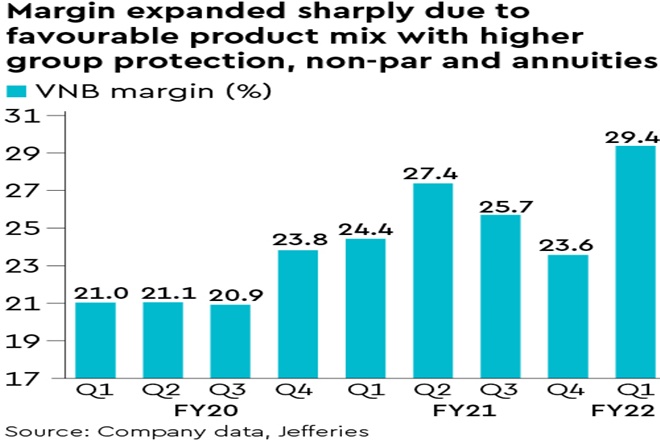

Like its sector peer, IPRU saw a sharp spike in Covid claims + provision at ~Rs 10 bn – 5x FY21 net Covid claims & ~3% of FY22EV. It posted a net loss of Rs 1.86 bn but VNB margin surprised at 29.4% (vs. our est of 23.7%) on better mix – VNB grew at 78% y-o-y with APE growing at 49% y-o-y. Its new banca partnerships are shaping up well, product mix is getting diverse & low base is helping growth in FY22. We expect VNB CAGR of 21% over FY21-24. Buy with Rs 750 PT.

Sharp jump in Covid expenses… IPRU’s Q1FY22 net Covid claims jumped to Rs 5 bn, while it provided a further Rs 4.98 bn . This also affected profitability with net loss at Rs 1.86 bn. Net Covid claims in Q1FY22 were 2.5x FY21, while average claim size has been 1.37x – owing to the impact on the under-45 cohort, where IPRU has a larger proportion of its policies.

…but VNB surprises big: IPRU posted a big beat on VNB margin – 29.4% on better product mix. VNB stood at Rs 3.6 bn, up 78% y-o-y. While retail protection declined y-o-y, overall protection premiums were up 26% y-o-y, taking protection share to 24%. Strong growth in non-par savings also aided margin. We expect FY22 margins to be healthy at 26.5%. Management sticks to its guidance of doubling FY19 VNB by FY23, and this quarter’s margin beat should help. Persistency improved with 13th month at 85.4% (+60bps q-o-q).

49% y-o-y growth on low base; product mix is improving: IPRU has started to benefit from low base with total APE growing 48% y-o-y and retail growing at 42%. We expect IPRU to see 24% FY22 APE growth – highest among listed players. Product mix is improving, with dependence on ULIP declining and share of non-par savings, annuity & protection rising. Credit protect has grown strongly on rising disbursements. IPRU also focused on group term in Q1—drawing comfort from high level of vaccination at employers’ and limited price negotiations. Retail term was lower y-o-y as underwriting comfort is still constrained. Annuity APE grew 164% y-o-y with ICICI Bank pushing it aggressively, and non-linked savings were up 66% y-o-y.

New banca partners shaping up well: Management indicated that at the 4 new banca partnerships (IIB, RBL, AuSFB, IDFC) IPRU’s share platform insurance sales is rising. We see these 4 partners as key components for IPRU to deliver on its FY23 VNB target of Rs 26.5 bn. ICICI Bank has also begun seeing strong growth on low base. The focus on agency additions stayed with 4518 agents added during Q1.

Maintain Buy: We expect high premium growth in FY22 and pay-offs from new distribution tie-ups. We see a 21% CAGR in VNB over FY21-24 aided by premium growth. We also see ROEV of 15% in FY22. With valuations at 2.6x FY22e P/EV, we see a favourable risk/reward and maintain ICICI Pru Life among our top picks with a PT of Rs 750 based on 2.7x Mar-23e P/EV.