While there is a growing concern that telecom tariff hikes may only take place after general elections, it could lead to accelerated market share shifts and in theory an effective duopoly which could add Rs 93/sh upside potential. Reliance Jio is the telecom arm of billionaire Mukesh Ambani-led Reliance Industries.

Addressing concerns on Jio: Following up on our recent note addressing key investor concerns on RIL which addressed the key concerns on capex, leverage and slower growth in Retail, we look at the key investor concerns on RIL’s telecom operations in this note. In our recent interactions, delays in timing of tariff hikes—potentially after the general elections in May-24, have been cited as the key concern on Reliance Jio, besides rising capex and leverage.

Also read: Is compounding truly the 8th wonder of the world?

Inflation vs an effective duopoly: There is a growing concern that tariff hikes may happen only after general elections due to the government’s focus on controlling inflation. In our view, the delay in hikes also seems unlikely because of cash-flow pressures being felt by Vodafone Idea Ltd. which in turn may bring the sector closer to an effective duopoly ahead of time.

VIL’s debt conversion positive for tariff outlook: We note that the government’s recent decision to convert a portion of VIL’s debt to equity has made it the largest equity stakeholder in VIL. This is likely to align its interests towards a tariff hike to support VIL. Moreover, this is also likely to shift Bharti/Jio’s focus away from market share gains towards market expansion, said the report.

Is an effective duopoly a possibility? VIL may potentially be able to secure incremental funding given the government’s support but we believe it would be unlikely to match Bharti/Jio’s network capex of $9/14bn over FY23-25. This would likely continue driving market share towards Jio and Bharti. As per our calculations, RIL’s FV could potentially rise by Rs 93/share in the event of an effective duopoly scenario.

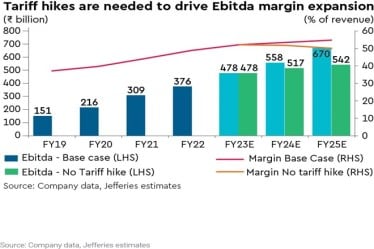

Normalising tariff hike assumptions: While the pace of tariff hikes has disappointed, the government’s recent stake in VIL could drive positive surprises. Over FY23-25, we now expect a single tariff hike of 15% towards end-CY23, resulting in 1-6% cuts to our FY23-25 revenue/Ebitda estimates. Post the cuts, we expect Jio to deliver 15/18% revenue/Ebitda Cagr over FY23-25. We lower our EV for Jio to $80bn.

Also read: Analysts slash crude oil price forecasts amid recession fears; go short at Rs 6000/bbl

Favourable risk reward: Our FY24/25 Ebitda estimates for Jio could be lower by 7-19% if there were no tariff hikes till Mar-25. In such a scenario, and all else being equal, our EV for Jio would fall by 25% to $60bn. Even then, RIL’s SoTP-based fair value would be Rs 2,872, implying 28% upside from CMP and suggesting a favourable risk-reward. We maintain Buy with a revised price target of Rs 3,060, implying 36% upside potential.