rs 25 cr. However, one small ray of hope is seen as the EBITDA for the quarter ending December 2024, the company has finally seen a positive number of Rs 51 lacs after a long wait.

No wonder the net profits are also not a welcome sight. In FY19 the company declared net losses of Rs 27 cr, and for FY24, the company recorded losses of Rs 86 cr. But when you look at the last 3 quarters, the losses are just Rs 20.5 cr.

For the same 3 quarters in the previous year, the losses were a huge Rs 52.2 cr, so unless something goes completely south, this could be a year when PHRL will see a big drop in losses.

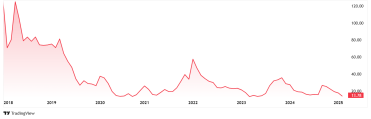

Coming to PHRL’s share price, the company’s share price went from Rs 30 in February 2020 to its current price of RS 13.78 (as on closing of 27th February 2025)

The company’s share is currently trading at a negative PE and hence not available on screener.in. The current industry median is 41x.

On the 14th of February 2025, PHRL has initiated a strategic equity conversion, issuing 52.88 lac shares at Rs 23.19 each to five distinct entities, including AB M Wood Décor and Peps Industries. This move aims to transform Rs 12.26 cr of trade payables into equity, effectively reducing the company’s debt burden and enhancing its liquidity.

All the allottees are independent of the promoter group and shareholders are scheduled to vote on this proposal at an Extraordinary General Meeting on March 13, 2025.

Now for an investor, this signifies PHRL’s commitment to trying to turnaround the business. While the issuance will result in a marginal dilution of existing shareholdings (52.88 Lakh shares out of total 13.52 cr shares), it potentially improves the company’s long-term financial stability. Market sentiment will likely reflect a balance between acknowledging the benefits of debt reduction and any concerns regarding equity dilution. Overall, this equity conversion underscores Praxis’s focus on prudent liability management while pursuing its growth objectives.

Greaves Cotton Ltd (GCL)

Founded in 1859 and bought to India and Incorporated in 1947 by industrialist Lala Karamchand after he bought the company, GCL has been known for decades for their robust diesel engines.

However, they have now completely reinvented themselves. Now, they are all about future-forward mobility, no matter the fuel source.

In FY24, Greaves Electric Mobility announced the launch of the electric 3-W passenger vehicle, Greaves Eltra City. New product Nexus in the E2W segment, was launched in Q1 FY25. In July 2024, it introduced its range of new CPCB IV+ Compliant Gensets.

With a market cap of Rs 5,932 cr, GCL is a leader in India’s 3W engine market. Ampere is ranked 5th in Electric Mobility with a market share of over 2.8%.

Porinju bought 12,51,900 through his company Equity Intelligence India at Rs 234.63/share.

Let us see if the financials were strong enough to pull Porinju’s interest towards them.

The company’s sales grew at a CAGR of 5% from Rs 2,015 cr in FY 2019 to Rs 2,633 cr in FY24. And from April to December 2024, the company has already recorded sales of Rs 2,095 cr.

EBITDA saw a big drop from Rs 272 cr to Rs 91 cr between FY19 and FY24, which is a 67% fall.

GCL also took a big hit when it comes to net profit. For FY24, the company reported losses of Rs 367 cr. This after the company just saw a profit of Rs 70 cr in FY23, after seeing losses of Rs 19 cr and Rs 35 cr in FY22 and FY21, respectively.

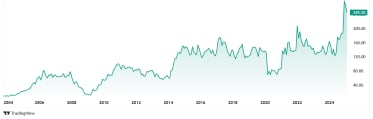

The company’s share price however has seen a jump of 96% in the last 5 years from its February 202 price of Rs 130 to its current price of Rs 255 (as on closing of 27th February 2025).

The current PE of GCL is negative and hence now showing up on screener.in. The current industry median is however 22x.

One positive aspect is that the company is almost debt free.

Greaves Finance Ltd, one of the company’s diversified business entities has a 100% EV-focused lending platform, Evfin, which has partnered with Muthoot Capital to expand electric two-wheeler financing across India, with a total deal size of up to Rs 150 Cr.

GCL is expanding its focus to include fuel-agnostic engines, components, and electric powertrain solutions, moving away from a single-product diesel engine.

With multiple business verticals likes Engineering, Electric Mobility, Retail, Technology and Finance the company is showing a strong back up in place.

According to the GCL’s latest investor presentation, the company’s board has a vision to achieve Rs 15,000 cr (US$ 2B) in revenue by 2030 through a blend of organic growth and strategic acquisitions.

These big plans are probably what caught the fancy of Porinju.

Darkest Before the Dawn?

Porinju Veliyath’s recent plays on Praxis Home Retail and Greaves Cotton is surprising because both companies are facing headwinds right now. Praxis is struggling with its net worth, and Greaves, despite decent sales, is showing some significant red.

However, Veliyath’s move suggests something else. Has he spotted something others have not – a potential comeback story, maybe? With Praxis cleaning up its balance sheet by swapping debt for equity, and Greaves is making a big leap into the future with electric and adaptable engines, these could be some great turnaround stories.

So, is this a stroke of genius in the making, or a risky bet? We will have to wait and see, but one thing is for sure – these companies are now firmly on many a watchlist.

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary