For Q2FY22, HDFCB’s profit of `88 bn, up 18% y-o-y, was a tad ahead of estimate aided by lower provisions. We are encouraged to see 5-7% q-o-q growth in retail/ commercial loans and management outlook sounded of bouyancy. Slippages were manageable & restructured loans rose from 0.8% of loans to 1.5%. Subs’ performance rebounded led by HDB-FS. Rebound in growth could aid rerating given recent underperformance – we marginally raise est. and TP to `2,070. BUY.

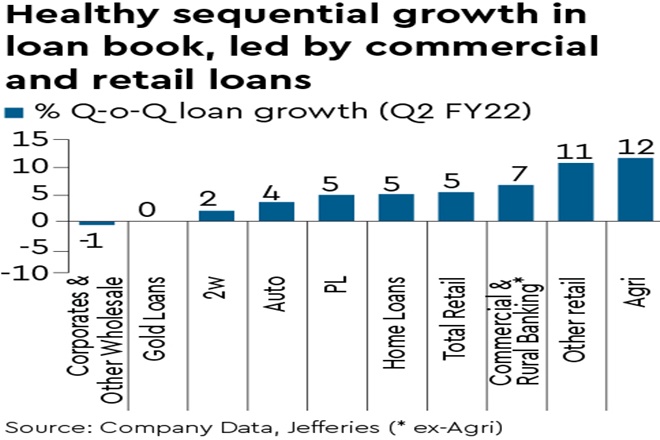

Uptick in retail & commercial lending activity is positive: The key positive trend from HDFC Bank’s Q2 results was the q/q uptick in retail loans (5%) and commercial loans (7%) – reflecting normalisation in business activity and market share gains. In fact, our recent channel checks show that HDFC Bank has been quite active in financing new demand – this was echoed in mgmt. commentary for festive lending activity as well. Overall loans grew by 4.4% q/q (16% y/y), a tad slower than retail segments due to modest growth in large-corp loans. CASA deposits rose by 29% y/y to 47% of deposits.

Operating profit growth dragged by cost growth, but momentum to improve: NII rose by 12% y-o-y and 4% q-o-q; fees growth was strong at 26% y-o-y, partly due to lower base. Operating costs rose by 15% y-o-y reflecting lower base, rise in origination cost and ESOP cost amortisation. Operating profit (ex-treasury) rose by 14% y-o-y and we see the momentum improving with uptick in lending activity and topline.

Slippages stable, but need to watch out for potential slippages from restructuring: Bank saw slippages at 2% of past year loans (annualised) and gross NPLs fell by 4% q-o-q to 1.4% of loans. Restructured loans rose from 0.8% of loans to 1.5%, due to fresh restructuring under second-package – 80% of fresh restructuring was of personal loans. We note that 23% of personal loans restructured in first-package slipped into NPL. While mgmt sees only 10-20bps of loans as peak-potential impact on NPLs, we watch out for trends here. Provisions were up just 6% y-o-y and 30% of total provisions were towards contingencies; core credit costs were at 1.3% of average loans. We expect credit costs to normalise towards 1.1-1.2% of average loans, savings from which management could utilise for opex/ investments.

Subs see rebound in performance: Subsidiary profits rose strongly as HDB Financial Services returned from loss last year to profits. HDFC Securities also reported 43% y-o-y growth in profits.

Maintain Buy: We raise estimates by c.1% and see 18% CAGR in profit over FY21-24. Rebound in growth can aid rerating given recent underperformance (YTD HDFCB up 18% vs. 31% for Nifty and 26% for Nifty Bank). We maintain our Buy rating with a TP of `2,070 (from `1,900) based on bank value at 3.7x Sep-23E adjusted PB. Our price target for ADR is $92, based on FX conversion of our local price target and a 12% premium.