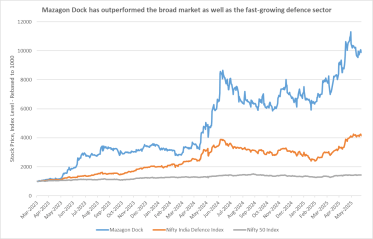

Mazagon Dock, the Navratna-conferred warship and submarine manufacturer, has appreciated by a whopping 250% in less than 3 months. And not without reason.

First, it was Trump’s tariff threats that rekindled investor interest in domestic demand-driven businesses. Defence in particular, held special interest, amid rising geopolitical tensions around the world. And then, as war stepped closer home after the Pahalgam attack, defence stocks soared even further.

But it is important to note that Mazagon Dock has outperformed the broader defence sector. Mazagon is the only government-owned shipyard that is engaged in building and repairing defence ships and submarines.

Established in 1774, 98% of its revenues are derived from defence-related orders for construction and repair of warships, submarines, and other maritime vessels for the Ministry of Defence.

Expectations have soared

Mazagon’s fast-expanding order-book and strong execution track-record have drawn in investors in hordes. But it is not just retail investor optimism (obsession?) with the defence sector that has supported the stock’s rise.

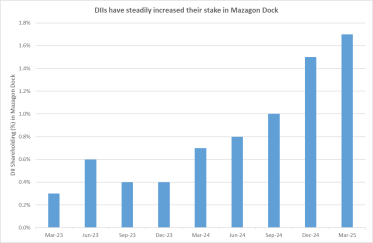

Domestic institutional investors (DIIs) have steadily increased their stake in Mazagon Dock. The government holds almost 85% stake in the company, and DIIs have increased their shareholding from just 0.3% in March 2023 to 1.7% in March 2025. The rising conviction of DIIs in the defence stock speaks to its long-term potential.

The stock is also set to carve its place among large-caps, and make it into the MSCI India Index in August.

But can the business live up to these soaring expectations?

Q4 profits spooked investors, but long-term margin-expansion intact

Mazagon recognizes revenues on a milestone-basis. When the execution on an order reaches predefined milestones, proportionate revenues are recognized. So, in the early phases of an order’s execution, when the focus is on finalization of design and other specifications, costs run ahead of revenues. This results in subdued margins.

But as execution gathers pace, margins pick up too.

This is what has played out over the last few years, resulting in an expansion of margins. Of course, the company’s cost-control initiatives through digital transformation with Shipyard 4.0, AI-based quality checks, and diversified streams of revenues have also played a role.

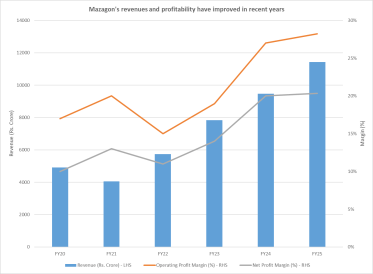

In the latest reported quarter, the company has had to make provisions towards anticipated losses on two of its projects. Due to rising costs towards a Denmark project and an order for fast patrol vessels. The company’s provisions jumped from Rs. 169 crore in FY24 to Rs. 747 crore in FY25, a bulk of which was recognized in Q4. This, along with higher employee and sub-contracting expenses, resulted in the company’s operating profit margin shrinking from 17% in Q4 FY24 to 3% in Q4 FY25. Profits halved year-on-year.

Despite the hit to its profitability in Q4, the company closed the fiscal on a positive note. Revenues expanded by 21% during the fiscal and profit margins improved year-on-year.

Government push fuels hopes

India accounts for less than 1% of global shipbuilding. But it aims to eventually establish itself as the global shipbuilding hub. Towards making this happen, tax relief and other financial incentives have been announced to support domestic ship-manufacturing and associated industries.

In the latest union budget, the government announced the Shipbuilding Financial Assistance Policy to boost domestic manufacturing. Companies which build and recycle ships have been exempted from basic customs duty for 10 years. Rs. 25,000 crore have been allocated towards supporting local shipbuilders.

Such financial incentives rolled out under the policy have improved the business prospects of Mazagon Dock.

Lofty order-book dreams

India’s current naval fleet can sustain for more than a decade. But shipbuilding takes time. Manufacturing of submarines can take up to 8 years. So, orders for new maritime vessels are already in the works.

Mazagon expects new orders worth Rs. 30,000 – 40,000 crore for Project 75 additional submarines to be signed next month. It is also eyeing orders for Project 75(I) submarines, next-gen Corvette and destroyers, repeat orders worth Rs 70,000 crore for Project 17 Bravo frigates, and a Rs 44,000 crore project for Mine Counter Measure Vessels (MCMV).

