at Rs 4-5 bn resulting in lower net portfolio accretion.")

Repco Home Finance’s (Repco’s) Q4FY21 earnings exceeded our expectations with PAT growth of 33% y-o-y (3% earnings growth for FY21). Stage-3 pool being contained at 3.7% and credit cost managed sub-1% for Q4FY21 and 0.7% for FY21 came in as a positive surprise. However, Covid second wave disruption and extended impact in Tamil Nadu throw in uncertainty for FY22. Disbursements failed to cheer with a mere 6% y/y growth in Q4FY21 (down 30% in FY21). This coupled with elevated balance transfer weighed on AUM growth (2% for FY21).

Though growth momentum lags peers, superior NIM and lower credit cost can sustain Repco’s RoAs at >2% and RoEs at >13%. We believe the company’s business franchise is currently undervalued – stock trades below FY23E book and 7x earnings, and is available at <0.2x AUM. Maintain Buy with a target price of Rs 650. Key risks: fundamentally weak performance derailing growth, and quality of credit amidst Covid disruption.

Stage-3 pool well contained; Covid second wave disruption key monitorable: Against the apprehension of rise in stage-3 assets, the pool was contained at 3.7% in Q4FY21 vs Q3FY21 proforma stage-3 of 4.3%. Collection efficiency in Q4FY21 was near pre-Covid levels of 95-96%. Second wave disruption would however have derailed collection efficiency in Q1FY22. We expect stage-3 pool at 5-6% in the initial part of FY22.

FY21 credit cost at less than 70bps: Credit cost of Rs 292 mn (sub-1% for Q4FY21) was primarily towards stages-1/2 assets, thereby exiting FY21 with credit cost at less than 70bps. It carries management overlay of Rs 425 mn (35bps of advances). Overall, Repco is carrying cumulative provisions of 2.4% against stage-3 assets of 3.7%. We are building in credit cost of 1.4%/0.6% for FY22e/ FY23e respectively. Restructuring was stable at 0.3% (included in stage-3), but restructuring under resolution framework 2.0 (not coexisting with moratorium) can be relatively higher in FY22.

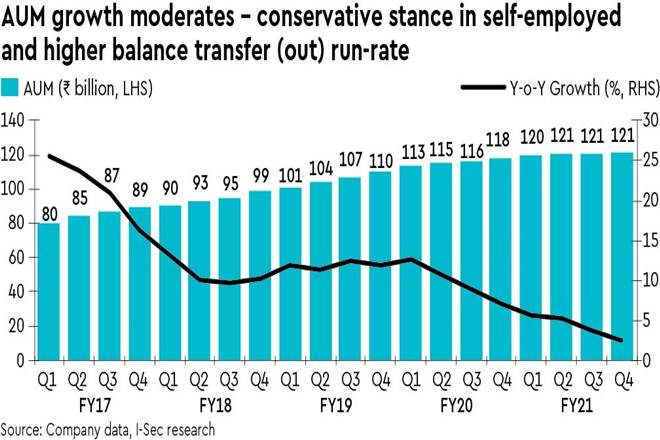

AUM growth moderate as low disbursements and high balance transfer weighs: Disbursements grew by only 6% y-o-y in Q4FY21 thereby exiting FY21 with 30% lower disbursements vis-à-vis FY20. Against the guided monthly disbursement run-rate of Rs 2.2-2.5 bn, Q4FY21 disbursements were marginally lower at Rs 6.4 bn due to Tamil Nadu election impact.

Consequently, loanbook growth further moderated to 2% (from 5-7%) to Rs 121 bn (almost flat q-o-q), which shows that the company is still very conservative in lending compared to peers. In terms of geographical distribution, Maharashtra and Gujarat loanbooks have grown in the range of 7-9%, while southern states derailed the momentum. Also, competitive intensity as well as Repco’s high lending rate vs peers is leading to elevated balance transfer (outward) at Rs 4-5 bn resulting in lower net portfolio accretion. Going forward, we are building in loan growth of 2% and 6% for FY22e and FY23e respectively.