")

SRF has managed to stage a comeback in 2025 after 3 years of underperformance. The company has managed to turn around thanks to strong domestic performance. But can it continue?

Pandemic boom

Specialty chemical stocks have been a tough sector for investors in the last few years.

These stocks had been on a roll since 2020 to 2021. The pandemic increased demand for local players as Chinese companies were struggling with reduced production. The zero-COVID policy in China ensured that Chinese companies struggled with their supply chain.

Indian specialty chemicals grabbed the opportunity, and this includes SRF.

SRF’s numbers increased significantly during this time.

Its revenue jumped by 48% in FY22, compared to a 16% increase in the previous year. Net profit also surged by 57% against a 17% jump in FY21.

Export demand crumbles

Things took a turn when the Chinese firms came back. Due to lower demand on account of China’s weak economy, they started dumping their products all over the globe. This pushed the prices down, affecting Indian chemical companies as well.

Another factor that affected the demand was destocking done by US and European companies after the pandemic. These companies overstocked during COVID, fearing supply chain disruptions may last far longer than they actually did. But once the lock downs ended and things started to normalize, these companies started drawing down on the supplies, which reduced demand.

From January 2022 to January 2025, a period of three years, SRF shares had fallen by 2%, as the stock struggled with demand.

SRF shares from January 2022 to January 2025

This was a reflection of the fundamentals of the company. The company’s FY24 revenue of Rs 13,139 crore grew at 2.8% CAGR from FY22.

Turnaround

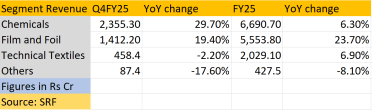

The overall environment for specialty chemical stocks, including SRF started to turn around in Q4FY25. In SRF’s case, revenue surged 20% from the previous year to Rs 4,313 crore. From the December quarter, the top line increased by 23%.

The chemical segments’ revenue grew by 29% in Q4FY25. It contributed to 45% of the company’s revenue in FY25.

The company achieved this through the traction for newly launched products. The demand pick-up in agrochemical intermediaries also helped.

This was reflected in the stock price as SRF’s share price surged by 38% in 2025 so far.

SRF shares in 2025

HFC production ramp-up

The company also recorded high volumes of hydrofluorocarbons (HFC) in domestic and export markets.

SRF also recorded the highest-ever domestic refrigerant gas sales. This was driven by its highest-ever R32 gas production.

R32 is a refrigerant gas mainly used in air conditioners.

Moving forward, the company expects higher demand for refrigerants used in increased AC and automobile production in India.

As India is facing more heat during summer, it could lead to more AC demand.

The mandate for in-cabin AC for commercial vehicles will also increase demand.

The company is also planning to maximise HFC production within India’s phase-down quota till 2026.

India has committed to decreasing HFC production under the Kigali Amendment to the Montreal Protocol.

For this, a baseline year has been set from 2024 to 2026. In this period, India will calculate its average HFC consumption. From 2028, HFC production will be reduced in phases.

This is done to combat global warming as HFC is a greenhouse gas.

As companies can maximise production before 2026, SRF is also looking to do the same. SRF increased its capacity by 30% by debottlenecking and R&D.

SRF’s other segment also posted good growth, adding to its resurgence.

Its packaging films business grew 19% from the previous year. For the BOPET and BOPP segments, margins improved due to increased capacity utilization.

BOPET and BOPP films are important materials for packaging in various sectors.

BOPET is crucial for consumer electronics and medical devices. BOPP is used in food packaging.

Outlook

The management gave a 20% growth guidance in FY26 for the overall chemical business. SRF expects this on volume growth in the HFC business and traction in agrochemical intermediaries.

HDFC Securities gave an add call with a target price of Rs 3,111 in a May report. The brokerage valued the company at 42 times FY2026 P/E.

This is a 2% upside from Monday’s close.

According to the brokerage, the energy cost in Europe is likely to soften. This will help the packaging films business.

The brokerage is upbeat on the company due to a strong outlook for refrigerants. Its newly launched products in the specialty chemical business are another factor.

What could derail SRF?

The company may not be out of the woods yet, as China still casts a large shadow. Cheap Chinese imports and inventory dumping are still putting pricing pressure on the company’s chemical business. The company’s textile business is seeing weakness due to Chinese imports and weak Indian government spending.

Kotak Institutional Equities in a May report maintained a sell call with a Rs 2,060 target price.

According to the research firm, SRF management has missed guidance in the last 2 years. This casts uncertainty on the management’s 20% growth outlook. Challenging global macro conditions would also affect the 2026 guidance, according to Kotak.

Kotak added that the stock is trading at expensive valuations at 50 times FY2026 P/E.

Conclusion

While SRF managed to stage a turnaround from previous weakness, dark clouds loom over the company in the form of China. The tough macro conditions are also expected to play spoilsport for the company.

However, as India faces increasing temperatures, it could help with SRF’s main refrigerant business.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Ananthu C U is an equity market journalist who has written about listed companies, equity market regulations, and economic development. He is deeply interested in increasing his knowledge about the equity market, the Indian economy and listed Indian companies. He generally tracks infrastructure, power and financial companies.

Disclosure: The writer and his dependents do not hold the stock discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.