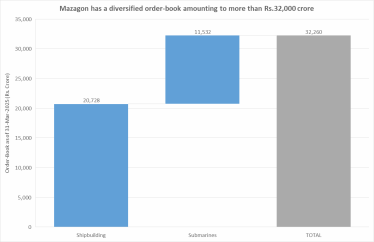

On the back of these orders, the management is gunning for an almost 4-fold expansion in its order-book from Rs 32,260 crore to Rs 1.25 lakh crore. This would translate into an improvement in revenue-visibility from 3 years to more than 10 years. In fact, much of the enthusiasm around the stock centers on the business’ ballooning order-book amid India’s persistent defence push.

Execution and margin risks can rain on hopes

It is important to note that for the newly bagged orders, even as costs start picking up now, revenues will start flowing in only in FY28. So, the management has guided for 8-10% growth in revenues at 15% PBT margin in FY26. Analysts and investors are pricing in faster growth at wider margins.

Moreover, the business is no stranger to negative surprises. The company had to recently ramp up provisions due to rising costs in two of its projects. The management has left the door open for further provisioning in subsequent quarters, if needed.

Order-wins and execution have been volatile as well. Execution on the 2015 order for stealth frigates under Project 17 Alpha, and that for 4 destroyers awarded under Project 15 Bravo in 2011, had seen delays. As competition rises from private players, more such negative surprises can spring up on order-wins, execution, and costs. On cue, investor sentiment could dampen.

Capex plans can add debt

Mazagon’s capacity can also constrain growth. The company’s current capacity can handle parallel manufacturing of 10 warships and 11 submarines. While the submarine capacity has expanded from 6 to 11 in recent years, the company’s shipyards can only handle repairs of small to medium-sized ships. Moreover, India’s persistent push on expanding its defence capabilities calls for further capacity expansion at Mazagon as well.

Towards this, it has committed to doubling its capacity with investments worth Rs 5,000 crore spanning the next couple of years. With sufficient cash reserves, the expansion is likely to be largely met through internal accruals. But if the expansion plans lead to addition of significant debt to its books, investors will no longer be able to draw comfort from its zero-debt position. So, the debt on its books will need to be closely monitored through the capex plans.

Margins to moderate going forward

The company is in a transition phase where older projects are nearing completion, and new projects kick off. Several vessel deliveries are coming due over the next couple of fiscals. This should close the last legs of revenue-recognition for these projects, while costs remain under budget. Consequently, the trend of margin improvement witnessed over the last few fiscals could continue until around FY27.

But thereafter, as work begins towards the new orders, revenue-recognition would be back-loaded and operating margins can fall back towards 12-15%. Of course, the management expects offshore and export orders to pick up some of the slack in revenues. That said, the company has also forayed into AI-based security contracts. The lack of a robust track-record in the field raises questions on how this would play out.

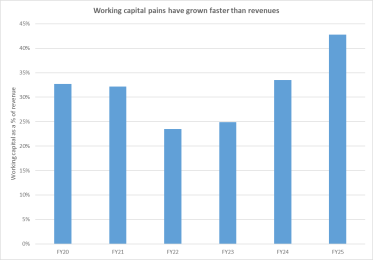

Furthermore, as is typical with companies catering to government projects, receivables have remained under stress. In fact, working capital requirements have spiked from 33.5% of revenues in FY24 to 42.8% in FY25. As margins moderate and working capital pressures escalate, cash-flow management could get trickier.

Valuation poses significant risk

With a sharp acceleration in growth over the last few years, the stock’s valuations may have run ahead of business fundamentals. The stock is trading at more than 55 times its trailing-twelve-month earnings. Recent growth has been projected into the future as well.

In fact, analysts’ projections on growth and profitability are markedly more aggressive than the management’s guidance. With revenue and EBITDA projected to grow at up to 20% and 35% CAGR respectively between FY25 and FY27, the stock’s target price has been pegged at Rs.3,858-4,350 apiece. This reflects an upside of 20-35% over current levels.

But if growth disappoints going forward, the stock can see volatility, that may be exaggerated by its recent inclusion under F&O contracts. Corrections can bring the counter down to more defensible valuations.

Disclaimer

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Ananya Roy is the founder of Credibull Capital, a SEBI-registered investment adviser. An alumnus of NIT, IIM, and a CFA charter-holder, she pens her views on the economy and stock markets.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.