By Mohit Bhambhani

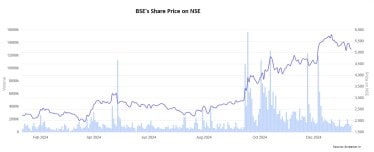

The surge in the stock price of BSE in the last year has been breath taking. One look at the chart and you know this was something special.

But then this is history. What lies ahead for BSE?

Well, if you believe a leading research house, BSE may be set for another 25% rally.

But let’s not get ahead of ourselves. Instead, let’s start with understanding what the BSE’s business is all about.

BSE’s Business

BSE’s businesses include the following:

- Trading and Clearing – catering to trading of Equity, Debt, Derivatives, SMEs and Startups, Spot Markets, and Interest Rate futures.

- Distribution – Mutual funds, Book-building services for IPOs, New bond platform, Offer to buy/sell, and Insurance.

- Services to Corporates – Equity listing, Listing of Debt Securities and Commercial Papers, Mutual funds listing

- Other services include Data feed, Index services, Software services, and Training services.

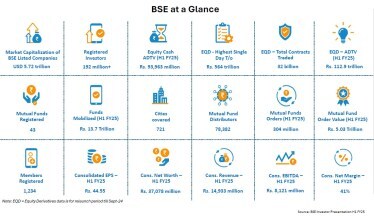

As per the BSE’s Investor’s Presentation for H1 FY25 in November 2024, BSE has over 192 million registered investors, 1,234 registered members, and 78,382 Mutual Fund Distributors, covering 721 cities across India.

Even though the BSE has lost the race to the NSE long ago, its numbers are still vast. Where it gets interesting is that in some areas, the BSE is actually starting to regain some share.

During the Q2 FY25 conference call, Mr. Sundararaman Ramamurthy, MD and CEO of BSE said BSE has recorded its best ever half year revenue and profit, recording highest ever quarterly consolidated revenues of Rs. 819 crores, a 123% growth over the revenues in corresponding quarter last year. The growth was driven by strong performance in transaction-related income, investment-related income, and treasury income from clearing and settlement services.

He added that BSE platform continues to remain the preferred choice of Indian companies by enabling issuers to raise Rs. 13.7 lakh crores by the means of equity, debt, bonds, commercial papers, mutual funds, etc.

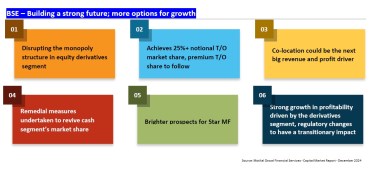

As per Motilal Oswal Capital Markets report dated December 2024, the equity derivatives market where NSE had a monopoly earlier, BSE has now achieved a market share of over 23% in notional options turnover.. BSE has increased its market share through launch of contracts with smaller lot size, changes in expiry, and lower transaction fee.

Mr. Sundaram R. also clarified that the size of contracts was to be increased on November 20, 2024, which in turn will increase the premium earned, and in turn the transaction charges received would increase. However, the clearing charge is based on number of contracts, and so it would move in sync with the volume of contracts.

Financials Explained

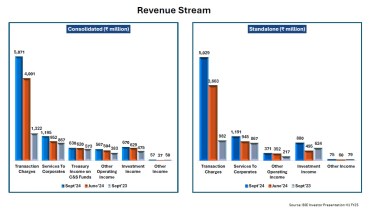

For Q2 FY25, BSE reported operational revenues of Rs 746.3 crores, a 237% growth over the operational revenues of Q2 FY24, investment income was nearly Rs 67.0 crores, and other income of Rs. 5.7 crores. Net profit came in at Rs. 345.8 crores for Q2 FY25. Over last three years, BSE has reported a compounded sales growth of 36%; while the compounded profit growth too has been 36% over last three years.

The largest chunk of revenue is generated through the transaction charges including the equity cash, equity derivatives, mutual funds, and clearing house income, which contributed Rs. 507.1 crores during the quarter, a 284% growth from Rs. 132.2 crores in Q2 FY24.

The company has maintained a healthy dividend pay-out of 57.2%, and is almost debt free. Since MCX and BSE are exchanges for commodities and stocks respectively, they can be compared. MCX also has a healthy dividend pay-out of 58%.

BSE’s Return on capital employed (ROCE) has increased to 20% in March 2024 from 12% in March 2023 which represents an improving operational efficiency; while for MCX, ROCE has been 7.1% in March 2024, as compared to 13% in March 2023. The median return on equity (ROE) has been around 10% over last 10 years for both BSE and MCX. But considering last three years, BSE’s ROE of 11.3% is still better than MCX’s ROE of 9.1% over last three years.

BSE is trading at 18.8x its book value of Rs. 274, while its peer MCX is trading at around 18.3x its book value of Rs. 311.

Coming to the shareholding pattern of BSE, as of September 2024, Foreign institutional investors (FIIs) have increased their holdings to about 13.0%, as compared to 7.9% holdings in September 2023; while the domestic institutional investors have increased their holdings to about 11.7%, as compared to 8.1% in September 2023. The holding of public at large has decreased to 52.4% in September 2024, from 58.9% in September 2023, while others holding has decreased to nearly 22.9% of the shares, as compared to 25.1% in September 2023.

What Analysts Say?

In December 2024, Motilal Oswal Financial Services Ltd, in its Capital Markets report, recommended a “Buy” on the company’s shares, stating that it expected the company to deliver a 45% compound annual growth rate in revenues following an exponential growth in options volume. It set a one-year target share price of Rs 6,500 based on 42x the company’s 2026 PE estimates. This implies a return of over 25% from current levels.

However, in December 2024, HDFC Securities Ltd. recommended a “Reduce”, with a target price of Rs. 5,000, based on 38x the FY27 estimated core Profit after Tax and Net Cash. This is due to BSE’s notional volume drop of 20% in December following the collapse of Bankex contract. The report also states that the rise in Price to Notional percentage will protect the premium and the shift from expiry to non-expiry trades will boost the margins.

Concluding this, BSE could show an upside from current levels considering the growth in revenues, improving profitability, and the changes including new products and derivatives introduced by the company over last few quarters. Only time will tell whether it’s strategy continues to play out well…

Disclaimer

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Mohit Bhambhani is a seasoned financial professional with over 13 years of experience in the field of financial research and corporate advisory. He also has substantial experience in Indian stock markets. With an analytical approach, he studies the performance of companies deeply, bringing value to the readers.

Disclosure: The writer and his dependents do hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.